Coast FIRE Calculator

Save until your Coast age, then stop contributions — and still reach FIRE by your chosen retirement age.

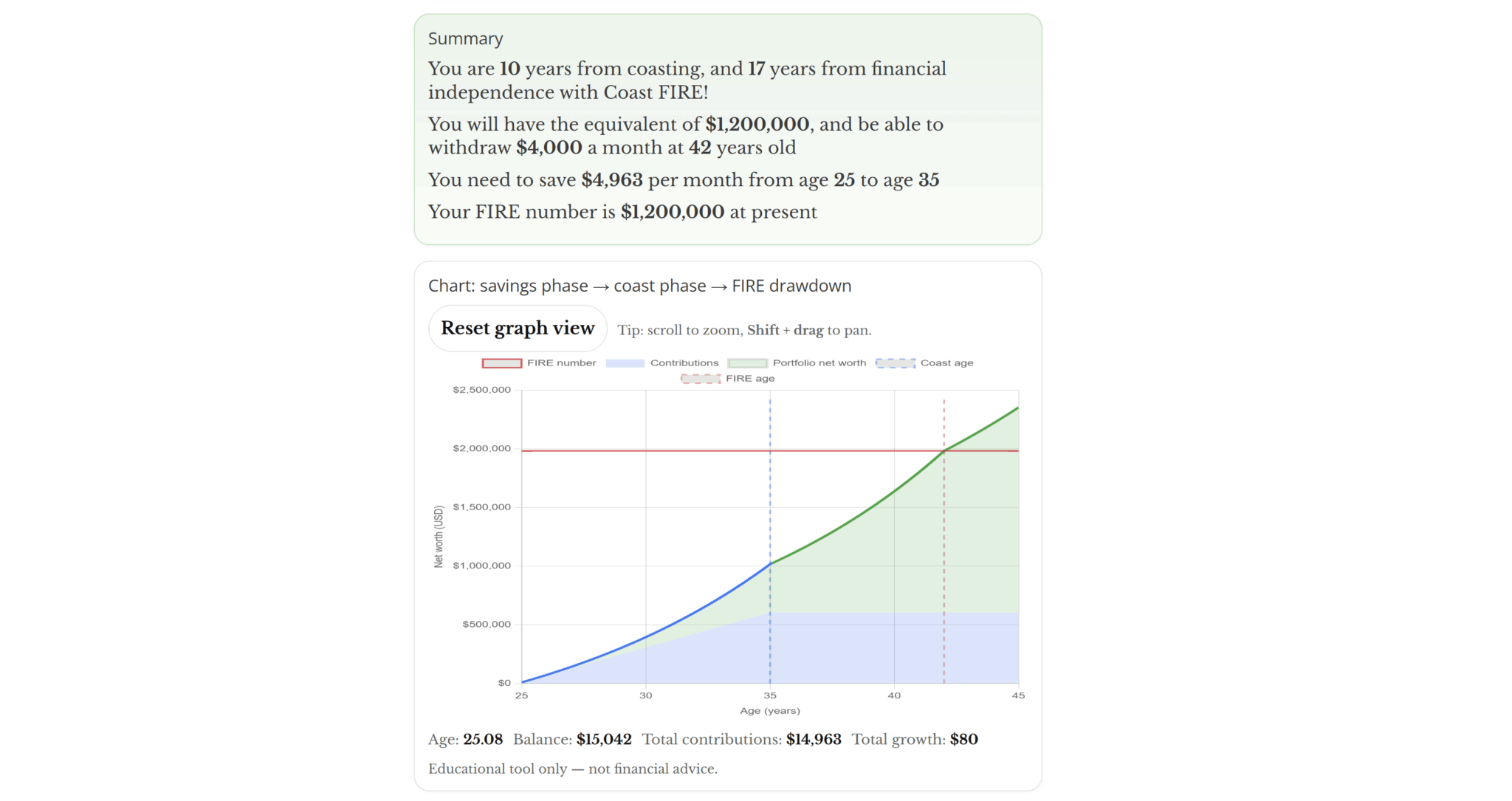

Summary

Inputs

Assumptions

Summary

Chart: savings phase → coast phase → FIRE drawdown

Outputs

Inflation adjusted (today’s dollars)

Nominal data (future dollars)

Projection table (annual)

Show table

| Year | Age | Contributions | Withdrawals | Investment growth | End balance |

|---|

Find Your FI Number Where Compounding Does the Heavy Lifting

Coast FIRE is the moment your portfolio hits a size where—if you stop contributing—time and compounding can carry it the rest of the way to traditional retirement.

In other words: you don’t have to “hit FIRE” today. You just have to reach the point where your money can coast.

This Coast FIRE calculator helps you estimate:

- the portfolio value you need now,

- given your age, target retirement age, expected returns, and inflation assumptions.

It’s the most underrated FIRE milestone because it changes how you work: you can stop sprinting.

Stop guessing. Stress test your plan for 50 years.

Build your FIRE number, then pressure test withdrawals across inflation and ugly sequences.

- PASS/FAIL + ruin year

- Inflation plus real return sequences

- One-time expense shocks

Includes the FIRE Number Builder, 50-year Stress Test, and the IPS rulebook.

What this Coast FIRE calculator does

This calculator estimates:

- Your Coast FIRE number (the amount you need invested today to coast to your future FI target)

- How your number changes with age, retirement date, and expected returns

- How much contributions matter vs how much time matters

- How “coasting” can reduce savings pressure and open up life choices earlier

Coast FIRE isn’t retirement. It’s leverage.

Coast FIRE in one equation (conceptually)

Coast FIRE is essentially:

What do I need invested today so that future growth = my target retirement portfolio?

There isn’t a single one-line formula that stays accurate without assumptions (returns, inflation, years to grow), which is exactly why a calculator matters here.

How to use the Coast FIRE calculator (fast and correctly)

- Enter your current age and target age

Coast FIRE is time-sensitive. A few years changes the math. - Enter your current invested assets

Use investable portfolio value, not home equity unless you plan to monetize it. - Enter your retirement spending goal (or target portfolio)

You can use a FIRE number based on expenses × 25, or input your target directly. - Set realistic return and inflation assumptions

Don’t optimize for optimism. Coast FIRE works best when it’s conservative enough to survive reality. - Stress-test with two scenarios

A normal market assumption and a “lower return” assumption.

How to interpret your results (so the number actually helps you)

If you already hit Coast FIRE

That’s a major milestone. It means:

- you can reduce your savings rate,

- change jobs,

- downshift intensity,

- or design a Barista/Expat/Nomad plan

…but you should keep a margin of safety. Coast FIRE is powerful, but it’s still exposed to returns and inflation.

If you’re close

This is where Coast FIRE shines psychologically. You’re not “years away from freedom”—you’re often months to a couple years away from coasting. That can change how you negotiate, work, and plan.

If it’s far away

The levers are simple:

- increase contributions

- extend time horizon slightly

- reduce target retirement spending

- stack Coast FIRE with geoarbitrage (Expat/Nomad) or Barista FIRE

Common mistakes people make with a Coast FIRE calculator

- Assuming high returns without stress-testing lower ones

- Ignoring inflation (it quietly breaks long plans)

- Using a retirement spending target that isn’t realistic

- Counting assets that won’t actually fund retirement

- Treating Coast FIRE like “I’m done”—it’s a milestone, not the finish line

Coast FIRE is freedom from sprinting, not freedom from planning.

What to do next (once you know your number)

- Decide whether you want to keep sprinting, or start coasting.

- If you’ve hit Coast FIRE, design the next phase:

- reduce savings pressure

- optimize for lifestyle and health

- consider Barista FIRE or Expat/Nomad “bolt-ons”

- Re-run the calculator annually and after major changes (income, spending, markets).

For the full guide on what Coast FIRE means—and how to use it without making your plan fragile—read the complete Coast FIRE guide here: (coming soon**).

.

.

ABOUT THE AUTHOR

Carlos Grider launched A Brother Abroad in 2017 after a “one-year abroad” experiment turned into a long-term life strategy. After 65+ countries and a decade abroad, he now writes about FIRE, personal finance, geo-arbitrage, and the real-world logistics of living abroad—visas, costs, and tradeoffs—so readers can make smarter global moves with fewer surprises. Carlos is a former Big 4 management consultant and DoD cultural advisor with an MBA (UT Austin) and Boston University’s Certificate in Financial Planning. He’s the author of Digital Nomad Nation: Rise of the Borderless Generation and is currently writing The Sovereign Expat.