Everyone would love the idea of being “financially independent,” and the FIRE approach is a great option that makes that life accessible. Unfortunately, the prospect of sacrificing life’s comforts to achieve and live in Lean FIRE, or even FIRE, is too much for some to fathom. At the other end of the spectrum, the millions of dollars required for Fat FIRE put the system out of reach for most people. But nestled in between is the goldilocks version of FIRE called “Chubby FIRE” – vastly more comfortable than Lean FIRE, and, with the right planning, vastly more achievable than Fat FIRE.

While Chubby FIRE’s clear differentiator from Fat FIRE is the smaller FIRE number (maintaining a tad of overlap), the subtle difference that should matter to aspiring FIRE followers is the range of income and assets required, which makes Chubby FIRE vastly more attainable than Fat FIRE. While achieving Fat FIRE generally requires a very high income, either from an executive position, or a difficult-to-attain certified position (e.g., doctor, lawyer), or business ownership, Chubby FIRE is in a zone that the average American, if they plan well and start early, can achieve.

In this guide, we’ll break down what Chubby FIRE is, how to achieve it, and the essential steps and process that the average American can follow (if starting early) to achieve Chubby FIRE.

Chubby FIRE at a Glance

The idea:

Chubby FIRE is financial independence with a comfortable lifestyle and real margin—between Lean FIRE’s tight budget and Fat FIRE’s high-discretionary spending.

The equation:

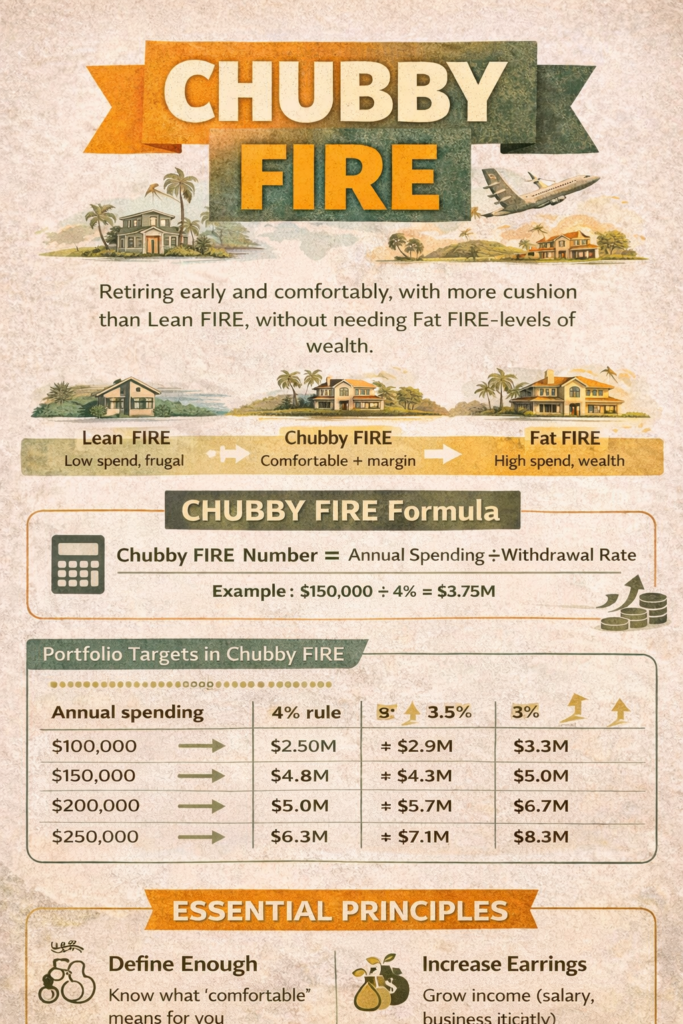

Chubby FIRE Number = Annual Spending ÷ Withdrawal Rate

(4% = ÷ 0.04; 3.5% = ÷ 0.035; 3% = ÷ 0.03)

An example:

If you spend $150,000/year and plan around a 4% rule, your target is $3.75M.

At 3.5%, it’s ~$4.29M—same lifestyle, more margin.

The Approach for you: Use our Chubby FIRE Calculator:

Run your number here: (link to Chubby FIRE calculator)

Key Points

- Chubby FIRE is early retirement with comfort + margin, not extreme frugality and not luxury-for-luxury’s-sake.

- It’s “high” inside the FIRE world, but still a structured plan, making it realistic and not a fantasy.

- You still typically need a strong earning engine, such as a high salary growth, business ownership, or meaningful investing consistency, but the need isn’t as extreme as with Fat FIRE.

- The biggest unlock is simple: start very early, spend intentionally, earn intentionally, invest boringly, protect the downside, and actively seek other income opportunities.

- The biggest risk is also simple: lifestyle creep dressed up as “I deserve it.”

Table of Contents

Chubby FIRE is a style of financial independence where you aim for a comfortable, upper-middle-class lifestyle in early retirement with enough cushion to travel, eat well, live in a place you actually like, and handle life without panic, but without building a Fat FIRE empire.

It’s still FIRE. The math still works the same way. The difference is that your “enough” number is bigger because your lifestyle is bigger – and that means the path usually demands one (or more) of these:

- higher income (salary, business, equity, or a strong career runway)

- A higher savings rate (often meaningfully above “normal”)

- longer runway (more years of earning)

- smarter tax planning

- or a location strategy that keeps comfort high while costs stay reasonable

Chubby FIRE is the “comfortable early retirement” lane — and it’s only sustainable if your spending stays intentional. You’re not trying to win consumption. You’re trying to buy freedom without hating the journey.

Retirement incomes in the Chubby FIRE range tend to fall between $100,000 and $200,000, which translates to a FIRE number of $2.5 million to $5 million when using the “4% rule” for safe withdrawals. While these numbers are much higher than the average FIRE follower’s target numbers, they are still more achievable than Fat FIRE numbers (reaching $10+ million) for the average individual – as long as they start early, exercise discipline, and actively seek out opportunities to “expand” income.

How much do you need for Chubby FIRE? | Chubby FIRE Net Worth ($2.5m to $5m net worth)

People throw around “Chubby FIRE net worth” ranges because it’s a quick shortcut. The most common band you’ll hear is roughly $2.5M to $5M. That range makes sense as a starting point because it maps to a spending level that feels “comfortable” in many parts of the U.S. (and downright great in others), and puts the effort required to achieve Chubby FIRE into clear perspective as a “total invested assets” number.

But here’s the truth: there is no universal Chubby FIRE number.

There is only your spending level and the withdrawal rate you’re willing to plan around.

Chubby FIRE is not “a net worth.” It’s a spending-powered plan.

So instead of asking, “Is $3M Chubby?” ask:

- What do I want my life to feel like?

- What does that cost per year, honestly?

- What withdrawal rate gives me margin and sleep?

- What’s my tax + healthcare reality in that plan?

From here, you can calculate your expenses and translate this into your FIRE number (required invested assets for financial independence).

Then you’ll know whether you’re running Lean, Chubby, or Fat – regardless of what the internet calls it. What matters from here isn’t the label necessarily, but the savings/expense bands, and the FIRE labels that go with them, which generally correlate with the best approach to achieve them.

Lean FIRE is achieved with a very intentional and minimalist life structure empowered by discipline. Traditional FIRE is about optimizing your work and savings situation, and executing the basics of personal finance and FIRE in the long haul. Fat FIRE is about working towards a “high earner” position, and then resisting cultural norms to save and invest in a way high earners don’t. And Chubby FIRE is about achieving just enough “Fat FIRE styled comfort” from the position of a more average earner lifestyle as a starting point, empowered by starting early, planning with intention, executing with discipline, and sniffing out opportunities to expand and grow earnings along the way.

We’ll dig into the different types of FIRE later, but just internalize that net worths and labels don’t matter – understanding your number and choosing the right tactics, approaches, and principles to reach it do matter.

Spending & respective portfolio targets in Chubby FIRE

The basic equation is:

Portfolio target = Annual spending ÷ Withdrawal rate

(So at 4%, it’s spending × 25)

Here’s the clean starting table (before taxes/healthcare/location assumptions):

FIRE Numbers Based on Spending and Withdrawal Rates

|

Annual spending |

4% rule |

3.5% |

3% |

|---|---|---|---|

|

$100,000 |

$2.50M |

$2.86M |

$3.33M |

|

$125,000 |

$3.13M |

$3.57M |

$4.17M |

|

$150,000 |

$3.75M |

$4.29M |

$5.00M |

|

$175,000 |

$4.38M |

$5.00M |

$5.83M |

|

$200,000 |

$5.00M |

$5.71M |

$6.67M |

Use this as a starting point. Taxes, healthcare, and housing costs can shift your real-world spending target, and many Chubby/Fat FIRE plans use a more conservative withdrawal rate to buy extra margin.

What is a Chubby FIRE lifestyle like, compared to the other types of FIRE?

A helpful way to think about Chubby FIRE is: you’re retiring into a life that still has options.

Not “unlimited options” – that’s Fat FIRE.

But real options:

- You can travel without needing to “make up for it later.”

- You can live in a good neighborhood (or at least in a place you don’t resent).

- You can say yes to hobbies that cost money.

- You can handle surprises without immediately threatening the plan.

Chubby FIRE tends to feel like:

- comfort without constant spreadsheet anxiety

- convenience within limits (some outsourcing, not everything outsourced)

- quality upgrades that actually matter to you (not status upgrades)

- a lifestyle that’s still recognizably normal — just not chained to a job

It also tends to come with one hidden requirement:

You must know you’re “enough.”

Because the line between Chubby and Fat can disappear fast when lifestyle creep becomes your hobby.

Who is Chubby FIRE for, & Is Chubby FIRE right for you?

Chubby FIRE fits people who want FIRE, but don’t want to win it by living in permanent deprivation, and to achieve that, they’re willing to be disciplined and ambitious, but not to the point of getting a new law degree or becoming a Fortune 500 executive.

It tends to work best for:

- Earners between average and high earners who can push income up meaningfully over a decade

- Entrepreneurs and investors who can create a stronger savings engine than a normal salary path

- Average earners who can find time and space to build and grow a side hustle, an income engine

- People who want to retire earlier but still live a comfortable, upper-middle-class life

- People who want to FIRE in larger cities or major metro areas (where Lean FIRE is often friction-heavy)

- People who want maximum global mobility without lifestyle compromise (travel, multiple bases, higher-quality housing)

Chubby FIRE tends to be a poor fit if:

- You hate your work and don’t have a realistic income-growth path

- Your “comfortable” lifestyle is actually a moving target

- You are not willing to proactively build a side hustle income engine if income opportunities are topped out in your current job.

- You’re relying on vague investing optimism rather than a plan you can stress-test and adapt.

Is Chubby FIRE right for you?

A quick self-check:

- Are you willing to sacrifice now for the benefit later, without resenting your life?

- Do you actually want to stop working early, or do you just want more control?

- Is your relationship with consumption intentional, or reactive?

- Are you comfortable building the engine (earn/save/invest) as a project, not a wish?

If you want comfort and early freedom, Chubby FIRE can be the cleanest lane — as long as you don’t confuse “comfort” with “no limits.”

Pros & Cons of Chubby FIRE

Pros

- More margin than Lean FIRE. More room for error, more room for joy.

- More lifestyle flexibility. Travel, hobbies, housing choices, and healthcare planning become less fragile.

- Less psychological strain. You’re not constantly fighting the “one surprise breaks everything” feeling.

Cons

- Requires a stronger engine. Higher income, higher savings, longer runway, or smarter strategy.

- Lifestyle creep risk. Chubby FIRE fails when “comfortable” becomes “automatic upgrades forever.”

- More complexity. Taxes, healthcare, asset allocation, and withdrawal strategy matter more when the number is big and the lifestyle is comfortable.

Chubby FIRE is freedom with cushions — but those cushions aren’t free.

The Math Behind Chubby FIRE & How to Calculate Your Chubby FIRE Number

Chubby FIRE math is not special math. It’s standard FIRE math with a higher spending target and (often) a more conservative withdrawal rate.

The moving pieces that matter:

- Annual spending (the real driver)

- Withdrawal rate assumption (4% / 3.5% / 3%)

- Taxes (especially if you’ll have taxable brokerage withdrawals, dividends, Roth conversions, etc.)

- Healthcare (one of the biggest “blows up the plan” variables)

- Housing (own vs rent, city vs region, lifestyle expectations)

Once you calculate your FIRE number, you’ll be able to check if you are in the “Chubby FIRE range” of $2.5 million to $5 million. Then, you can assess your income and savings rate for accurate detail, but generally, you will be able to assume that a solid FIRE plan and discipline will be necessary, along with scaling your income or building a side income engine.

How to calculate your Chubby FIRE number

- Decide your target annual spending – your target retirement lifestyle costs.

- Pick a withdrawal rate assumption for retirement that matches your risk tolerance (e.g. 4%, 3.5%, 3%, etc.)

- Compute your FIRE Number (Spending ÷ Withdrawal Rate) and assess if you’re in Chubby FIRE territory

- Add reality buffers:

- Healthcare + out-of-pocket

- Travel variability

- Home repairs/replacement cycles

- Taxes (don’t hand-wave this)

- Stress-test:

- “What if markets underperform for a decade?”

- “What if healthcare costs spike?”

- “What if I want to live in a higher-cost city again?”

- Run your plan at the lower withdrawal rates of 3.5% and 3% to see if it will work in more conservative scenarios.

Chubby FIRE isn’t hard because the math is complex. It’s hard because the inputs have to be honest.

Chubby FIRE calculator

Use our Chubby FIRE calculator to quickly see your rough numbers and think through scenarios.

- Run your spending level against 4% / 3.5% / 3%

- See how small changes in spending move the portfolio target

- Model “buffer” spending (healthcare, travel, housing upgrades)

- Decide whether you’re truly Chubby, or quietly Fat, or actually closer to Traditional FIRE

Use the calculator here.

How to make Chubby FIRE a reality: A Roadmap

- Define your Chubby lifestyle by deciding what you keep, what you upgrade, and what you refuse to fund.

- Calculate your target number using multiple withdrawal-rate assumptions.

- Build the engine: Plan your existing income, creatively increase income, control spending, automate investing, repeat.

- Plan for surprises and downside: Taxes, healthcare, buffer, and bear-market resilience.

- Run a trial version of your “Chubby” lifestyle now, not later, and see what’s real.

- Re-check your plan annually: Spending drift, market returns, life changes, and whether “enough” moved.

If you do nothing else, define “enough” early. It’s the difference between Chubby FIRE and an endless chase.

Practical Options & Income Ideas

Chubby FIRE usually needs one of two realities:

- You earn more than average, or

- You build an engine that behaves like you do (business, equity, real estate, high upside skill)

Practical levers, in descending order of impact:

1) Options for increasing income without drastically changing lifestyle or profession

- Promotion or increase in specialization

- Add high-leverage skills (sales, engineering, product, finance, executive ops)

- Negotiating equity compensation and ownership paths

- Moving to higher-paying markets temporarily (if it accelerates savings)

All of these options involve personal development and cultivating yourself to be more valuable professionally, so that you are compensated more for the same work. A recurring theme is learning, or growing into doing, what fewer people in your field and workplace are trained to do, qualified to do, and have proven they can be trusted to do. For practical ideas, look around your workplace and ask yourself what roles and tasks are people taking on, and whether they are being compensated more for it. If the answer is yes, assess this as a viable path to increasing your income to support a chubby FIRE path without increasing the number of hours you’re trading for money.

2) Building a side business engine

Lifestyle businesses can work – but only if you treat them like a business, not a dream journal. A “good” business for Chubby FIRE has:

- Recurring revenue

- Survivable customer acquisition

- Clear margins

- Doesn’t require your soul as ongoing collateral

- Ideally either runs without your involvement or only requires the amount of time you can healthily afford to dedicate outside of your 9 to 5

Side business income engines are as varied as the colors of the rainbow. Though the “best” options – those with reliable income and simple, durable business models – are boring, this is by design. Side businesses such as vending machines, “easy” yet well-compensated niche services such as professional window washing or landscaping, ice and water machines, self-operated parcel lockers, photo kiosks, automated car washes, self-storage, self-operated dog washing stations, and more.

Ultimately, a simple business using a straightforward business model that you are passionate enough to get your hands dirty in, and have enough specialty knowledge (or knowledge in general) to operate the business now or very soon.

Cody Sanchez’s book Main Street Millionaire is a great, simple, and straightforward book to start the brainstorming process for ideas like these.

3) Use location strategy as a lever

The pure approach to using location to lower your cost of living to either improve your quality of life or boost savings and investment is Expat FIRE. You don’t have to be “Expat FIRE” forever to benefit from geoarbitrage. A 2–5 year period in a lower-cost, high-quality base can function like a turbocharger for savings.

Additionally, you don’t have to move abroad to make geoarbitrage work for you. Moving from New York City to Houston, Texas, while keeping 80% of your salary, creates a lot of margin between your living costs and take-home pay. Changing your location to change the structure of your life and your expenses can be the move that creates the margin that leads to Chubby FIRE.

Common FIRE investment strategies

Chubby FIRE investing should be boring on purpose – because you’re playing a long game and the goal is durability, not dopamine.

A clean default approach to choosing “FIRE-friendly investments” is to use the following criteria:

- Diversified, broad-market exposure

- Low fees

- Consistent contributions

- An allocation you can hold through ugly years

- Simple setup that is easy to manage

Though there are many permutations of the right investment portfolio for you, many FIRE followers opt for broad market ETFs that can be purchased and traded easily through their preferred brokerage account, with low fees, automated, and (within each ETF) cover the larger and trusted US and global markets

If you add complexity (real estate, concentrated positions, private deals), do it because:

- You understand the risks, how to manage them, and how to use them to your advantage

- The numbers work, and work better than the simpler investing options

- You’re not quietly turning your retirement plan into a second job

Chubby FIRE portfolios fail less from “bad investments” and more from panic selling, overcomplication, hidden (or unacknowledged) fees, and spending drift that quietly outpaces the plan. By keeping it smart and simple, you’ll like in a resilient, solidly performing portfolio that, with discipline, will be easy to ride through down markets.

To build the right portfolio for your FIRE plan, your risk tolerance and capacity, and your needs, consider speaking with a fee-only advisor, and be sure to educate yourself on personal finance and investing with this summary of essential personal finance books.

Risks & Realities of Chubby FIRE, and how to mitigate them

Chubby FIRE is safer than Lean FIRE in one sense: more margin.

But it’s riskier in another sense: it’s easier to drift into a lifestyle you can’t defend.

The key risks of Chubby FIRE are:

- Lifestyle creep disguised as “I earned it.” Mitigate this by defining “enough,” setting guardrails, and tracking the few categories that actually move the needle (housing, vehicles, travel).

- Sequence of returns risk (bad early market years). Mitigate this by planning a buffer, exercising flexible spending, choosing a conservative withdrawal rate upfront, and maintaining an income option even into retirement.

- Tax drag (especially on large taxable portfolios and high-income years). Mitigate this by planning an efficient account strategy early, planning smart withdrawal sequencing, looking into how to optimize tax via location, consulting a tax strategist to carve in the smart details, and real planning.

- Healthcare and aging costs. Mitigate this by treating your healthcare as a system, not a line item. Build honest healthcare costs, accounting for again, into the number. Practice proper prevention and plan a lifestyle that aligns with such.

- Complexity creep (multiple properties, businesses, “passive income” that isn’t passive). Mitigate this by keeping your income engine simple unless complexity is accepted with intention, after clear calculation, and clearly pays you more than simpler options while accounting for the additional effort and headache.

Chubby FIRE is not “set it and forget it.” It’s “set it, protect it, and check it as your retirement depends on it.”

Chubby FIRE vs. FAT FIRE vs. Lean FIRE

Chubby FIRE

- Comfort + margin: not extreme frugality, not luxury-for-luxury’s-sake

- Balanced lifestyle: travel, dining, hobbies, and convenience within limits

- Best for: people who want early retirement with a “normal, comfortable” life

- Main tradeoff: requires higher income and/or a longer runway than Lean FIRE

Lean FIRE

- Essentials-first: low spending by design

- High simplicity: fewer moving parts, fewer luxuries

- Best for: people who value time freedom more than comfort upgrades

- Main tradeoff: low margin for error (surprises hit harder)

Fat FIRE

- High discretionary spending: premium lifestyle with fewer constraints

- More complexity: taxes, estate planning, multiple income streams/assets often matter more

- Best for: high earners/owners who want maximum optionality and comfort

- Main tradeoff: bigger number, more management, and lifestyle creep risk if not intentional

FAQ

What is the difference between fat fire and chubby FIRE?

Fat FIRE is maximum comfort and discretionary spending with fewer constraints – usually a bigger number and more complexity. Chubby FIRE is comfort + margin without trying to fund everything forever.

What net worth is Chubby FIRE?

Common shorthand ranges float around $2.5M to $5M, but this number is actually invested assets generating passive income, not net worth.

What is chubby FIRE retirement?

It’s early retirement (or work-optional living) where your lifestyle still feels comfortable: travel, hobbies, housing choices, and a buffer — without needing Fat FIRE-level assets.

What does fat fire mean?

Fat FIRE typically refers to financial independence at a level that supports high discretionary spending with fewer constraints — often requiring a larger portfolio, more planning complexity, and stronger income engines.

.

.

ABOUT THE AUTHOR

Carlos Grider launched A Brother Abroad in 2017 after a “one-year abroad” experiment turned into a long-term life strategy. After 65+ countries and a decade abroad, he now writes about FIRE, personal finance, geo-arbitrage, and the real-world logistics of living abroad—visas, costs, and tradeoffs—so readers can make smarter global moves with fewer surprises. Carlos is a former Big 4 management consultant and DoD cultural advisor with an MBA (UT Austin) and Boston University’s Certificate in Financial Planning. He’s the author of Digital Nomad Nation: Rise of the Borderless Generation and is currently writing The Sovereign Expat.