A complete guide to the 4% rule, your FI number, 25x, and crafting a FIRE plan.

Most people are taught a simple financial script for their lives: go to school, work for 40–45 years, spend as you go, and retire at 65…if you’re lucky. Then, in retirement, if everything goes right, you may get 10–15 healthy years to enjoy before your body and options start to degrade.

The problems are obvious: you spend your best years trading time for money, and the years when you finally “get your time back” often arrive as your energy, health, and curiosity are fading.

Fortunately, a growing movement of people is not so quietly refusing that script, and sharing new ideas for achieving financial independence earlier than tradition dictates. They’re using a different way of thinking about money –the FIRE movement – to move their freedom years earlier in life. Instead of asking “At what age do people retire?” they ask a better question:

How much money do I need for work to be optional, and how can I get there faster?

Stop guessing. Stress test your plan for 50 years.

Build your FIRE number, then pressure test withdrawals across inflation and ugly sequences.

- PASS/FAIL + ruin year

- Inflation plus real return sequences

- One-time expense shocks

Includes the FIRE Number Builder, 50-year Stress Test, and the IPS rulebook.

You don’t have to wait until a certain age to retire. You can “retire,” or just work on your own terms, when your assets can reliably cover your spending. Your ability to become financially independent is driven by what you save, spend, and invest, not how old you are. That mindset shift matters because it transforms “I retire at 65” into “I retire when I hit $X,” which is a plan you can not only control but also accelerate, if you know how.

This guide will explain what financial independence is, show you how to calculate your FI number, and walk you through the steps to become financially independent, including how living abroad and traveling the world along the way can cut that number and your timeline in half.

Disclaimer: This content is for educational and informational purposes only and is not individualized financial, tax, or legal advice. I don’t know your personal situation, and reading this does not create an advisor-client relationship. Consider consulting a qualified professional before making financial decisions, and invest based on your goals, time horizon, and risk tolerance.

Assumptions Notice: Examples and calculator outputs are hypothetical, based on user inputs and assumptions (e.g., returns, inflation), and actual results will vary.

Contents

- What is Financial Independence?

- Why Financial Independence Matters

- A Glimpse of modern financial independence, in the real world

- The Simple Math of Financial Independence: Your Savings Rate + the 25x rule

- How long will it take to FI

- How to become financially independent: A step-by-step guide

- The FIRE Movement: Ideas on the Fast Track Method to FI

- The Variations of FIRE: Lean, Coast, Barista, Expat, and Nomad FIRE

- FIRE Abroad: How choosing the right location can cut your FI number and time to FI in half

- Financial Independence vs Financial Freedom: What’s the difference and why it should matter to you

- How realistic is FIRE?

- The Risks, Trade-Offs, and Flexible Safety Nets for any Good FI/RE plan

- Step-by-step: How to Become Financially Independent

- Useful Tools, Resources, and Calculators for Your FI and FIRE Journey

What is Financial Independence?

Financial independence (FI) is the state of having a secure financial position in which your investments, investment returns, and other assets reliably cover your cost of living, so paid work becomes optional.

In FI, you can keep working if you want to, perhaps because you enjoy the work, the structure, the purpose, and the social contact, but you no longer need to work just to keep the lights on and food on the table. In financial independence, your time is no longer rented out by the hour to pay for your basic life. Your time and your life become yours without question.

FI is about using financial security to create options.

For example, with financial independence, you might:

- Leave a job that’s draining you without panicking about money

- Take a year off to travel, write, learn a new trade, or raise a child

- Switch to working part-time in a field you love

- Take up a cause you care about, even if the endeavor pays less or nothing at all

- Move abroad to somewhere that fits your values, mindset, and desired lifestyle better

When FI, you’re no longer financially dependent on an employer, a spouse, a government program, or “the market” staying perfect. Your own assets and habits give you room to breathe.

Why Financial Independence Matters

Interest in FI has exploded among millennials and Gen X for a simple reason: in unstable times, it lets them retake control of their financial future.

Traditional safety nets are becoming shakier. Company pensions are vanishing. Government social security programs are under pressure. Employment stretches with a single company are shorter-term and less guaranteed, especially in industries automating with AI and robotics.

Work isn’t delivering what society promised in the generations passed. In several studies by the Pew Research Center, the National Institute of Health, and UGA, nearly half or more of workers reported feeling disengaged or unhappy in their jobs. Workdays are more commonly bleeding into evenings and weekends, suffocating the remnants of personal time and the little extras that should make life enjoyable. All the while commuting, childcare, and the constant cost of “looking professional” eat into both money and time.

Life is more mobile than ever, and FI allows making the most of that opportunity. There’s a quiet opportunity for life optimization for people aiming for FI. Long-stay visas, digital nomad visas, and “independent means” residency options that allow you to live abroad in sought-after locations are quietly multiplying, but the financial criteria for qualifying hold many would-be nomads and expats back. But, if your income is portable and your financial base is solid, you can live in more places, not fewer, and the options to enrich your life via a simple move abroad are nearly unlimited.

If you want to see where your FIRE number actually goes furthest — with honest monthly budget breakdowns, not promotional estimates, across 47 cities at multiple spending levels: 47 Cheapest Cities in the World: Where Your FIRE Number Goes Furthest →

Financial independence is a tool for taking your long-term well-being back into your own hands. It lets you:

- Buy back your time and attention

- Protect yourself against future corporate restructurings, layoffs, and broken promises.

- Design a life that balances work, health, relationships, and genuine interests.

- Live, work, or retire in countries that fit your values and budget better than where you are now.

You don’t have to hate your job to care about achieving FI. You just have to recognize that relying entirely on a single employer, a single country, or a single system for your long-term security is a fragile plan, with a ceiling for your happiness.

A Glimpse of modern financial independence, in real life

Sitting in the calm of a sand-colored café on a cobblestone lane in Málaga, Alan scribbles notes between reflective pauses and slow sips of coffee. His morning has the pace of someone who could be retired, and, on paper, he is. He’ll likely never need to work again.

Still, he’s staying productive because he wants to. He’s sketching ideas for a small passion project as he’s learning about AI platforms to “vibe code” an online tool for a new generation of budget travelers. This simple project feels more engaging than his old job in finance ever did. The modest income from side projects such as this pays for small “bumps” in his normally modest yet satisfying lifestyle: an F1 race weekend in São Paulo, a sushi-making intensive in Tokyo, a long singles cruise he has circled on his calendar for later this year.

At 33, he never imagined he’d be “semi-retired,” based most of the year in southern Spain. What changed was discovering the ideas of financial independence and the tools of the FIRE movement, including variations like Lean FIRE, Expat FIRE, Nomad FIRE, and Barista FIRE that he switches between as life, his preferences, and his financial foundations sway.

Right after university, Alan learned about “financial independence,” the “FIRE movement,” and most importantly, his FI number, or the amount of invested wealth it would take for his portfolio to cover his annual expenses. At first, he assumed he would need around $1.5 million to maintain the lifestyle everyone seemed to lead in the high-cost city he first moved to out of university. That goalpost felt distant. But as he stayed focused on FI, tightened his budget, moved into a smaller apartment, cooked at home more, and ditched a car he barely used, his annual expenses fell sharply.

With more conscious consumption, he realized he could maintain a good, healthy, enjoyable life at $40,000 a year, not the $60,000 he initially estimated. That dropped his FI number from $1.5 million to about $1 million.

Then came the kicker. On a budget backpacking trip through Vietnam, Alan fell in love with cheap, rich-in-experience cities like Da Nang, Hanoi, and Dalat, underpinned by the general idea of living abroad. He noticed that in the right places, like Bangkok, Kuala Lumpur, and Tirana, he could live well on $2,000 a month or less. These potential destinations abroad implied a possible FI number closer to $500,000 if he were willing to be location-flexible.

Over the next seven years, he saved aggressively, invested simply, and experimented with short tester trips abroad. Today, while sitting in Malaga, his investments cover his core expenses. His small projects pay for upgrades and one-time luxury experiences. And his “work” revolves around curiosity and fulfillment instead of survival.

Financial independence abroad isn’t just about the number — it’s about the legal residency, banking, and tax structure you build around it. That’s the shift from “financially independent and living abroad” to something more deliberately architected: The Sovereign Expat: Building Financial Independence That Actually Holds →

My friend Alan’s life didn’t “catch FIRE” by accident. It followed a repeatable pattern: understand the financial math, change the levers you can control, and use geography as an ally instead of a prison.

The Simple Math Behind Financial Independence: Your Savings Rate & the 25x Rule

Behind every successful FI story, there are three factors:

- How much do you spend

- How much do you save

- How you invest what you save

You don’t need complex models to understand it. Two ideas carry most of the weight: your FI number and your savings rate.

Your FI Number (25× Rule and the 4% Rule)

When people talk about FI or FIRE, you’ll often hear shorthand like “25× your expenses” or “the 4% rule.”

The logic comes from research conducted by financial planner William Bengen in the 1990s, later expanded on by the so-called ‘Trinity Study’ and many follow-up studies, which tested how long a diversified portfolio of stocks and bonds could support withdrawals before being fully depleted. The finding was that if you withdraw roughly 4% of a well-diversified portfolio in the first year of retirement, and then increase that amount each year with inflation, a 30-year retirement has historically had a high probability of success.

This means, if you have a portfolio of $1,000,000, you can withdraw 4% of that, $40,000, annually.

In many of the historical periods Bengen modeled, that $1M has been enough to support ~$40,000 of inflation-adjusted spending for 30+ years.

Flip that around, and you get a rough rule of thumb for calculating the number of dollars you need for financial independence: 25x.

Your FI number ≈ 25 × your annual expenses

If you can live on $40,000 a year, your “Financial Independence number” is about $1,000,000.

If you can live on $30,000, it’s about $750,000.

If you can live on $20,000 — perhaps in a cheaper country — your number is $500,000.

That’s the simple version. For very long retirements (35–50+ years) or if you want money left over for children or causes, it’s wise to be more conservative: think 3–3.5% withdrawals, or roughly 33× your annual expenses is a smarter bet.

For now, you don’t need to memorize the exact percentages. The key takeaway is this:

Lower expenses translate to → a smaller FI number, which requires → fewer years of saving required.

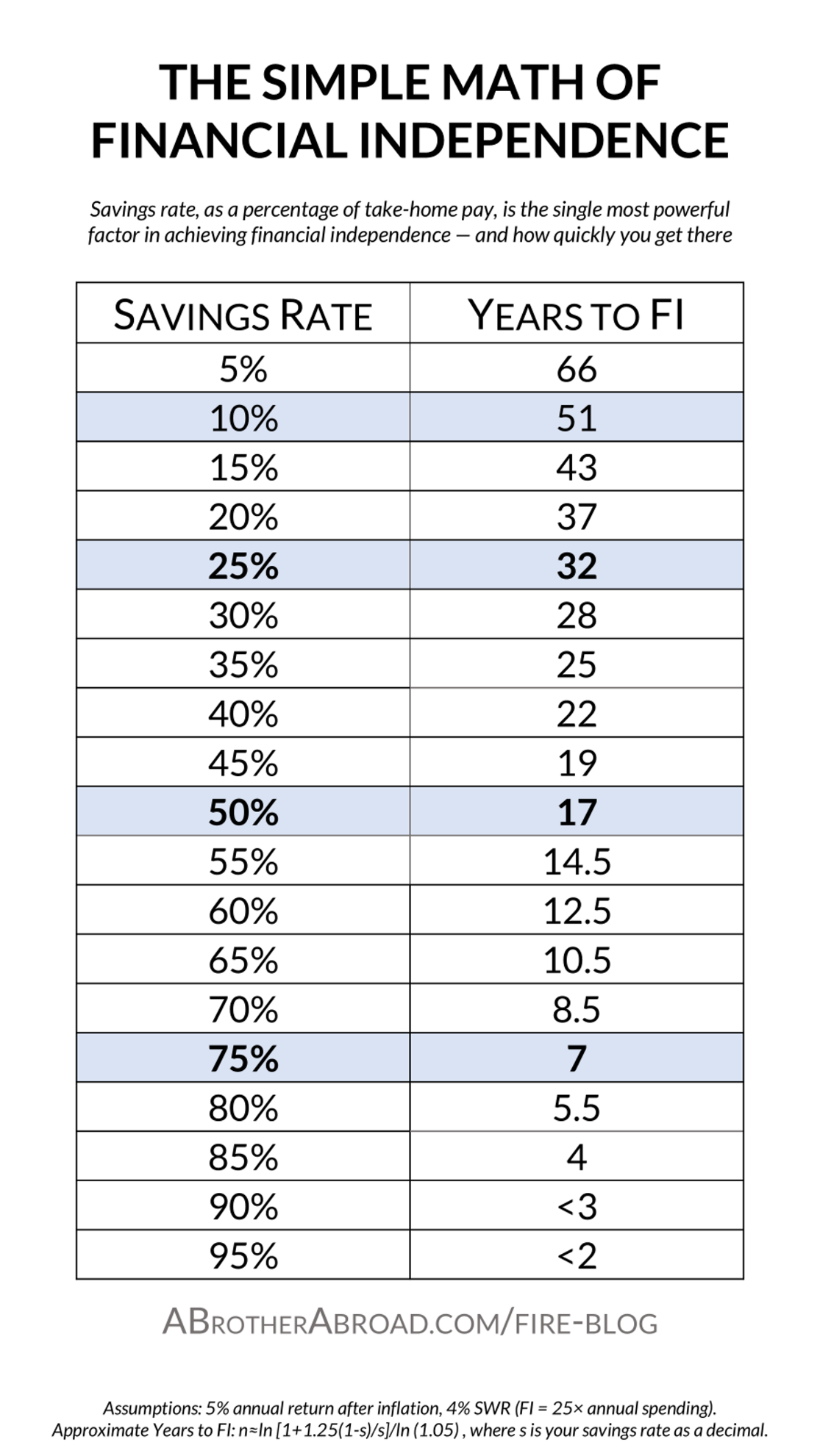

Savings rate is the real FI accelerator: Higher savings rates disproportionately speed up time to FI.

Most people are told to save 10–15% of their income for retirement. While this is better than nothing, it’s still designed to get you to a conventional retirement age, 65 or later, and assumes you plan on working for 40+ years.

If you want financial independence earlier, the math changes. Your savings rate becomes the master variable.

Your savings rate is the percentage of your income that you save. If you earn $100,000 per year and save $15,000 per year, your savings rate is 15%

Now, to understand how powerful a higher savings rate can be, think about financial independence in terms of how many years of expenses you can pay for with a year of savings.

- At a 10% savings rate, you’re spending 90% of your income, and it takes 9 years of work to save 1 year of expenses.

- At a 50% savings rate, you’re saving and spending the same amount, and every 1 year of work to save buys 1 year of FI.

- At a 75% savings rate, you’re living on 25% of your income. It only takes about 4 months to save 1 year of expenses. Ten years of aggressive saving can buy roughly 30 years of basic living expenses before investment growth even enters the picture.

While this calculation is rough and doesn’t account for how investment returns and compound interest will help you achieve your FI number, it does show why “save 10% forever” points to either very late retirement or a very meager retirement. The relationship is clear:

- Point 1: Savings rate matters massively for how soon you reach financial independence.

- Point 2: If you want to become financially independent in under 10–15 years, you’ll need to strive to save 50–70%+ of your income.

- Point 3: Cutting expenses is often more powerful and a more accessible option under your control than increasing income.

- Point 4: Every permanent reduction in spending lowers both your FI number and what you need each month once you cross the line of financial independence.

Keep in mind that in achieving those savings rates, the key skill isn’t learning to enjoy deprivation. It’s learning to build contentment, health, and happiness on a lower budget by aligning your money with what actually matters to you.

The table below shows how quickly different savings rates get you to FI.

Now, try this FI calculator to test your potential numbers and timelines for achieving FI.

How you can really become financially independent in 10 years: Save ¾ of your income

A decade to FI sounds extreme until you see the mechanics.

In very broad strokes, a 30-something with a decent income, a savings rate in the 60–70% range, and a simple investment strategy in broad index funds can get close to or reach FI in around 10 years, especially if they’re flexible about where they live.

That doesn’t mean everyone should aim for a 10-year sprint. But it shows what’s possible when you deliberately design a lower-cost life, and you aggressively capture the gap between your income and your expenses, rather than letting it leak away.

Accelerating FI by Moving Abroad

There’s another lever most traditional retirement advice barely mentions: optimizing your location, for somewhere with a lower cost of living.

This tactic applies to both achieving FI, cutting expenses to save and invest more, or crossing the FI line, moving to a location where a smaller income and a lower FI number suffice.

If your life in a major U.S. or Western European city costs $40,000 a year, and your FI number is approximately $1,000,000, moving to a country where your lifestyle costs $20,000 a year cuts your FI number to roughly $500,000.

Same person, same habits, same portfolio, but because life costs half as much in your chosen country, the amount of invested wealth you need to support it also halves. And these aren’t quality of life downgrades. You could trade living in a town in quiet Kentucky or snowy Wisconsin for the sun-soaked Mediterranean coast or the Thai tropical islands at a lower average cost of living.

You don’t have to move abroad to reach FI. But in a world where solid long-term investment returns are a bit outside your control, geoarbitrage, earning in stronger currencies or higher-paying markets, and spending in lower-cost locations, is one of the most powerful, underused levers available for quickly achieving financial independence.

We’ll come back to FI abroad later. First, let’s look at how to start moving in the right direction wherever you are.

That’s the heart of FI: your annual spending sets the target, your savings rate controls the timeline, and geography quietly multiplies (or shrinks) both.

How to become financially independent: A step-by-step guide

Now that you know what FI is and how the math works, here’s how to actually move toward it in real life.

1. Stabilize and Understand Your Financial Foundation

Before you sprint toward FI, you need a stable financial base.

- Build your emergency fund. Aim for 3–6 months of essential expenses in an easy-access account. This keeps small crises (car repairs, surprise medical bills) from pushing you back into high-interest debt.

- Eliminate high-interest and “unproductive” debt. Credit card balances and other double-digit interest loans quietly erase your progress. Make a plan to pay them down fast.

- Track your spending for 1–3 months. You can’t find your FI number if you don’t know what your life actually costs. Use a notebook, spreadsheet, or app, whatever you’ll stick with, and record your expenses honestly.

- Calculate your current savings rate. Add up what you’re saving and investing each month. Divide by your total after-tax income. That’s your starting point.

This step isn’t glamorous. It’s also the step that separates people who daydream about FI from people who eventually reach it.

2. Calculate Your FI Number and Time to FI

Once you know your annual expenses, you can do the simple FI math:

Step 1: Calculate your FI number with the 25x rule.

FI number ≈ 25 × annual expenses

(If you want to be more conservative, use 33× instead.)

Step 2: Estimate years until FI at your current savings rate.

As a rough rule, (25 x your expense rate)÷ savings rate (as a decimal) ≈ years to FI, or use the calculator here.

Step 3: Run a quick FI-abroad scenario to see if there are options to accelerate your time to FI.

Is there anywhere you could see yourself moving to in Southeast Asia, Central Asia, Southern Europe, or Latin America, and living happily?

What if you moved to a place where your cost of living fell by 30–60%? How would that change your number? Use our “Where can I afford to live” calculator to investigate options for you.

This potential approach, Geoarbitrage combined with **ExpatFIRE**, is a way to turn a vague wish (“I’d like to retire early someday”) into something concrete (“If I save like this, I’ll hit FI in ~20 years; if I increase my savings rate and/or switch locations, I can cut that to 12 years).

3. Save More (by Reducing Expenses)

There are only two ways to increase your savings rate: Spend less or earn more.

We’ll talk about earning more next, but for most people, the easier first wins come from spending less in big categories.

Focus on the big structural categories like housing, healthcare, transport, food, and tax; see the FIRE Abroad section for how these change when you move.

As a simple rule, whenever you get one-off windfalls, such as bonuses, tax refunds, or unexpected cash, save or invest most of it by default. Let lifestyle creep be deliberate and delayed, not automatic.

4. Invest in a Way That Matches Your Risk Profile

Increasing savings and reducing expenses are what move you towards FI. Investing is what accelerates your savings and keeps them from being eaten by inflation, and lets your wealth grow faster than you can by sheer effort.

Why Investing Matters: Doubles your savings every ~7 years

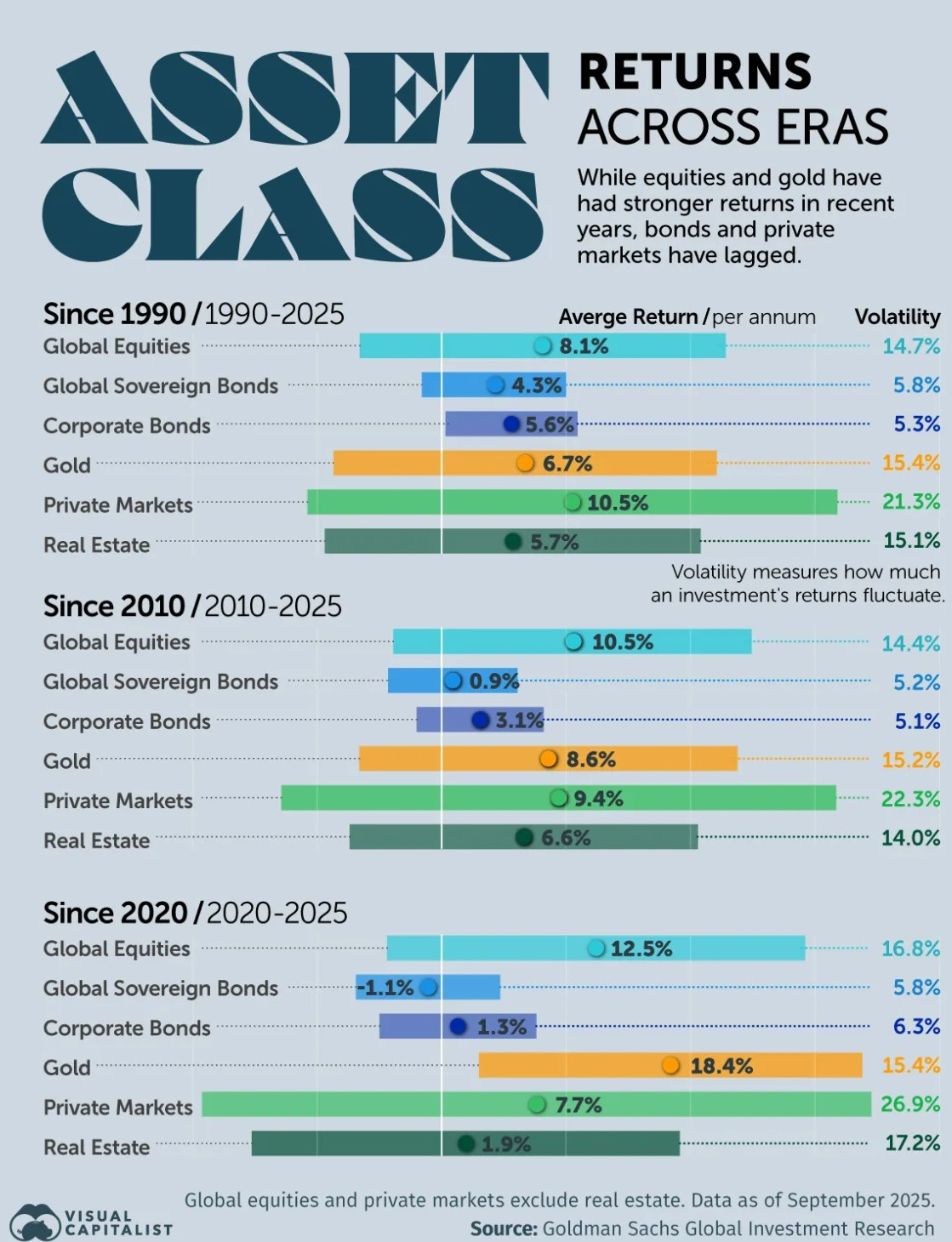

A diversified portfolio that roughly tracks stock market returns has historically doubled every ~7–10 years in real terms, thanks to compounding.

That growth helps your assets keep up with or outpace inflation, so your future self isn’t trying to live on dollars that have been degraded by inflation. The compound growth of invested savings also powers ideas like **Coast FIRE** wherein you save as much as possible (such as $250,000 now) and allow compounding interest to do the work (delivering $1,000,000 in 14 years on that same $250,000).

Investment returns also help extend the life of your portfolio once you start drawing down in FI or retirement.

Match Investments to Your Risk Tolerance

The classic FI “4% Rule” framework assumes a well-diversified portfolio, typically a mix of stocks and bonds. The exact mix depends on:

- Your time horizon

- Your comfort with market swings

- Your need for growth vs stability

However, the 4% rule is most appropriate with an aggressive portfolio of primarily stocks or ETFs covering the broad stock market, still invested in stocks. If you’re unsure if this level of aggressiveness suits your situation, it’s worth talking with a fee-only financial planner or at least doing a proper risk-tolerance assessment. The goal is simple: a portfolio you understand well enough not to panic-sell when markets inevitably drop.

The Common FIRE Approach to Investing

Within the FIRE community, the default approach is:

- Use low-cost, broad-market index funds or ETFs that track entire markets (e.g., total U.S. stock market and global stock market such as such as VTI, VTSAX, VOO, ITOT, SCHB, FSKAX, etc.).

- Keep fees low. Compounded over decades, cost differences matter.

- Hold for the long term. It’s about time in the market, not timing the market.

Looking at investment returns across the last 35+ years, this infographic shows that, historical returns could easily support a FIRE lifestyle – if the underlying investments are smart

You don’t need exotic products or daily stock picking and trading to reach FI. In many cases, those things hurt more than they help.

5. Earn More

Cutting expenses can only go so far. At some point, earning more and capturing the extra in savings instead of lifestyle upgrades, becomes the faster path.

Think in three layers:

Make your current job pay better.

- Upskill: Train new skills, take on projects that stretch your abilities, and justify raises.

- Negotiate: Don’t assume your current pay is the ceiling; ask for more as your knowledge, skills, productivity, and contribution increase.

- Seek promotions or lateral moves into better-paid roles: If your company won’t pay a raise, move to a company that will.

Add income streams.

- Freelance work in your existing skill set

- Remote consulting or teaching

- Small, simple online businesses or service businesses that fit around your main job

Books like Main Street Millionaire by Cody Sanchez, Chris Guillebeau’s Side Hustle, as well as the online business marketplace Flippa, are great resources to start exploring side income streams.

Consider “lumpy but lucrative” work.

Short bursts of intense, well-paid work (including some fly-in/fly-out jobs or contracts) followed by longer stretches of slower life and higher savings. These types of work are common and available in Australia, Norway, Canada, and Saudi Arabia in the Mining, Energy, and Offshore drilling sectors, and can pay $200,000 or more per year with meals and expenses covered.

The goal isn’t to work 80-hour weeks forever. It’s to temporarily widen the gap between income and spending, then lock in the benefits via higher savings and investment.

6. Rethink Big Commitments

Some of the biggest decisions in your life are financial decisions in disguise with long-term effects. This doesn’t mean avoid the opportunities entirely. It does mean ensuring you know how the worst-case scenarios will affect and fit your FI goals.

- Mortgages. Buying a home you’re not sure you want to live in for at least 5+ years can turn into an expensive trap rather than an investment, and immediately reduces mobility and discretionary income that could be saved.

- Marriage and partnerships. Divorce is expensive, but not the only risk. Ongoing friction around money can be mentally and emotionally taxing, stemming from incompatible beliefs about money or simple financial misunderstandings in a relationship. Understanding a partner’s financial habits, debts, and goals before you fully merge lives is both emotionally and financially wise. Being clear about FI and FIRE aspirations and commitment is equally valuable.

- Career choice. Some fields are structurally fragile or require long training for modest pay, such as teaching, social work, the arts, and the humanities. Others, like healthcare, finance, engineering, and IT, offer high income but have high potential for burnout if not planned well. For FI, aim for work that is sustainable enough to stick with while you’re saving, and resilient enough to survive industry change.

- Debt. Every time you borrow, you’re committing your future to support the present you. That’s not always bad, as some debt can be useful if used strategically and smartly, but overusing it eats directly into your FI potential and mobility.

You don’t have to optimize every decision in life purely for money. Just be aware and recognize when you’re locking in decades of financial consequences and choose accordingly.

For people building financial independence while living abroad, the rent-vs-buy decision is genuinely different than it is at home — and the math usually lands somewhere surprising: Rentvesting: The Expat Approach to Property and Wealth →

The FIRE Movement: A Fast Track Method to FI

So where does FIRE fit into all this?

What is FIRE: The Financial Independence, Retire Early Movement

The FIRE movement (“Financial Independence, Retire Early”) is a community and approach built around a simple idea:

Spend far less than you earn, invest the difference in broad, low-cost index funds, and reach financial independence decades earlier than traditional retirement. Work becomes optional once your portfolio can safely cover your spending.

It’s an internet-visible, community-shaped expression of the same math we’ve just walked through.

FIRE Principles That Are Perfect for FI

The FIRE culture has done a good job of codifying FI math into practical rules:

- Savings rate is the master variable. The more of your existing income you consistently keep and invest, and the less you spend, the fewer years you need to reach FI.

- A simple target: ~25× your annual spending. If you can live on ~4% yearly of your current portfolio, you’re effectively financially independent. For longer horizons than 30 years and goals of multi-generational wealth, many people use lower rates of 3% to 3.5%.

- Frugality is a tool, not a punishment. Spending intentionally, and often less, is how you both save more now and reduce the number you need to hit later.

- Smart, simple, long-term investing. Most FIRE folks stick to low-fee index funds that cover the broad stock and bond markets, then keep them indefinitely to avoid constant trading.

- Flexible options along the way. The FIRE approach to FI isn’t all-or-nothing. Many people pursue semi-financial independence, take mini-retirements, or downshift to less intense work once they’re partway to their number.

You don’t have to adopt every FIRE habit or identity, but the toolkit is still very useful, even if you never “retire early” in the classic sense but simply want good financial habits.

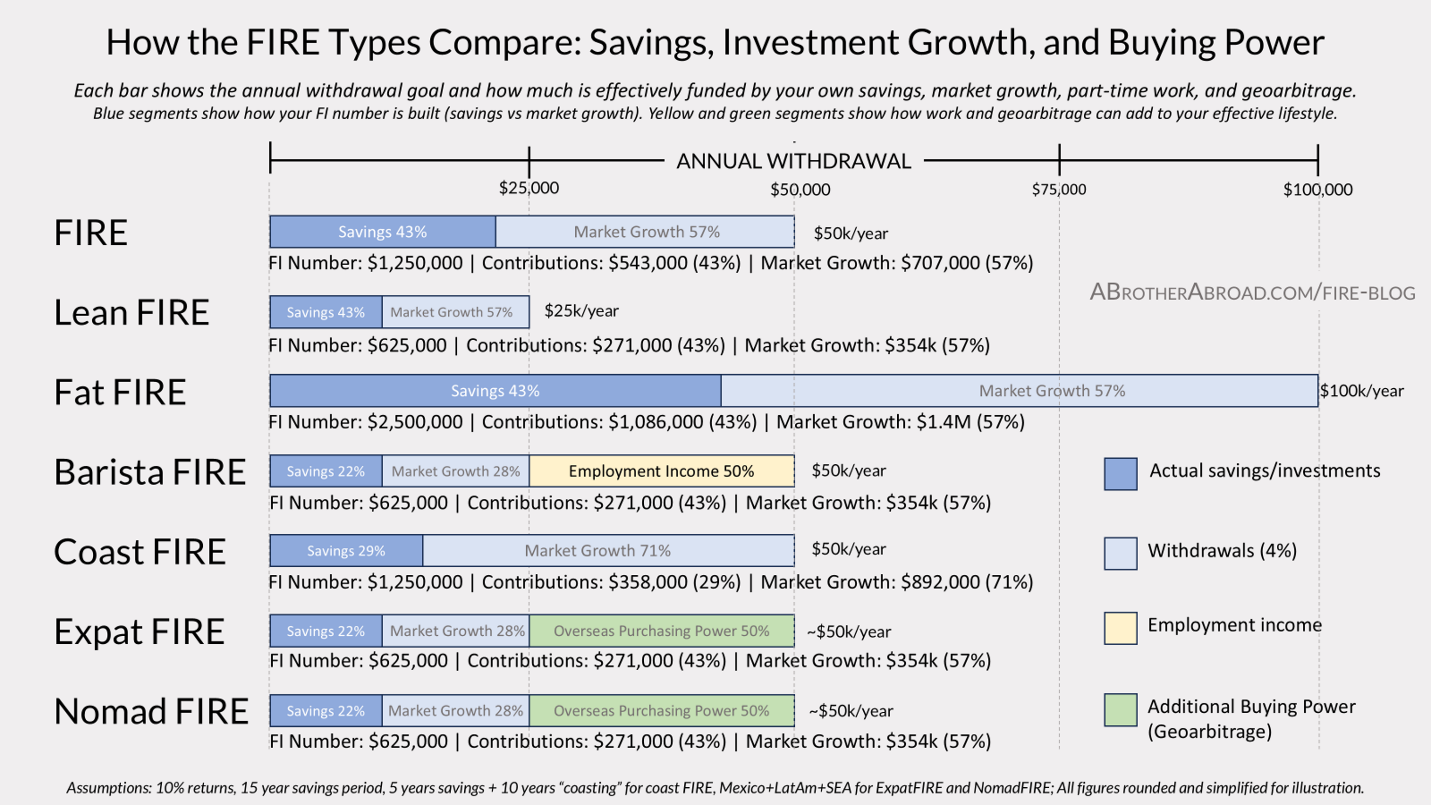

The Variations of FIRE: Barista, Coast, Lean, Nomad, Expat

Over time, the community has created several different styles of approaching FI suited to different ambitions and levels of commitment:

- Traditional FIRE: ** Full FI, often in your home country, with a middle-class lifestyle.

- Lean FIRE: ** FI on a deliberately minimalist budget, usually under ~$25,000 per person per year, often in lower-cost locations.

- Fat FIRE: ** FI with a larger budget and more slack with six-figure annual spending, private healthcare, and premium cities.

- Barista FIRE: ** Semi-FI where your portfolio covers most expenses, and flexible, part-time work covers the rest (and often healthcare).

- Coast FIRE: ** You’ve saved enough early that your existing investments can “coast” to a full retirement number without further contributions; you just need to cover your ongoing expenses.

- Nomad FIRE: ** FI combined with slow travel across countries and regions, using geoarbitrage to stretch your money.

- Expat FIRE: ** FI built around a long-term base in one (or a few) foreign countries with a favorable cost of living, lifestyle, and sometimes tax regimes.

You don’t have to place yourself in any of these boxes to get value from FI. You can simply borrow the tools and ideas that fit your life.

Myths and Realities of the FIRE Movement

A few common myths are worth clearing:

Myth: You need a huge salary to FIRE.

Reality: Income helps, but savings rate and spending matter more. Plenty of people with moderate incomes reach FI by designing lower-cost lives and keeping their fixed costs low.

Myth: FIRE means never working again.

Reality: Work becomes optional. Many FI folks “unretire” into passion projects, part-time roles, or new careers. Going back to work for a while during rough market periods can be a smart wealth-preservation move, not a failure.

Myth: You have to live an extremely frugal, joyless life.

Reality: Most successful FIRE stories are about sustainable, values-driven frugality, not suffering. People cut what they don’t care about so they can spend more on what they do.

Myth: The markets have to be perfect, or your savings and investments are doomed.

Reality: Good financial and FIRE plans include buffers, planned flexibility, and downside thinking specifically for down markets. Negative market returns occur every 3 to 5 years, so bad market years aren’t just possible, they’re inevitable, and a good FIRE plan hedges accordingly.

You don’t have to “join FIRE” and take it on as an identity. You can simply take the smart parts of the approach and quietly improve your own financial independence trajectory.

FIRE Abroad: How choosing the right location can cut your FI number and time to FI in half

Most FI discussions assume you’ll stay in your home country. But your current FI number lives in a specific currency and cost tied to a specific location. Change the location, and the number changes.

Your Two FI Numbers: FI at Home and FI Abroad

You can think of yourself as having two FI numbers:

- FI number at home = (Annual spending at home – any reliable other income) x 25

- FI number abroad = FI number at home × % cost of living factor for the country or region you choose

For example, if your life costs $50,000/year in a major U.S. city and you’re using a 4% withdrawal rate, your FI number is roughly $1.25 million.

Now, in Mexico, the cost of living is on average 50% of the cost of living in the US. If you can live a similar or better quality of life on $25,000/year in Mexico, or another well-chosen place abroad, your FI number for that same lifestyle as home could fall to about $625,000 or less.

Same person, same skills, different FI target, simply because the cost location changed.

By the Numbers: How Much Cheaper Life Abroad Can Be

Numbers will vary by city and lifestyle, but as broad examples:

- In parts of Thailand, many expats live comfortably for 40–60% of the cost of a comparable U.S. lifestyle.

- In Mexico, it’s common to see total costs 40–50% lower than in a major U.S. metro, especially outside the most tourist-saturated hubs.

- In Portugal, many people report 30–40% lower overall costs than in expensive U.S. or Northern European cities, especially once housing is optimized.

The following is a table of the average cost of living in the 20 most popular countries with expats, displaying how much the cost of living is compared to the US cost of living, and roughly what $75,000 of living expenses in the US look like in these 20 countries/

|

Cost of Living Adjustments Around the World | ||

|

Country |

% of the US for the average cost of living |

Sample Annual COL (Based on $75,000 in the US) |

|

USA |

100% |

$75,000 |

|

Mexico |

50% |

$37,500 |

|

Thailand |

39% |

$29,250 |

|

Indonesia |

39% |

$29,250 |

|

Bali |

65% |

$48,750 |

|

Vietnam |

29% |

$21,750 |

|

Colombia |

44% |

$33,000 |

|

Peru |

45% |

$33,750 |

|

Chile |

48% |

$36,000 |

|

Morocco |

47% |

$35,250 |

|

South Africa |

48% |

$36,000 |

|

Spain |

61% |

$45,750 |

|

Italy |

75% |

$56,250 |

|

Portugal |

63% |

$47,250 |

|

Croatia |

64% |

$48,000 |

|

Albania |

48% |

$36,000 |

|

Georgia |

49% |

$36,750 |

|

Uzbekistan |

48% |

$36,000 |

|

Dubai |

100%+ |

$75,000 |

|

Malaysia |

40% |

$30,000 |

|

Panama |

62% |

$46,500 |

|

Costa Rica |

61% |

$45,750 |

Data Sources: Expatistan, Numbeo

What FIRE Abroad Actually Looks Like

FIRE abroad isn’t a single, inflexible idea. It can look like:

Lean FIRE abroad: A minimalist, nature and outdoor-oriented lifestyle in a low-cost town in Mexico, Eastern Europe, or Southeast Asia, living well on $1,500–$2,000/month, with plenty of free time and simple pleasures.

Expat FIRE: A stable base in a country like Portugal, Spain, Malaysia, or Thailand, often with a long-stay or retirement visa, a local community, and maybe a small side project or business.

Nomad FIRE: Slow travel through high satisfaction and low cost regions like Southeast Asia, Latin America, or Eastern Europe, spending 2–3 months in each place, stitching together the best of multiple locations while keeping overall costs far below what one would experience in a U.S. big city.

If any of those possibilities interest you, FI isn’t just a number. It’s a way to open doors to lives that are hard to imagine from a cubicle.

Financial Independence vs Financial Freedom

People often use “financial independence” and “financial freedom” interchangeably, but there’s a useful distinction that can help shape your short-term and long-term financial goals.

Financial independence means your needs and current lifestyle are covered by your assets and passive income. Essentially, you can maintain your current quality of life without working.

Financial freedom implies a step beyond: your needs plus your major wants and options are covered. You have the slack to radically upgrade your lifestyle, take big risks, and say “yes” to expensive dreams without worrying about money.

FI might mean your existing life, or a leaner, more intentional version of it, is fully funded.

Financial freedom could manifest as upgrading locations to premium global cities at will, funding more travel, education, or philanthropy, or even deciding to live more comfortably or be more generous, and have the means to do so without concern or worry.

You don’t have to chase full “freedom” for your life to change dramatically. Reaching plain FI, the point where work is optional, and you’re no longer financially fragile, is already a profound shift and a wonderful stepping stone. The independence, free time, and free mental space FI affords you could become a platform from which you build to full financial freedom.

How realistic is FIRE?

For proactive savers who are willing to:

- Learn the basics of the math behind achieving financial independence

- Take an honest look at their spending

- Make some structural changes to housing, transport, and work

- Use geoarbitrage and change to a better location, if it suits them

…achieving a version of financial independence in 10–20 years is realistic.

That doesn’t happen by accident or by stuffing a few extra dollars into a high-yield savings account. It happens by deliberately designing your finances, your lifestyle, and eventually your location around a goal.

Key Principles in Achieving Financial Independence: Discipline and Flexibility

Two important traits make FI plans durable:

Discipline. It’s not complicated to spend less than you earn, invest the gap, and avoid lifestyle creep. It is hard to do those things consistently over 10 to 20 years. Systems help: automatic transfers to investment accounts, pre-commitments to save raises and bonuses, and clear “rules” for yourself.

Flexibility. Your preferences, health, family, and opportunities will change. Build slack into your plan. Allow for course corrections. Being able to move cities, change housing arrangements, or take up part-time work again can turn what looks like a crisis on paper into a manageable, and even enjoyable, adjustment in real life.

Keep these in mind as we review the major risks and concerns with FI, and how to deal with them.

Concerns, Risks, Trade-Offs, and Flexible Safety Nets

No serious FI discussion is complete without the caveats.

“Those savings rates look impossible for me.”

For many people, especially early in a career or in low-wage work, a 50–70% savings rate feels, and likely is, unrealistic. That doesn’t mean FI is off the table. It means your early focus may need to be on establishing the foundations of your FI engine while taking advantage of structural changes in life that create financial breathing room.

- Build skills to move into better-paid roles.

- Consider relocating (within your country or abroad) to a place where your income stretches further.

- Consider work opportunities that cover living expenses, offering food and housing for living on site, such as “Fly In Fly Out” (FIFO) work or a travel version of your current work.

- Start with modest savings improvements to establish the habit, and let compounding investment interest and career growth work together.

- Start early. Starting seven or ten years earlier can dramatically reduce how much you need to save later, because compounding has more time to work.

Even moving from a 5% savings rate to 20% is a major leap, so start small and early and aim to increase incrementally and steadily.

FI and FIRE often require consistent frugality and lifestyle changes: smaller spaces, fewer status purchases, a different social rhythm. If that feels like pure deprivation to you, it won’t be sustainable.

The goal is not punishment. It’s to align spending with what genuinely makes your life better and cut what doesn’t.

“I have a family/partner, and we’re not all on the same page.”

FI is hard to pursue alone if you share housing and major expenses with someone else. It’s also not something you can spring on people after the fact. The mindset shifts and habits required for FI run counter to most social norms around money. Because of this, FI and FIRE habits can’t be forced on anyone, and one person can’t do all of the work when two people create the financial situation. This is where honest conversations matter and are required. Discuss what you want life to look like, what trade-offs you’re willing to make, and what you’re not willing to sacrifice.

Sometimes the answer will be “Not yet.” That’s okay. You can still build better habits, pay down debt, and quietly strengthen your position.

Market Risk and Sequence of Returns

“What if markets underperform?”

They will, at times. That’s baked in. The stock market has returned negative returns once every three to five years over the last century, and it will happen again. You can’t control the market, but you can plan for it.

Markets don’t move in straight lines or forever upward. On average, you can expect negative years every three to five years, and occasionally clusters of them, according to Kiplinger and Capital Group.

A particular risk in retirement is sequence-of-returns risk, which is essentially hitting a streak of bad markets early in your withdrawal period. If you’re pulling 4% a year from a portfolio that’s simultaneously down 30%, the damage compounds as you “lock in” losses that would have otherwise recovered.

Ways to manage this include:

- Keeping a 1–2 year cash or short-term bond buffer to live on during bad years

- Be flexible in your spending, dialing back when markets are rough and loosening up after strong runs, and being willing to temporarily reduce withdrawals during deep downturns.

- Using more conservative withdrawal rates (e.g., 3–3.5%) if you want higher confidence over long horizons

A good FI plan assumes there will be bad years and gives you dials and emergency buttons to adjust when less desirable market conditions inevitably come.

Ultimately, for investment planning and withdrawal planning, consult a fee-only financial planner to review the viability and risk of your financial plan.

Healthcare and Medical Surprises

“What about healthcare?”

In many countries, healthcare is one of the biggest wildcards in retirement, but it is still something we can plan for.

Planning effectively for healthcare in FI means:

- Prioritizing health, fitness, and preventative care for a longevity-focused lifestyle, as these are the cheapest healthcare options and “health insurance additions” long term. Consider keeping or building health-relevant habits (fitness, diet, stress management) as part of your FI strategy, not separate from it.

- Understanding your home country’s system (and gaps), and intentionally accounting for them

- If you’re abroad, learning how local public systems, private insurance, and international health plans work.

- Recognize that healthcare needs and costs often increase with age, and build that into your FI number and withdrawal plans.

- Factor realistic healthcare costs into your FI number. Don’t go for cheap, go for quality and the safety net suited to your health, your situation, and your life.

- Understand how healthcare coverage works in any other country you plan to live in, both public healthcare, travel insurance, and your private healthcare of choice.

The Possibility of Unretiring: A great safety valve in FI

One of the quiet truths about FI is that many people end up working again. They do so not because they have to, but because they want to and because it is a great, optional lever to maintain as FI.

Sometimes that’s for financial resilience: picking up part-time work during prolonged market downturns to reduce portfolio withdrawals. Sometimes it’s for a purpose, structure, or social connection.

The best way to maintain the option of “unretiring” on your terms is:

- Maintain at least one marketable skill even after you hit FI

- Continue learning and adding new skills to your toolbox, as the world, technology, and industries change

- Stay mentally active in your craft, whether paid or unpaid

- Keep your professional network warm

- Follow your curiosity into side projects that could, if needed, be turned into income

One of the hallmark findings in studies of centenarians in blue zones was that they often never truly retire and practice a trade for life, which gives life purpose and keeps them pleasantly engaged in the world they live in. FI gives you the option to pick that activity deliberately.

Changing Needs Over 30–50 Years

Your life at 35 will not look like your life at 65 or 75. Needs, tastes, family situations, and health will change. The sacrifices you are willing to make now may be unthinkable in your later years, and the compromises in location and lifestyle may not be possible as you age. Financial independence is not a worthwhile prize if it traps you into increasing misery, so plan for changes in life so that you can age and grow comfortably and gracefully.

Your FI plan should be a living, revisable guide, not a rigid script. Check in regularly and ask:

- Are your expenses still what you expected?

- Has your health situation changed?

- Do you still want the same lifestyle or location?

How to Get Started This Month

If all of this feels a little too abstract, here is a simple plan to help you get started:

- Track your spending for 30 days to get a clear baseline and full picture of your expenses. Multiply by 12 to get your annual expenses.

- Calculate your FI number (25× your annual expenses), calculate your current savings rate, and calculate your number of years to FIRE.

- Build or top up your emergency fund to at least 3 to 6 months of expenses.

- Attack one ugly piece of high-interest debt.

- Pick one lever to reduce expenses (housing, transport, food, subscriptions) and one lever to increase income (small side project, negotiating a raise, extra shift).

- If you’re curious about living abroad, run a “FI abroad” scenario for one or two countries you genuinely like the idea of and compare the numbers.

A note on becoming tax literate

Remember: investment gains are taxed, even if you’re abroad; retirement accounts have their own rules and penalties; capital gains and dividend rules vary by country. A bit of tax literacy early on can save you a lot later.

Useful Tools and Next Steps

- Use the FI / FIRE calculator on this site to run your numbers and hand calculate your FI number to test scenarios (“What’s Your Number”).

- Read the deep-dive on FIRE Abroad: How Moving Overseas Can Cut Your FIRE Number in Half for more on geoarbitrage, visas, and cost of living. **

- Explore the guide “Which Type of FIRE Abroad Is Right for You? Lean, Coast, Barista, Nomad & Expat FIRE” to see which path best fits your personality and circumstances. **

- If living abroad is part of your plan, dig into the visa and long-stay residency resources to understand the legal and bureaucratic side of building a life elsewhere.

Financial independence isn’t about hoarding money for its own sake. It’s about building enough stability and flexibility that you can live where you want, do work you care about (or none at all), and spend your time on the people and experiences that matter most.

You don’t have to become a finance nerd or move to a cabin in the woods. You just have to understand the math, choose your levers, and give your future self the kind of life your present self wishes you had more time for.

Other Great Articles in the Financial Independence and Global Mobility Series

Guides to Achieving Financial Independence

- How to achieve Financial Independence & Retire Early

- Barista FIRE Guide: Semi-Financial Independence

- Expat FIRE Guide: Living abroad with geoarbitrage to retire early

- Nomad FIRE Guide: Achieving financial independence by traveling around the world

- Coast FIRE (Coming Soon)

FIRE Calculators

- FIRE Calculator | How much do you need to retire early?

- Expat FIRE Calculator

- Nomad FIRE Calculator

- Lean FIRE Calculator

- Coast FIRE Calculator

- Barista FIRE Calculator

.

.

ABOUT THE AUTHOR

Carlos Grider launched A Brother Abroad in 2017 after a “one-year abroad” experiment turned into a long-term life strategy. After 65+ countries and a decade abroad, he now writes about FIRE, personal finance, geo-arbitrage, and the real-world logistics of living abroad—visas, costs, and tradeoffs—so readers can make smarter global moves with fewer surprises. Carlos is a former Big 4 management consultant and DoD cultural advisor with an MBA (UT Austin) and Boston University’s Certificate in Financial Planning. He’s the author of Digital Nomad Nation: Rise of the Borderless Generation and is currently writing The Sovereign Expat.