Here’s how to Make It Happen in Your 20’s, 30’s, and 40’s…

Financial independence is something many people dream of but few people realize is possible. However, the fast-spreading FIRE Movement is quickly sharing financial independence savvy and the ability retire with everyday people like you, and me.

With all of the “get rich quick” pitches from fake gurus, cryptocurrency scams, and disastrous world events with major economic impact on a global and personal level, cynicism about the possibility of financial independence is justifiable. Luckily for us, financial independence is more possible than ever (thanks to the internet, free information, and the investment opportunities it makes accessible) and achievable for the average person. A fresh wave of old-fashioned thinking and personal financial management approaches are catching on…like FIRE…and its making the path to financial freedom more accessible than ever.

The Financial Independence Retire Early Movement, also known as the “FIRE movement” is a philosophy on personal financial management aimed at retiring early, as soon as your late 20’s or 30’s, by using frugality, spending awareness, and time-tested investment approaches. To date, thousands of members of the community have reported reaching financial independence by following a handful of principles, and learning a few new budgeting and spending management approaches. The entire movement revolves around openly sharing knowledge on how to live a more financially healthy and efficient lifestyle.

Unfortunately, this kind of simple financial savvy isn’t taught in most schools, and most families don’t have the generational knowledge or wealth experience to teach children and young adults how to properly save money, avoid debt, reduce expenses, invest in income generating assets, and reach financial independence.

Fortunately, thousands of others have learned the knowledge, applied the knowledge and reached a financially independent status, and I have been lucky enough to learn from them. Now, in this complete guide to the Financial Independence and Retire Early Movement, I will share everything you need to know to get started on your own path to financial health and financial freedom.

Disclaimer: This content is for educational and informational purposes only and is not individualized financial, tax, or legal advice. I don’t know your personal situation, and reading this does not create an advisor-client relationship. Consider consulting a qualified professional before making financial decisions, and invest based on your goals, time horizon, and risk tolerance.

Assumptions Notice: Examples and calculator outputs are hypothetical, based on user inputs and assumptions (e.g., returns, inflation), and actual results will vary.

This article contains affiliate links

Contents of this Guide to the Financial Independence and Retire Early Movement

- What is the “FIRE Movement”?

- What is Financing the Escape: Using location independence and geoarbitrage to live better, and retire earlier

- Tenets of FIRE (Financial Independence and Retiring Early)

- The Tenets of FTE (Tenets of Financing the Escape)

- How money much do you need to retire?

- FIRE Lifestyle FAQ

- Next Steps: A Tactical Checklist for Achieving Financial Independence

I’ll start this article with two very clear statements about the FIRE movement and why this article is worth reading.

1. I am semi-retired, and fully financially independent. You can trust that I’ve practiced what I’ll be sharing.

2. I achieved financial independence by following the “FIRE movement” methodologies, short for “Financial Independence and Retire Early” movement.

3. I sped up the process of reaching financial independence with a little tactic called “geoarbitrage” and by building and cultivating location independence in my life

I did not share that information to brag. I shared the information to validate the value of the ideas I am going to share with you in this article detailing what the Financial Independence Retire Early movement is, what is financially possible and how it can be achieved.

Click here to jump straight to the tenets and steps in the FIRE movement and Financing Your Escape

As I write this, I sit in a cute little hotel in Penang, Malaysia where, after this, I’ll wander, eat, and write before returning back home to my villa in Bali for a few months. I’ll relax, write, and surf there before leaving to Japan to repeat the process. This is my life, thanks to the FIRE movement and what I learned from the community, financial freedom, and geoarbitrage (the means by which I financed my escape, from the corporate world and to…well…wherever I want to be actually).

Anyone can do the same by following a few principles diligently over the long term.

Let’s get started.

What is The “FIRE Movement” and “Financing the Escape”?

The “FIRE movement”, or Financial Independence and Retire Early movement, is a lifestyle movement aimed at achieving financial independence and early retirement by reducing expenses and living a frugal lifestyle, saving a high percentage of income and investing the savings into assets that generate passive income.

The goal of each person in the movement is to accumulate enough savings and investments to retire from traditional employment, thus leaving them to pursue passions or hobbies as they choose, without worrying about financial constraints.

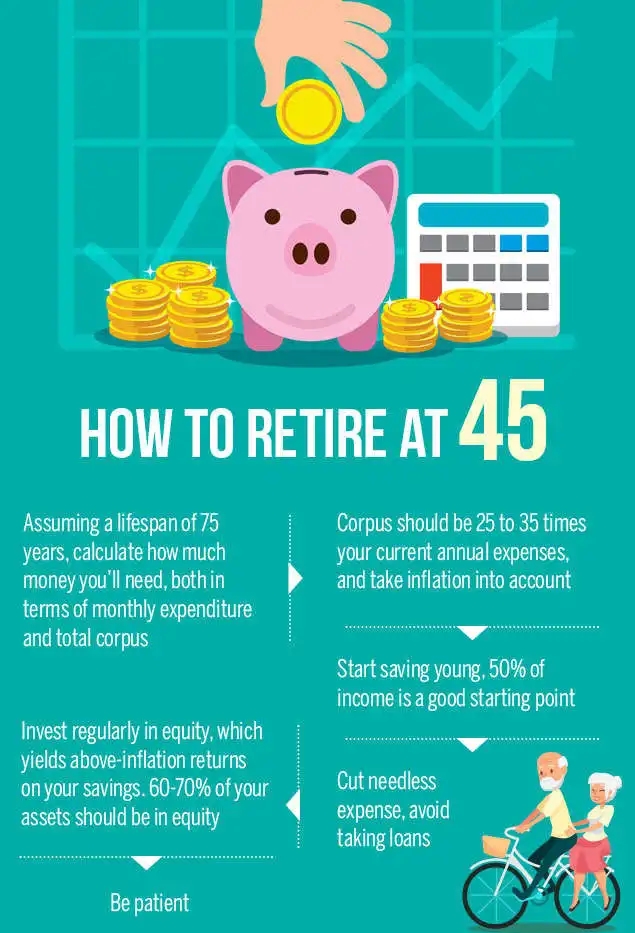

The FIRE movement’s driving principle is that by living below one’s means and investing the savings to achieve assets worth 25x annual spending, individuals can achieve financial independence and (if they choose) retire early, in their 30s or 40s or earlier instead of the commonly accepted age of 62 to 67.

The FIRE movement is underpinned by the importance of financial education, frugality, and long-term planning to achieve financial independence. All of this is supported by the shared knowledge and support of within the community of FIRE followers who actively share experiences, lessons, and developing insights as the economy and world changes.

I highly recommend joining the completely free Reddit r/FIRE community for active support, engagement, and education on frugality, saving, investing, and retiring early as you start the journey as this community was the figurative match that lit my FIRE. You can read all about FIRE followers’ experiences just starting on the road to financial independence, sharing their progress years in, and sharing as they retire financially independent.

For Americans reaching financial independence and planning to live on passive income abroad, there’s a visa category built specifically for this situation — and it’s often more practical than digital nomad visas: Retirement Visas for Americans: 11 Options Worth Considering →

What is “FI” (Financial Independence)

In the context of the FIRE movement, “financial independence” is having accumulated enough savings and passive income-producing investments to cover one’s living expenses indefinitely without having to rely on traditional employment or a regular paycheck. This means that individuals who have achieved financial independence have enough assets generating passive income to cover their expenses and sustain their chosen lifestyle.

individuals who have achieved financial independence have enough assets generating passive income to cover their expenses and sustain their lifestyle indefinitely

Practically, financial independence is having enough passive income-producing investments (such as stocks or index funds), businesses that you own but do not actively manage (such as franchises or automated online businesses) real estate, etc., to pay for your reasonable living expenses for the rest of your life.

With “FI” you have the freedom to do as you wish with your time, within reason. Working, full or part-time, or engaging in income-generating hobbies are optional at this point.

It’s worth noting that the amount a person must achieve to be financially independent, also referred to as the “FIRE number” varies depending from individual to individual, based on each individual’s personal goals, chosen lifestyle and respective costs, and personal circumstances. However, a rule of thumb is that financial independence can be achieved by saving 25 times the amount of a person’s annual expenses and investing that money in index funds or ETFs, according to the 4% rule. With these funds and investments, a person would be able to withdraw that amount every year indefinitely.

(Click to jump to more on achieving Financial Independence )

(Click to return to the table of contents)

What is “RE” (Retiring Early)

In the context of the FIRE (Financial Independence Retire Early) movement, “retiring early” means leaving traditional employment, as it is no longer a requirement for survival thanks to achieving enough passive income from investments to cover one’s living expenses.

While the traditional retirement age is often around 65 or later, followers of the FIRE movement aim to retire as early as their 30s, or 40s.

Retiring early does not necessarily mean not working at all. Rather, it means having the financial freedom to choose to pursue work, activities, or passion projects that are more fulfilling or meaningful. This might involve starting a business, working part-time, or volunteering, for example.

Many studies have drawn the connection between longevity and continuing a profession well into old age, as it can add fulfillment and “purpose” in life. This means that if you enjoy what you do for a living there is no reason that you shouldn’t do it. However, financial independence merely allows one to pursue employment for enjoyment and fulfillment, and leave as their preferences and circumstances change. “Semi-retirement,” solely for fulfillment, could involve seasonal employment, advisement only as a consultant or member of a board, or even transitioning to a part time teaching role.

The concept of “retiring early” and the best way to do it should and will vary between individuals based on personal goals, ambitions, passions, and life circumstances. Some early retirees may choose to continue working part-time. Some people may want to maintain traditional forms of work at the job they’ve always worked at simply because they enjoy it. Others may even choose to take a break from work entirely for a period or indefinitely and travel the world.

If your career is your passion, then there is no need to retire, but financial independence is still valuable and worth achieving

At the end of the day, if you are able to do what you love to do for the simple experience of doing it, not for the compensation, you will have more flexibility in accepting opportunities that fit your desires, passions, and purpose. Additionally, having the freedom of choice that comes with financial independence will allow you to weather downturns in your chosen profession, or if conditions become less than enjoyable, step away from the profession in “semi-retirement” while you pursue other passions with the option of returning later.

Nonetheless, the basic idea of achieving financial independence and having the freedom to pursue one’s passions or interests is the key goal of the FIRE movement.

(Click to jump to more on Retiring Early )

(Click to return to the table of contents)

What is “Financing the Escape”: Using location independence and geoarbitrage to save more, live better, and retire earlier

The “Financing the Escape” approach is a fairly new, fast-spreading idea that suits a subset of the population who love the ideas of travel, the expatriate lifestyle, and generally going abroad. The approach to living and saving more underpins the current digital nomad movement.

While the FIRE movement has been around for quite some time, the new concepts of remote work, digital nomads, and “Insta-envy” have done a great job spreading knowledge of the possibilities and happiness that can be achieved with a location-independent lifestyle and “geoarbitrage,” two tools that can be used to achieve financial independence faster.

The FIRE movement and tenets of eliminating debt, saving money, and investing that saved money do a great job of empowering us to build a large pile of assets. However, the one possibility the tenets underplay is how much quality of life can be improved, and how much additional money can be saved by simply moving outside of your own country, or to a lower-cost part of your own country.

Location independence: Building the financial resources, knowledge, and logistics in your life to move to or live anywhere

With the Financing the Escape approach, we go a step further by actively cultivating location independence in our lives.

Location independence is having the financial resources, logistical resources, and knowledge we may need to move our lives to a new city or country at will for short or longer periods, as often as we choose.

Cultivating location independence is much more than simply amassing financial resources. Location independence involves cultivating a mindset in which you are comfortable moving to a new city or country for a few months, a few years, or for life while thriving and enjoying the experience, as well as setting up the logistics for living abroad comfortably and legally (bank accounts, virtual mailboxes, international tax law friendly accounts, minimal items in your storage unit, visas, etc.).

Location independence is probably the most powerful tool in our arsenal because it works so quickly and so effectively in improving quality of life, reducing costs, and increasing savings when used with “geoarbitrage.” One flight to the right location can lower your cost of living and improve your quality of life immediately.

(Click to return to the table of contents)

Geoarbitrage: Moving to a cheaper location to improve your quality of life and save more

In the “Financing the Escape” methodology, the newfound resources gained through FIRE, assets, investments, and the passive income they create, are used to finance moving to a different location where your hard-earned dollar or Euro has much more buying power than it does back home. Every dollar or Euro buys more house, more food, and more resources if it is spent in the right country or city. This is a concept known as geoarbitrage. We can use geoarbitrage as an accelerator for saving to speed up our journey to financial independence.

Practical examples range from moving domestically, from say Milan, Italy, where the cost of living is $6,307 per month to Lake Como, Italy, where the cost of living each month is $3,063 saving you $3,000+ per month, while still living an amazing lifestyle.

Or, moving from the beautiful beachy town of San Diego, California, where the cost of living is $5,545 per month, to the still beachy and beautiful Canggu Bali, where the cost of living is only $2,039, saving you $2,500+ per month!

The benefits of geoarbitrage go beyond the simple costs of living and potential savings, as you can choose locations that deliver what you want and need in life.

For older retirees, in a period of their lives when healthcare matters more than ever, moving to Malaysia from the US where healthcare costs are ¼ the healthcare prices in the US, the move could change the quality of retirement immensely.

For active lifestyle types like myself, moving from the frigid waters of San Diego for warm surf in the Indian Ocean in Bali** or nearby Sri Lanka** a few months a year before returning home could be a dream come reality.

Imagine moving to tropical Southeast Asian islands for the European or North American winter to sun and surf your way through what would otherwise be a potentially miserable and frigid season. Or sculpting your life to move with events, moving to Italy during the grape harvesting season, or to Brazil for a month to soak in the build-up to Mardi Gras, or to Patagonia for the spring to trek through the many national parks.

This is the final step of “the escape” achievable only after building location independence, choosing destinations to shape the life of your dreams and add elements or activities of value to you. This could all be made possible by the financial resources accumulated by fire, and the logistical resources, and practical knowledge of how the ability to move temporarily created by cultivating location independence.

The abroad multiplier only works if you have a legal way to stay. For people reaching financial independence and planning to live on passive income, retirement and passive-income visas are the structures built specifically for this situation: Retirement Visas for Americans: Where to Retire Early Abroad →

(Click to jump to more on Geoarbitrage)

(Click to return to the table of contents)

Now that you understand what we are trying to achieve – financial independence and location independence for a higher quality of life – let’s look at the specific tenets and tools of FIRE and FTE.

Namely:

- Avoiding and eliminating debt

- Reducing expenses and saving

- Increasing income

- Investing

- Geoarbitrage

- Location independence

(Click to return to the table of contents)

Tenets of FIRE (Financial Independence and Retiring Early)

There are four essential tools for reaching financial independence within the FIRE approach. Each tool acts as a lever in achieving financial independence. The more you leverage them, the quicker you will reach financial independence.

The tools (and tenets) of FIRE are:

- Avoiding and eliminating debt

- Reducing expenses and saving

- Increasing income

- Investing in passive income and low-effort income-producing assets

All of these elements serve an essential driving idea behind FIRE:

The two ways to achieve the income and savings required by financial independence are to 1) earn more or 2) desire and consume less.

Avoid and Eliminate Debt

In life, we each have a figurative bucket with which we can collect assets and resources throughout our lifetime. As we earn money or resources, we can place them in the bucket to spend or use later. At some point, if we accumulate enough money or resources in that bucket, we won’t have to worry about actively placing anything in that bucket (i.e., working and actively earning) and we can trust that what we need will be there, in the bucket, when it’s needed.

Debt is the equivalent of a hole in the precious bucket where we store our financial resources. Because debt requires active repayment over time, and because many forms of debt (short term loans, credit cards, etc.) encourage only paying interest and fees and never paying down the principal, most debt is a leaky hole in our bucket – draining our resources 24/7.

The average American’s debt consumes 9.5% of their income, nearly as much as a good return from the stock market

According to the Federal Bank of St. Louis, the average American household spends 9.58% of their monthly income on debt repayment (Source). This is a tragedy because 10% annual returns from the stock market are considered good, meaning even if you win in the stock market, if you are the average American, you could be losing most of those precious monetary gains before they even touch your account.

Unfortunately, this fact may be new news to you because debt, and acceptance of it as benign, is so common in American society. Very rarely does anyone encourage the consumer to question how debt can impair a long-term financial plan. If this debt is used to finance the purchase of assets that generate income or financial gains beyond the cost of debt (such as an investment property, a home, or a business) then the debt could be beneficial. However, if the debt finances consumed purchases that bear no long-term benefit, such as a nice dinner out, a cruise, or a vacation, it’s a recipe for financial disaster.

If you plan to work at your 9 to 5 until you die, you’re confident your company will never fire you, and you have no intention of leaving your job/town or improving your life at all, debt is less of a risk to your life. But even then, it is still a risk.

However, if you desire to become financially independent or to retire early, unchecked and non-strategic debt is likely poison to your long-term plans.

Debt is a current expense that future you will have to pay

The worst aspect of debt is that it is screwing the future you not the current you.

“Current you” gets to live happily and carefree with the instant cash injection debt provides, living beyond your current means.

Future you is the one that gets to open the credit card statement and figure out the problem potentially years down the road of how to pay for a purchase in the past. Plus, this repayment could still be happening after whatever you’ve purchased with debt has become obsolete – that old TV, that iPhone that gets replaced every year, or those clothes that are “out of style” within a year.

This is the figurative equivalent of arriving at a fancy restaurant with empty pockets, ordering a lavish meal, and leaving, telling the waiter “My friend is coming later, he’ll pay for it.” Except, that friend is you. Future you.

You may get a huge pay raise or annual bonus at the same tie the credit card statement comes, fully covering the expense. Or you might not. Later, you might stumble on an investment opportunity that you would have preferred to use that “credit card money” on. Or you may not. And you may wish you’d saved money by skipping the fancier car, the bigger TV, the new table financed on credit. Or you might not.

The Solution to Debt: Avoid debt via proper planning, patience, and prudence (hunt for an alternative). Before purchasing, ask yourself “Do I really need this?”

Most things purchased on credit and financed with debt, outside of essential and lifesaving medical procedures, aren’t absolute needs at that exact moment. With proper financial planning and budgeting, we likely have enough cash to purchase something that will suffice in the moment and for plenty of time to follow. It could be a more modest car, a smaller apartment, or a non-flagship smartphone. The upgrade and luxury are what push us into that “need to borrow” category.

Instead of opting into the “borrow” category, try these expenses and debt avoidance tactics:

Cultivate patience. By being willing to wait another month or another year for that upgrade (when we may have already earned the cash), we dodge the need to borrow today.

Cultivate contentment, and a mindset of satisfaction today. By realizing that what we have in front of us will do for now, we resist that initial urge to swipe the credit card to purchase the unnecessary.

Live below your means. If your lifestyle costs more than your income, make structural adjustments to your lifestyle. Don’t pin the bad planning on the future you by borrowing today.

If there are people in the world surviving on $5 a day and, though it is extremely and unquestionably difficult, they manage to smile through it, you can manage without borrowing…from future you.

Prioritize debt repayment. If you have debt, make it a priority to pay it off as quickly as possible. Though it likely requires sacrifices in the short term, the long-run freedom created will be well worth the sacrifice. Additionally, the pain of early debt repayment will lock in some great lessons about financial management and the pain that debt creates.

Fees on debt for short-term loans and credit cards outweigh the benefits of most reasonable consumer investments, making debt repayment the most urgent part of your financial plan

Avoid new debt. Once you have paid off your existing debt, avoid taking on new debt. This will allow you to maximize your savings and invest for the future, bringing you one step closer to achieving financial independence.

Common forms of debt to be wary of:

- Credit cards: If you cannot pay your balance down to zero by the end of the month, don’t use the card

- College loans: If the loan is not financing a career with ample opportunities for hiring and growth and salary that allows quick repayment, reconsider. Instead, look into cheaper and more effective options. Trade schools, community college opportunities, online learning, on the job training, and the military are commonly overlooked alternatives. College isn’t for everyone and is far from the only way to learn a profession, so don’t force yourself into a financial conundrum before you have income.

- Car loans: With proper care, a well-chosen car can last forever. My 4runner hit 20 years old this year and still rolls just fine. If your current car is running and you can’t pay with cash for a new one, question your decision to purchase a new one. All of my cars since 18 have been purchased with cash or paid off within 1 year and this move alone has saved me tens of thousands of dollars.

- Mortgage: Owning a home financed with debt could be a gift, or it could be a curse. Though a home owned with a mortgage could be an asset, it reduces location independence, increases expenses (taxes, maintenance, HOA fees), and real estate valuations caused by fluctuating markets can leave you “underwater.” The solution is to heavily assess whether renting is better than buying. Additionally, assess how buying and owning a home fits in all possible scenarios in your life – you move, you lose your job, you can’t AirBnB, etc.

As a review. We want to pay off debt as soon as possible and avoid debt because…

Debt drains your income…before the income hits your account: When you have debt, a significant portion of your income goes towards paying interest and principal on the debt, which can limit your ability to save and invest for the future. Ultimately debt decreases how much you can save, how much you can invest, and how quickly you can achieve financial independence.

Debt limits your choices and freedom…to leave, to travel, and to risk: The commitment of repaying debt monthly limits your ability to take risks and make lifestyle choices or pursue career opportunities.

If you lose your job and have no debts, you can recover. If you lose your job and have debts, you immediately start getting pulled underwater financially.

If you decide to quit everything and travel the world, you can hitchhike and find food along the way (I’ve seen it happening with happiness many times). If you have debt, you are chained to whatever pays you to repay your debts.

(Click to return to the table of contents)

Reducing Expenses

Reducing expenses is important to achieving financial independence because it allows us to save more money, invest more, and learn to live better on less.

Reducing expenses creates more savings, allowing more opportunities to invest, and shortens the timeline to financial independence

By reducing expenses while maintaining the same income we naturally increase the savings that can be invested. This additional invested savings then generates more passive income feeding the compounding loop of income, helping us achieve financial independence sooner.

Actively reducing expenses creates a low-cost life allowing you to live longer on what you have now, or less.

If you have $100,000 in the bank and your lifestyle costs $100,000, you can live for exactly 1 year off your current assets.

If you have $100,000 in the bank and learn to live off $25,000 per year (as is possible in Bali thanks to a $2,039 per month cost of living or in Buenos Aires for $1890 per month cost of living) then you can live for 4+ years on the same money, by simply changing your lifestyle.

This skill of adjusting one’s lifestyle expenses is fantastic for lowering “your number” or the assets and passive income per month required for you to maintain your current lifestyle.

Ways to reduce expenses

There are many ways to reduce expenses in order to achieve financial independence. Some common strategies include:

- Creating a budget analyzing for areas to reduce expenses as a starting point

- Minimizing housing costs

- Cutting back on transportation costs

- Reducing food expenses

- Being mindful of discretionary spending

- Being wary of lifestyle creep

- Learning self-sufficiency skills

Let’s walk through what each of these opportunities to reduce expenses look like in reality:

Create a budget and analyze for areas to reduce expenses: Creating a budget allows you to plan reasonable spending limits, then track spending against it. Through this “plan, track, measure” approach, you can easily identify areas active spending areas to cut back and increase savings. Then,you can save more money each month through awareness of our spending habits (and spending faux pas on the path to financial independence).

Planning a budget and tracking should be the starting point for any financial plan. Then, you can go item by item through your expenses.

Minimizing housing costs: Housing is often the largest expense for many people. According to Bankrate.com, the average American spends $22,624 per year or $1,885 per month on housing. Finding ways to reduce housing costs, via a different approach, such as renting vs. owning, living alone vs. with roommates, moving to a cheaper neighborhood, or moving to a smaller (and cheaper) home can have a big impact on one’s ability to save.

If housing is eating a lot of your monthly income, consider these opportunities to reduce housing costs:

- Bringing in or living with roommates

- Owning vs. renting (accounting for taxes, home ownership costs, mortgage costs and equity)

- Downsizing: Moving to a smaller sized home with fewer rooms, or moving from a house to an apartment

- Cheaper neighborhood: Neighborhoods further away, up and coming neighborhoods, or locations devoid of “zip code envy”

- Moving to a cheaper city, state, or country

- Renting out your home and moving into an apartment to potentially generate a profit and temporarily reduce expenses

- Alternative living: tiny homes, van life, etc.

Cutting back on transportation costs: Transportation is another significant expense for many people as fuel, car maintenance fees, and tolls stack up.

The average American spends $819 per month on transportation costs, making it the second largest monthly expense (Source). However, this is just the average, so half of Americans spend more than that to keep and use their cars. Accounting for purchase/car loan repayment, fuel, maintenance, insurance, parking fees, and toll fees, transportation costs add up to a hefty number.

To detail the value of that $819 spent per month, $1,005 buys you an entire month of life in beautiful Hoi An, Vietnam so that is a lot of money to spend on a single aspect of your life.

Analyzing when you drive, where, and why can be a great exercise in planning lifestyle changes. Most people drive routinely to work, to shop, and for leisure activities.

To reduce driving to work

- Look into remote work or flex work options for your current job

- Look into public transportation options, and prioritize the availability of good public transportation when moving homes or switching cities (to automatically save ~$750+ per month as an unlimited monthly pass is $100 in most major US cities)

- Consider moving to a home closer to your place of employment – if the net savings/costs make sense

To reduce driving for “chores”

- Leverage online shopping and payment

- Consider buying in bulk to make fewer trips, and setting up storage at your home to accommodate bulk buying

To reduce driving for entertainment

- Aim to live in walkable neighborhoods with things you love nearby and plenty of green spaces for free, healthy leisure activities

- Add cycling for “leisure commuting” to your lifestyle

Fun addition: Consider biking as much as possible

Reduce food expenses: Food is another area with potent opportunity for cutting expenses and saving. High quality, healthy food should be part of everyone’s diet regardless of the cost. However, most people waste money by eating out, eating of season, and choosing food with costly packaging, processing, or marketing.

On average, the price of eating out is 7 times more expensive than cooking at home, thanks to the cost of prep, service, marketing, and facilities. So, for leisure nights, cook at home for pleasure and take a packed lunch to work to save up to 85% on your food spending.

Additionally, many people purchase food at their grocery stores that is out of season, and thus more costly as it must be shipped in and handled with care. Learn to buy local, in-season foods that your region specializes in, and you’ll save tremendously.

Last, beware of food with excessive packaging, processing, and marketing, as these all generally reduce the quality of food, per dollar spent, or increase the cost of the food.

To save money on food expenses:

- Buy in bulk: Costco and bulk buying are your friends. Buying in bulk, vice in smaller, highly marketed packaging, can severely cut costs. If the ingredients label is the same, and the quality of the ingredients is the same, the food is likely the same

- Buy locally, in season: By buying the fruits, vegetables, and meats that come from nearby, you’ll eat healthier for cheaper by skipping fuel fees and logistics fees that get added to shipping costs

- Eat out less: Eating out increases the cost of each meal, and your eating expenses, by 4 to 5 times on average and up to 7 times. Learn to cook your favorite meals at home, and take homemade meals to work to cut costs

- Host dinner parties and potlucks instead of eating out: I picked up on this with Italians. You can have just as much fun eating in, and with a more intimate atmosphere, for far cheaper than eating out in a group. Skip the bar or restaurant and open your home while sharing prep of the meal and BYOB

Be mindful of other expenses and discretionary spending: Other areas where individuals can save money include discretionary spending areas such as entertainment, clothing, and travel. Being mindful of expenses involves asking if the purchase is an expense (consumable with net negative financial impact) or an asset (long-lasting or income generating), and equal in value long term to what it will cost long term.

Practice “spending awareness” and asking “do I need this?” By being mindful of these expenses and finding ways to minimize them, individuals can save more and work towards achieving financial independence.

Beware of lifestyle creep: For many people, as their income increases, so do their expenses. It could be celebratory or it could be keeping up with the Jones. In any case, be aware that any increase in expenses should be intentional and purposeful, and that any expense increase also increases your timeline to financial independence.

Learn self-sufficiency skills: Beyond the personal satisfaction of learning a new, practical skill, you’ll save money by learning to do, repair, and make things yourself. Consider cooking, mending clothes, home maintenance, automobile maintenance and repair, woodworking, gardening, and more as hobbies, and they could become money-saving satisfaction-inducing skills.

(Click to return to the table of contents)

Increasing Income

By increasing income, while keeping expenses the same, we naturally create a greater percentage of income to save and thus accumulate wealth more quickly. We can increase our active income by pursuing a higher-paying job, starting a business, or side hustle. Or, we can increase our passive income by investing in real estate or stocks, or other investments that generate passive income.

This positive feedback loop of income -> savings -> investment -> passive income -> savings–> investment is the income-fueled process that allows us to achieve our financial “number,” financial independence, and retire early more quickly.

When it comes to increasing your income, focus on diligence and generating long-term recurring income that leans more towards passive (requiring less time and active effort) than active (dollar amount tied to hours worked). However, in the short term, you should also make continuous efforts to increase your salary at work too.

Some ways to increase income recommended within the FIRE movement include:

Pursuing a higher-paying job position or career field: By developing new skills, and pursuing advanced degrees or certifications we can get higher paying jobs, in our same industries, or more adventurously change industries to a more lucrative field with higher pay and better job prospects

Starting a side hustle or side business can also provide additional income streams. This might involve starting a freelance services business, selling products online, or providing consulting services in a specific area of expertise.

Investing in real estate or stocks can also provide passive income streams. This might involve purchasing rental properties, investing in dividend-paying stocks, or building a portfolio of index funds.

Reducing taxes can also increase income, as it leaves more money available to save and invest, feeding our financial loop. This might involve taking advantage of tax-advantaged retirement accounts, itemizing deductions, or structuring income to take advantage of lower tax rates.

Practical examples of reducing taxes include using the Foreign Earned Income Tax exclusion, operating as a privately owned small business for the related tax breaks with incorporation in a tax friendly state, moving to a personal income tax free state (such as Texas or Nevada), etc.

Forget get rich quick schemes

Most of us are underemployed with opportunities to leverage our extra time and skill to generate additional income. Whether you aim to improve your education and qualifications, ask for a raise, hunt for a new job, or create a side business, there is plenty of opportunity to increase income. Put down social media, start reading, start watching tutorial videos, and start experimenting to become better in your profesion and generate new forms of income.

There is no reliable, sustainable way to get rich quickly. Through diligence, focus, and the willingness to grow, getting rich slowly is very possible

Investing

Once we have the extra money to invest, why should we invest and how should we do it?

When you’re heading towards financial independence, you need your money to work for you.

When you invest, your money works for you, with each dollar working like a little employee generating returns over time. These returns from each dollar grow your wealth and the number of dollars actively working for you and allow you to achieve financial independence more quickly than if you simply saved your money in a low-interest savings account.

Money in a savings account won’t grow at the rate we need our money to grow to achieve financial independence.

The average savings account rate of return is .2%

The average stock market return is 11.9%

Over 25 years…

$1,000 left in a bank account grows to $1,059.12

$1000 invested in the stock market grows passively to $3,108.93

That is a ~$2,049.81 gain simply by putting your money in a different account – no extra work.

The bottom line is that we can’t just work and save money to reach financial independence. We must properly invest our savings and make it work for us to achieve financial independence.

Real estate, financial investments (e.g., stocks, index funds), and starting businesses can all work as ways to invest, grow your money, and finance financial independence. We’re interested in long-term sustainable investment returns large enough to cut down the amount of time left until we’re financially independent.

In addition to earning more money more quickly by investing our money, sound investing offers some other great benefits.

Investing properly provides diversification and lowers risks of losing your money: Investing in a variety of assets, such as stocks, bonds, and real estate, can provide diversification reducing volatility across your portfolio, and helping you manage risk. By spreading your money across different types of investments, you can minimize the impact of any one investment going down in value on your portfolio, in the event that the real estate market, stock market, or even a specific business investment experiences a bad period and losses. The gains in the other assets in a diversified portfolio will make up for losses in a single category.

Investing helps you keep up with inflation: Over time, the value of money decreases due to inflation, and a single dollar naturally buys less food, less house, etc. By investing your money, you earn returns that keep pace with or even exceed the rate of inflation over time. This ”inflation pacing” allows you to maintain the value of your money, “purchasing power,” and how much you are able to purchase with a single invested dollar over time.

When it comes to investing within the FIRE movement, there are several effective investment opportunities suggested that are manageable risk, simple to use, and have led to many average people achieving financial independence.

The financial approaches to investing commonly suggested within the FIRE movement include:

Investing in low-cost index funds that cover a broad portion of the stock market: Index funds are a type of low-cost mutual fund that is exchange-traded and automatically tracks a specific stock market index, such as the S&P 500, or broader, such as an emerging market fund. These funds, also called ETFs or “Exchange Traded Funds” are often low-cost (in terms of expenses) and provide broad exposure to the stock market, making them a good option for investors who want to achieve long-term growth without taking on excessive risk. The “broad exposure” hedges risk and reduces the possibility of the assets’ value going down in the long term, but you also benefit from the profits, just like the companies that you own via the ETF do.

If you’re interested in more information on why and how to invest effectively, check out the next article on How to Become Financially Independent: A Complete Guide and Summary of the 15 Best Books on Investment and Financial Independence

Additionally, these funds often outperform more expensive “managed funds” performing as well as the entire stock market does.

As a starting point for investing, I highly recommend researching Vanguards VTSAX (for the stock market) and VBTIX (for the bond market) funds in a split between 70%/30% Stocks to bonds for conservative investors to 90%/10% for young/aggressive investors.

VTSAX is a very low-cost ETF (Exchange Traded Fund based on the CRSP Total Market index fund) from Vanguard that tries to track the entire stock market.

VBTIX is a very low cost ETF (Exchange Traded Fund that tracks the entire Investment Grade US Bond Market via the Bloomberg U.S. Aggregate Float Adjusted Index) from Vanguard that tries to track the entire US bond market and adds a measure of safety to your portfolio.

The ratio split between these two ETFs that your investment portfolio should take depends on your risk profile, risk tolerance, and how close you are to your retirement date.

For those with a large sum in savings to invest, look into dollar cost averaging

If you have a large sum of cash sitting under your bed and need to invest it soon, look into the concept of dollar cost averaging** over 3 months to 12 months, to buy into your new portfolio.

Dollar cost averaging is the process of dividing a lump sum to be invested (say, $20,000) and investing it in equal chunks over a period. For example, $2,000 once a month for 10 months could be an option. By doing this, we avoid buying too much of a stock or ETFs when the price has spiked too high or has dipped too low. Generally, throughout the dollar cost averaged investing period the “average cost” of the stock will reach a reasonable point close to the average price of the stock or ETF you buy into. Not too high, not too low, just a good starting point.

Personally, I waited far too late to optimize my portfolio and instead used managed funds for a decade to my own detriment. Later, I realized I’d lost $200,000+ worth of potential gains that would have come from simply investing in index funds. Now, I only invest in/trade index funds and businesses, and I highly recommend researching whether the same approach is right for you.

Investing in real estate

Real estate can be a good investment for those in the FIRE movement, as it provides the potential for both rental income and long-term appreciation, and a home owned outright can be a fallback safeguard to live in and reduce expenses. However, investing in real estate requires careful research and due diligence in order to make sure you are investing in properties that will generate positive cash flow and suit your long term plan.

My experience with real estate: Buying a house in Bali to cut costs and improve my life:

In my current portfolio, I own a home in Bali. For the home, I cut “purchase costs” by half by managing the build myself (and gaining twice as much grey hair). That real estate investment serves foremost as my home and a base between travels, cutting my housing costs to zero, excluding maintenance and utilities. Secondarily, allowing that home to be rented (by proper legal channels according to Indonesian law) can generate $2,000 to $3,000 of passive income when rented during my travels.

Purchasing a home in Bali, is a perfect example of making sure real estate investment fits your plan. As a travel writer, Bali is my base between travels, making it easy to return and personally handle issues that may arise with renters. That same scenario, flying to Bali just to appease renters, would be virtually impossible if anyone in the US owned my home. Additionally, due to Indonesian law, rental taxes, and the harsh Bali climate, 30% to 40% of my rental income will go to taxes, management of my house as a rental by a local (required by law), and repairs due to intense equatorial sun, drenching rainy seasons, and building a home on precarious ricefields.

Losing 30% to 40% off the top would be harsh if I hadn’t selected an area where the average rental price is absurdly high. Last, I was able to design the build myself, to be (fairly) low cost, low maintenance, and very comfortable (by my utilitarian standards), decreasing my expenses and increasing savings, my bottom line, and my home’s outlook as an investment property and pleasurable base instead of a headache and expense.

Though I do advocate investing in real estate, I very much encourage researching:

- Logistics of ownership for the particular home and location

- Expected benefits and financial returns

- The total cost of ownership (taxes, maintenance, HOA fees)

- The nuts & bolts of how you can rent out the real estate

- Expected rental prices compared against the home’s cost averaged over time

- Comparable sales prices

- Whether owning and managing that real estate fits into your long-term goals of travel and living in a different location.

Utilizing tax-advantaged accounts: Retirement accounts, such as 401(k)s and IRAs, and Health Savings Accounts provide tax benefits that can help you grow your wealth more quickly. By taking advantage of these accounts, you can reduce your tax bill and maximize your savings over time.

Overall, the key to investing within the FIRE movement is to take a long-term view and focus on strategies that provide consistent returns over time with minimized expenses and maintenance. By investing in a diversified portfolio of assets and being patient, you can grow your wealth and achieve financial independence with minimal headaches

“Your number” for retiring, and the investments you’ll need to cover it

The amount of liquid assets you need to return a monthly passive income amount that is enough to achieve financial independence is referred to within the FIRE movement as “your number.” This number varies widely from person to person depending on the individual’s expenses. This number is often calculated using the “4% rule,” which states that if you withdraw 4% of your investment portfolio per year in retirement, you should be able to sustain that level of spending for 30 years without depleting your savings and indefinitely in most cases, while increasing withdrawal every year on pace with inflation.

To achieve financial independence, most followers of the FIRE movement typically aim to accumulate enough savings and investments to cover their expenses by this rule.

For example, if your annual expenses are $40,000, you would need to have a portfolio of $1 million of investments to achieve financial independence by the 4% rule. This is based on the assumption that your investment portfolio will earn a long-term average annual return of at least 7%, and that you will keep your expenses relatively stable over time.

(Click to return to the table of contents)

The Tenets of FTE (Tenets of Financing the Escape)

Whereas FIRE, and the tenets of avoiding debt, reducing expenses, saving, and investing, are suitable for anyone that desires good financial health, “The Escape” is uniquely suited to adventurous souls, willing to change their location to improve their quality of life quickly, while instantly reducing expenses, increasing savings, and increasing extra cash available to invest. Additionally, you don’t have to be fully financially independent to “escape” and improve your quality of life.

The Tools for “The Escape” are:

- Cultivating Location Independence enabled by the resources and skills to live around the globe

- Geoarbitrage, which is using location independence to move to in and live in locations with lower expenses and higher quality of life

If you’re averse to new environments and prefer to stay put – save your time and skip over this section.

However, if you are open to moving somewhere else to achieve the same quality of life – food, accommodation, and amenities – for a cheaper price, or simply to add something new and spicy to your life, read on.

“The Escape” part of Financing the Escape is a positive feedback loop of cultivating “location independence” or the means and logistics to work from anywhere, using that location independence for “geoarbitrage,” or moving to locations where you can live better for cheaper, and save more money that can be invested to reach financial independence more quickly.

Let’s get into the details of the tenets of FIRE and FTE.

(Click to return to the table of contents)

Cultivating Location Independence

What is location independence and what does it entail?

Location independence is the ability to live or work from anywhere around the globe – facilitated not only by your financial assets, but your skills, your planning, your mindset, and the logistical situation you create. Though this kind of mobility is easily achieved when fully financially independent, it is still possible to cultivate and use location independence while working by using the opportunity for remote work (with a company) and freelance work that is performed completely online.

By cultivating the skills and resources needed to be location independent, and move anywhere as we see fit, we allow ourselves to improve our quality of life and save money via geoarbitrage.

How can you cultivate and achieve location independence?

Develop a portable skill set: Developing skills that can be used to work remotely helps immensely in achieving location independence. This might include skills like web development, digital marketing, copywriting, or virtual assistance. These skills can be used to work for a variety of companies, to work as a freelancer or consultant, or to start your own business.

I recommend reviewing this list of jobs of successful digital nomads reported during the Global Digital Nomad Study

Start an online business: After developing portable skills and understanding the location independent market you’ll work in, starting your own business can be a great way to move toward achieving location independence. By creating a business that can be operated online or remotely, you can work from anywhere in the world and be your own boss. Some businesses that lend themselves well to location independence include e-commerce stores, digital marketing agencies, freelance writing or design, and online tutoring.

For ideas of potential online business, I recommend perusing the listings on Flippa and Empire Flippers, two of the world’s largest online business brokers.

Work for a company with a remote work policy: Many companies now have remote work policies, allowing their employees to work from anywhere in the world. If you have a skill set that can be used remotely, it may be possible to find a job with a company that offers this flexibility.

Keep in mind that though there are many remote job only job forums, such as:

- Remoteok.com

- WeWorkRemotely.com

- Workew.com

- Remotehunt.com

Most remote work opportunities will come from developing a stellar skillset in a domain that is commonly accepted as remote (i.e., software dev., tactical marketing management, SEO) and either learning about a position via word of mouth or networking into a long-term freelance position.

Build passive income streams and “low effort income streams”

Creating a source of passive income, such as rental properties, automated online businesses, or dividend-paying stocks, can provide the financial freedom necessary to achieve and maintain financial independence as well as location independence. With a steady stream of passive income, you can work from anywhere in the world without worrying about the day-to-day management of your investments.

Embrace digital nomadism

Digital nomadism is a lifestyle that involves traveling and working remotely. By embracing this lifestyle, you will achieve the mindset and skills required for full location independence while also exploring different parts of the world and experiencing new cultures.

Logistics to think about when developing location independence

Being location independent isn’t just about accruing resources and assets to “finance the escape” and portable skillsets and business options. If you plan to be abroad for 6+ months per year, like the average digital nomad, take these factors into consideration, and learn how to plan for them now.

- Visas: Aim for countries with a visa, and allowable stay, of 3+ months. These countries are my favorite, that offer expat friendly visas.

- Taxes: Even abroad, and while earning money abroad, you will likely have to pay taxes to your home country. Keep in mind that for most other countries, if you spend more than 180 days in them per year, you become a tax resident. Plan accordingly.

- Banking: Not all bank accounts and credit cards are conducive to international travel as some have exorbitant foreign transaction fees, maintenance fees, and atm fees. Check your account and card terms and ensure you have a checking account with no atm fees, a travel friendly credit card, and a means to transfer money to foreign accounts quickly and easily such as wise. Additionally, setup as many backup, foreign friendly accounts, like Wise and Paypal, to use as emergencies arise.

- Wi-fi, SIM cards, and connectivity: Ensure you have at least one sim card from home that you can receive text messages on for bank and financial authentication from home while anywhere in the world. For this, I highly recommend Fi from Google.

- Your things at home: Reduce the number of physical things you own at home as much as possible. Empty apartments and homes cost money, as do large storage units to hold the possessions you can’t bring while traveling. Embracing minimalism and reducing as much stuff at home as possible, and thus reducing expenses, adds up to a lower-cost, location-independent lifestyle.

- Brainstorming Locations for Your Escape: There are millions of places – countries, cities, neighborhoods – in the world that you could live that offer exactly what you love for a more reasonable price than those passions would cost you back home. Do some brainstorming and research to understand what you want and need in life, then start hunting for locations that offer that at a price that fits “your number.” That is a recipe for financial independence and happiness. This list of nomad-friendly cities is an excellent list for figuring out some great potential homes for you.

Overall, achieving location independence requires a combination of skills, resources, and a willingness to take risks and embrace new opportunities. By developing a portable skill set, creating passive income, and exploring different career paths and business opportunities, you can achieve the freedom to work and live from anywhere in the world.

Geoarbitrage: Leverage location independence and geoarbitrage to live the same quality of life for cheaper

Geoargitrage is my favorite tool in the financial independence toolbox of things we can do to achieve a better quality of life. With a bit of location independence you can leverage geoarbitrage immediately to drastically improve your life. The food you eat, the default “vibe” of people around you, the nature where you live that is available to explore and enjoy, and the comfort you live in can be changed immediately with no additional expenditure of resources or expenses, just by changing where you live.

In that same move, you can decrease your expenses, increase how much you save, and increase how much you have available to invest thus putting you on a faster track to financial independence.

For example, when I lived in Dallas, Texas, I had an apartment downtown (~$1500 per month) walking distance from coffee shops where I would work (~$5 a coffee, $15 a meal). Ultimately each month I would spend, on the frugal side, $3000 to $4000 per month of after tax money on an apartment, food, transportation, insurance, entertainment, and all other living expenses if I wasn’t careful.

Now, my home is Bali. My 2 bedroom, 2000 square foot villa cost on average per month is $500 (and much nicer than my Dallas apartment) while still being next to chic coffee shops to work from ($1.75 a coffee, $7 a meal). Ultimately, in Bali, I end up spending $1200 to $1700 per month to live comfortably and be a 10 minute bicycle ride from the beach.

The difference between these locations is a $1300 to $2800 savings per month that I reinvest in stocks and real estate, or use to bolster my travel budget for the rest of the year.

One key caveat I must add to this idea, is geoarbitrage is only a true tool if you have income that you will continue to receive while abroad. Having income that isn’t affected by where you are makes you more location independent. If moving to a new location eliminates your source of income, then it’s simply a vacation, an expense, and potentially sets you back in the path to financial independence.

How much do you need to retire? 25x your annual spending – introducing the “4% rule”

Questions: How much do you need to save to retire?

Answer: 25 times your annual spending.

Here’s why…

Understanding how much you’ll need in retirement: The 4% rule, 25x rule, and the Trinity Study

The Trinity Study, also known as the Trinity Retirement Study, was a landmark study published in 1998 by three professors at Trinity University in San Antonio, Texas. The study analyzed historical market data from 1926 to 1995 to determine how much money retirees could safely withdraw from their investment portfolios each year without depleting their savings.

The study concluded that retirees who withdrew 4% of their initial portfolio balance at the beginning of retirement, and adjusted that withdrawal amount for inflation each year, had a high probability of their savings lasting for 30 years or more. The researchers found that, based on historical data, a retirement portfolio invested in a mix of stocks and bonds had a success rate of approximately 95% when using this withdrawal rate.

The 4% rule has since become a widely used rule of thumb for retirement planning, as it provides a simple way to estimate how much money someone may need to save for retirement. The rule suggests that if someone has saved 25 times their annual living expenses, they should be able to safely withdraw 4% of their portfolio each year in retirement and have a good chance of not running out of money over a 30-year period.

For example, you have $1,000,000 in retirement accounts investment across the whole stock market. According to the 4% rule, you can spend $40,000 yearly for ~30 years, increasing that $40,000 annually with inflation, without running out of money.

$1,000,000 * 4% =$40,000 annual withdrawal rate, indefinitely.

It’s important to note that the 4% rule is based on historical market data and is not a guarantee of future performance. Additionally, the 4% rule assumes a relatively fixed level of annual expenses, not increasing medical expenses, large purchases, or moving a higher cost locale, and a portfolio invested in a mix of stocks and bonds. Individuals should tailor their retirement plan to their unique situation and consider their individual risk tolerance, lifestyle goals, and financial needs.

What about inflation?

The 4% rule from the Trinity Retirement Study accounts for inflation by allowing the withdrawing person to ajust the withdrawal rate annually to keep pace with rising prices. The study did this by assuming that retirees will increase their annual withdrawal amount each year by the rate of inflation, which is typically measured using the Consumer Price Index (CPI).

For example, if a retiree begins with an initial withdrawal rate of 4% of their investment portfolio, and the inflation rate in the first year is 2%, the retiree would increase their withdrawal rate in the second year to 4.08% (4% + 2%). In subsequent years, they would continue to adjust their withdrawal rate to keep pace with inflation.

The inflation adjustment is important because it helps to ensure that retirees can maintain their purchasing power and keep up with the rising cost of living. By accounting for inflation, the 4% rule provides a more accurate estimate of the amount of money needed to sustain retirement income over the long term.

Notes to keep in mind:

- The Trinity study assumes only a 30 year retirement period. Longer retirements likely need a lower withdrawal rate or a dynamically adjusted withdrawal rate (increased or decreased), based on stock market performance (bull market or bear market).

- The Trinity Study assumes a mixture of stocks and bonds, and doesn’t account for the volatility of crypto, or assets such as real estate and owned businesses.

- The Trinity Study assumes $1 in the bank account is “success,” thus some 30 year periods had lower ending balances. Again, if you are accounting for a period of withdrawal longer than 30 years, you will want to dynamically adjust your withdrawal rate as you monitor the balance of your assets.

Recommended Reading for Financial Independence

Investing

- The Bogleheads Guide to Investing

- A Random Walk Down Wallstreet

- If You Can: How Millenials Can Get Rich Slowly

- The Four Pillars of Investing

- The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns

- The Intelligent Investor

- The Simple Path to Wealth

Early Retirement

- Get a Life: You Don’t Need a Million to Retire Well

- Early Retirement Extreme

- Building Wealth And Being Happy: A Practical Guide To Financial Independence

FIRE Lifestyle FAQ:

How does the FIRE movement work?

The Financial Independence and Retire Early Movement (FIRE Movement) is a community of people that want to retire early and thus are dedicated to saving as much money as possible to reach a savings amount ( referred to as their FIRE number ) that when invested properly will support them with passive income for the rest of their lives.

This money is commonly invested in ETFs in brokerage accounts or retirements funds or in real estate. When invested properly, an amount 25x the annual spending of individual will allow them to with draw money in that specific amount indefinitely.

What is Lean Fire ?

- Lean FIRE is a sub-philosophy of FIRE wherein many fire proponents apply minimalist, frugal, and stoic philosophies aiming to achieve FIRE by reducing their expenses to $25,000 per year per person or $50,000 per year per couple. This thus reduces their required retirements savings, allowing them to gain financial independence more quickly through frugality.

What is Fat FIRE

a version of financial independence and early retirement that involves accumulating a larger amount of wealth and spending more in retirement than the traditional FIRE approach.

While traditional FIRE focuses on achieving financial independence and retiring early by living frugally and saving a high percentage of income, Fat FIRE takes a different approach. Fat FIRE practitioners aim to accumulate a larger amount of wealth and live a more comfortable lifestyle in retirement, with a higher level of spending on travel, hobbies, and other luxuries.

Fat FIRE practitioners typically have higher income levels and invest more aggressively than those pursuing traditional FIRE. They also tend to have higher expenses and require a larger portfolio to support their retirement spending.

The term “Fat FIRE” is meant to distinguish this approach from the more frugal and minimalist lifestyle associated with traditional FIRE. It’s important to note that both approaches to FIRE are valid and can be tailored to meet an individual’s goals and preferences.

Is the FIRE movement realistic?

Yes, the FIRE movement is realists, proven by the droves of FIRE movement followers that have retired early. Even if the principles of the movement don’t lead you to retire at 30, following their principles of saving and investing will improve your retirement plans and situation.

All that is needed is a willingness to cultivate your financial literacy, and a few dollars to invest. The risk of such activities is low, and the outcomes could be lifechanging.

What are the 4 rules of FIRE?

Save income, avoid debt, reduce expenses, and invest savings

Next Steps: A Tactical Checklist To Financial Independence

Preliminary Steps: Assessing your spending, assets and needs

- Assess yourself, your desires, and your needs to understand what you need (financially and intangibly to be fulfilled and content)

- Assess and understand your spending and monthly expenses

- Assess and understand your current income

- Calculate, understand, and specify your income requirements (“Find “your number”)

- Define and understand your financial goals, and the sacrifices required

Eliminate and avoid debt that is a net expense

- Eliminate existing debt

- Avoid debt

- Student loans

- Credit card debt

- Short term loans

Reduce Expenses

- Reduce Housing Expenses

- Consider renting over the full costs of ownership

- Consider roommates

- Size down

- Move to a cheaper neighborhood, city, country, or state

- Consider tiny home ownerships

- Reduce Eating & Food Expenses

- Eat out less

- Cook at home more

- Take a lunch to work

- Make coffee at home

- Avoid drinking alcohol in bars or in restaurants

- Buy food in bulk

- Reduce transportation costs

- Shorten commute to work (saves gas, vehicle maintenance, and time)

- Take public transportation

- Walk or bike when possible instead of driving

- Opt for a smaller car on initial purchase

- Opt for a more reliable car on initial purchase (based on consumer reports)

- Don’t purchase cars new, only used

- Keep your car longer: avoiding buying a new car early, properly maintain for a longer useful life

- Take alternate, lower cost vacations:

- Exchange a costly Las Vegas or resort weekend for a road trip and camping

- Avoid lifestyle creep

- Avoid buying a new car if not necessary

- Avoid upgrading phones or laptops if not necessary

- Avoid replacing large appliances (refrigerator, TV) unless necessary

- Repair what you have before buying new

- Purchase all new items with a “buy it for life” mindset:

- Reduce leisure and entertainment expenses

- Swap costly entertainment for fun activities outdoors

- Host dinners, barbeques, and potlucks instead of having events at bars and restaurants

- Beware of the lasting expenses of decisions with long term effects

- Loans

- Mortgages

- Purchasing cars with debt financing

- Large credit card purchases

- Marriages

- Having children

- Reduce everyday expenses by learning self-sufficiency skills that improve quality of life and save money

- Consider cooking

- Mending clothes (to extend life)

- Home, automobile, bike repair

- Gardening, etc.

Bolster income

- Start by strategically choosing a profession or occupation with plenty of jobs available (job surplus), high salaries, and flexibility relative to training timeline, requirements, and costs

- Strategically Increase Income

- Demand your worth when signing into a new job

- Request promotions

- Request raises

- Leave your current company for a higher paying position

- Work smarter, if paid by the project

- Work more hours, if paid by the hour

- Build side hustles

- Build side businesses

Invest in semi-passive and low effort investments

- ETFs (Index funds tracking the stock and bond markets)

- Real Estate

- Small businesses that do not require active management

- Online businesses that do not require active management

Invest Holistically (beyond financial investments)

- Health and fitness

- Eat Healthy and exercise as preventative maintenance

- Use outdoor and sports activities as a low cost leisure activity

- Invest in healthcare and preventative care

- Invest in mental health education and treatment

- Knowledge, education, and marketable Skills

- Invest in personal finance education

Cultivate Location Independence

- Get a passport

- Visit foreign countries to test what works for you

- Test if the location independent lifestyle suits you

- Research foreign countries, cities, and neighborhoods that could make better homes for you

- Research visa opportunities that suit your passport/country of citizenship

- Develop “portable skills”

- Cultivate location independent businesses or income streams

Engage in geoarbitrage

- Test the foreign cities and countries on your list

- Explore the digital nomad lifestyles

- Explore the expatriate lifestyle

- Settle in to a few international cities, build a long term social network, and establish yourself in these cities accordingly

.

.

ABOUT THE AUTHOR

Carlos Grider launched A Brother Abroad in 2017 after a “one-year abroad” experiment turned into a long-term life strategy. After 65+ countries and a decade abroad, he now writes about FIRE, personal finance, geo-arbitrage, and the real-world logistics of living abroad—visas, costs, and tradeoffs—so readers can make smarter global moves with fewer surprises. Carlos is a former Big 4 management consultant and DoD cultural advisor with an MBA (UT Austin) and Boston University’s Certificate in Financial Planning. He’s the author of Digital Nomad Nation: Rise of the Borderless Generation and is currently writing The Sovereign Expat.