Most people want financial independence and the opportunity to retire early. Unfortunately, the small margin of savings that many Americans have after paying the bills doesn’t make it easily possible to early retire with $2 million in the bank, or an $80,000 retirement withdrawal. But luckily, the solution doesn’t have to be working forever, or finding a cheat code to save millions. An alternative solution is designing your life to need less. This is the Lean FIRE approach to Financial Independence.

Within the FIRE movement, a trend is emerging of rejecting unquestioning consumerism and intentionally designing a more efficient life – with less waste, fewer expenses, and a smaller, leaner FIRE number in the process.

Choosing to FIRE lean isn’t about deprivation – it’s about design.

While Lean FIRE is often labeled as an extremely frugal lifestyle, that label isn’t accurate. Up until 1979, the annual consumption of the average American was naturally low enough that a Lean FIRE retirement would cover it – a mere $~29,000 in today’s dollars (inflation adusted). This often overlooked hides a truth, and an opportunity. Unquestioned lifestyle creep, near automatic consumption, and upgrade culture (without intention) are what many back from the prospect of financial independence.

The beauty is that knowing this empowers you to make the choice, of how you consume, intentional from now on. Even better, intentional consumption, or deliberately not consuming, can be your key to an easy, minimalist approach to early retirement.

Lean FIRE isn’t about extreme frugality or austerity. It’s driven by intention, to turn the dial back on consumption the moderation of times past, and gain time and financial independence in return.

In this complete guide to Lean FIRE, we’ll break down the quick path to FI by choosing less of what you don’t need and more of what matters to you.

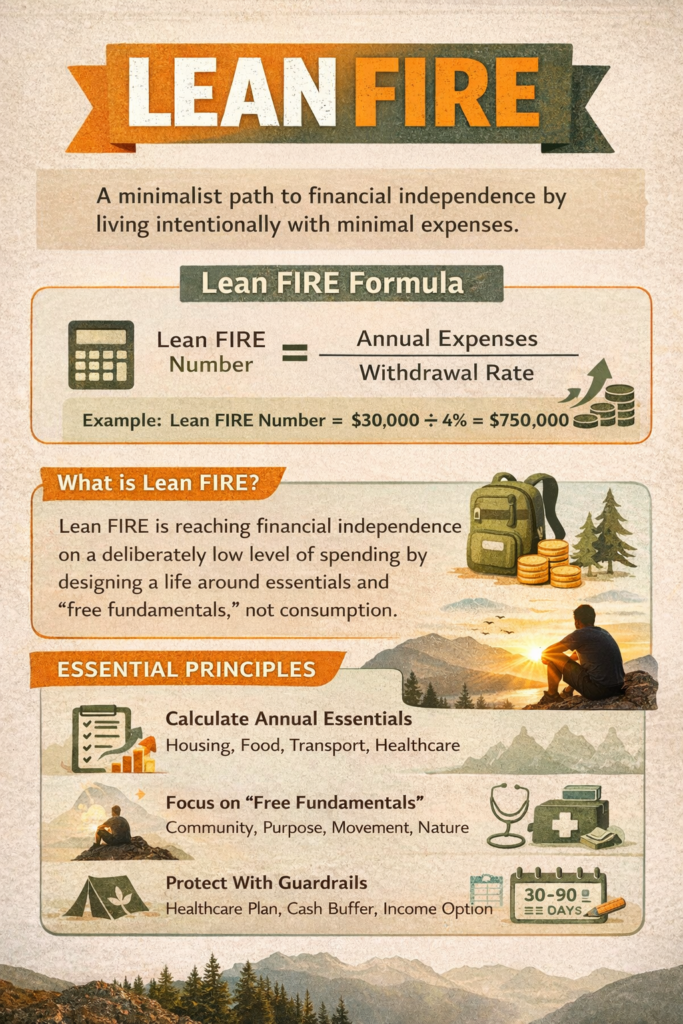

Lean FIRE at a Glance

The Idea:

Lean FIRE is reaching financial independence on a deliberately low level of spending, by designing a life around essentials and “free fundamentals,” not consumption.

The equation:

Lean FIRE Number = Annual Expenses ÷ Withdrawal Rate

A Quick Example of Lean FIRE:

If you can live well on $30,000/year and use a 4% rule, your Lean FIRE number is about $750,000. 🡪 ($750,000 FIRE Number = $30,000 annual expenses ÷ 4% annual withdrawal rate)

The Approach:

Use the Lean FIRE Calculator to run your numbers.

The Simple Lean FIRE roadmap:

- Define your “Lean, but livable” lifestyle (what you keep, what you cut, what you refuse to cut).

- Calculate your real annual essentials (housing, food, transport, healthcare, buffers).

- Validate that you can live enjoyably on a “Lean FIRE” passive income

- Pick a withdrawal-rate assumption (4% / 3.5% / 3%) and stress-test it.

- Design the “free fundamentals” into your lifestyle (community, purpose, nature, movement) so life still feels rich.

- Build guardrails to protect against surprises (healthcare plan, cash buffer, flexible income option).

- Test-drive the lifestyle for 30 to 90 days, then adjust before you commit.

Key Points for Lean FIRE Success

- Lean FIRE requires a minimalist and lean lifestyle, which, in reality, requires unconventional living or relocation for most.

- Lean FIRE success is about mindset and habits.

- Healthcare planning is the most significant trap that Lean FIRE planners miss.

- Location selection and life design are levers that empower Lean FIRE

- By nature, Lean FIRE only covers food, transportation, and housing, with no extra financial room for luxuries

- Lean FIRE requires designing a life wherein the other “healthy essentials” are created, or available, for free

- Successful Lean FIRE requires honesty with yourself about the level of comfort you need (and can do without) and what you’re willing to sacrifice in return

- Existing on a “Lean FIRE income” has been the norm, up to the 80s, and has only become a lifestyle requiring “intention” and “compromise” in the face of unquestioned, modern lifestyle creep.

Disclaimer: This content is for educational and informational purposes only and is not individualized financial, tax, or legal advice. I don’t know your personal situation, and reading this does not create an advisor-client relationship. Consider consulting a qualified professional before making financial decisions, and invest based on your goals, time horizon, and risk tolerance.

Assumptions Notice: Examples and calculator outputs are hypothetical, based on user inputs and assumptions (e.g., returns, inflation), and actual results will vary

Table of Contents

What is Lean FIRE?

Lean FIRE is the minimalist approach within the “Financial Independence, Retire Early” (FIRE) movement, but it’s not just “spend less.” The “lean approach” is built on a deliberate decision to design and practice a life where your baseline expenses are low enough that a relatively modest portfolio can cover them.

It’s choosing a life that works on purpose, with intention, and designed with minimal “waste”: fewer paid conveniences, fewer expensive defaults, fewer “automatic” upgrades, and more of the things that are often free when you build your days around them: community, nature, purpose, movement, and healthy routines. The “free fundamentals” are what make Lean FIRE not only possible, but fulfilling and sustainable.

Lean FIRE is also defined by what it is not:

- It’s not a vow of misery. If your plan requires constant suffering, it isn’t sustainable and won’t last.

- It’s not “I’ll just be more disciplined.” Motivation and pure grit are unreliable at best. Systems are reliable, and what Lean FIRE is built on.

- It’s not a loophole that eliminates adult responsibilities, such as taxes and healthcare. Those are still part of the plan and must be factored in.

- It’s not a moral identity that justifies itself, such as “I’m better because I spend less”. It’s a strategy that must work for your life, your needs, and your goals…or it is pointless.

At its best, Lean FIRE is a clean trade. You trade the personal sacrifice of less consumption. In return, you receive something most people never get back – or more accurately, you “regain” time and control.

Lean FIRE numbers: $25k per year and what that means in real life

Lean FIRE only becomes a real possibility the moment you stop treating it like a potential “philosophy” and start testing it like a budget.

In practice, the Lean FIRE approaches to financial independence apply when someone aims for a lean annual spending target. This “Lean FIRE number” is often somewhere in the range of $25,000 to $40,000 per year (per person). However, the exact number depends on where you live, how you live, and what you consider “non-negotiable.” The range is wide because life is wide:

- A rural or small-city setup can make the same spending feel calm and spacious.

- A major coastal city can make that number feel like constant friction with no margin for error.

- A couple sharing housing costs changes the math dramatically.

- Kids, chronic medical costs, and fixed obligations change it even more.

The key point: Lean FIRE isn’t one number. It’s a level of spending that’s low enough that your portfolio target stays under the “traditional FIRE” bracket, and thus requires non-traditional FIRE approaches to make it possible. This lean FIRE number is often under $1,000,000 (which is the equivalent of a ~$40,000 per year retirement withdrawal), depending on assumptions and household size.

At the same time, a creative Lean FIRE type may get by on $625,000 net assets, roughly equivalent to a $25,000 per year withdrawal, via homesteading, ExpatFIRE, or creative approaches like RV Life, Van Life, and shared living situations.

The honest version is this:

Lean FIRE only works when your essentials are truly covered without undue stress, and when your life still contains enough “richness” that you don’t rebound into lifestyle inflation the moment you get bored, lonely, or exhausted.

That’s why location strategy matters (and why Lean FIRE often overlaps with Expat FIRE and Nomad FIRE). If your housing and healthcare are structurally expensive, there is no financial room for the remaining essentials, or surprises, and Lean FIRE stops being “design” and turns into “pressure.” However, if those base costs of housing and essentials drop due to how you structure life more efficiently, Lean FIRE starts to function in a sustainable, goal-achieving way.

Lean FIRE Portfolio Targets Based on Spending

What does the common annual Lean FIRE withdrawal rate (to cover expenses for the average Lean FIRE budget) look like?

|

Annual spending |

Portfolio at 4% |

Portfolio at 3.5% |

Portfolio at 3% |

|---|---|---|---|

|

$20,000 |

$500,000 |

~$571,000 |

~$667,000 |

|

$25,000 |

$625,000 |

~$714,000 |

~$833,000 |

|

$30,000 |

$750,000 |

~$857,000 |

$1,000,000 |

|

$35,000 |

$875,000 |

$1,000,000 |

~$1,167,000 |

|

$40,000 |

$1,000,000 |

~$1,143,000 |

~$1,333,000 |

This table gives a rough idea of assets to plan for based on your situation, not a promise. Your real plan needs to account for:

- Healthcare (the hinge)

- Inflation (your quiet enemy)

- Sequence-of-returns risk (bad early years)

- Your investment portfolio and expected returns

- Whether your spending target is actually realistic for your setup

That’s why you run the calculator and pressure-test assumptions instead of betting your future on one clean spreadsheet.

Lean FIRE in one equation

Lean FIRE is conceptually simple:

Lean FIRE Number = Annual Expenses ÷ Withdrawal Rate

Or this can also be calculated as…

Lean FIRE Number = Annual Expenses x 25

Using the “multiple” rule, use “25x” for a 4% withdrawal rate in retirement, 29x for 3.5%, and 33x for a 3% withdrawal rate

Everything else is making sure “Annual Expenses” is honest and “Withdrawal Rate” is conservative enough for your risk tolerance.

A few notes so you don’t misuse the simplicity:

- Expenses are the truth. If you undercount housing, healthcare, taxes, or “annual surprises,” Lean FIRE turns fragile fast.

- Withdrawal rate is your margin dial. 4% is the classic shorthand; 3.5% and 3% buy more resilience but require more assets.

- Your plan should survive real life. Not just the average year—the bad year, the boring year, the “I need dental work” year, the “rent jumped” year.

If you take nothing else from this: Lean FIRE doesn’t fail because the equation is wrong. It fails because people try to live a life they can’t actually support—then call it “discipline” when it’s really a design flaw.

Basic FIRE Math Refresher

The 4% rule for safe withdrawal rates based on the Trinity Study translates to the 25x rule – meaning 25x your annual expenses equals your FIRE number.

Note that 3% and 3.5% withdrawal rates may be more appropriate for long retirements (30+ years) or intentions of leaving inheritances to create multi-generational wealth.

Read the article on Traditional FIRE for a full refresher of the Simple Math Behind FIRE.

Lean FIRE calculator

The Lean FIRE calculator exists for one reason: to turn the idea into numbers you can stress-test.

Use it to:

- Estimate your Lean FIRE number under different withdrawal rates (4%, 3.5%, 3%)

- See how sensitive your plan is to small spending changes (because in Lean FIRE, small changes matter)

- Pressure-test your assumptions before you redesign your life around them

Use the Lean FIRE calculator here.

And one practical recommendation: run it in ranges, not single points. Lean FIRE planning is less about “the number” and more about how the plan behaves when the world doesn’t cooperate.

How Lean FIRE actually works

Lean FIRE has a mechanism – and it’s not “be frugal forever.”

Lean FIRE works when two requirements are true at the same time:

1) Lean FIRE covers the essentials (food, housing, transportation) with slack you can live with.

Lean FIRE, by nature, covers the basics. Housing, food, transportation, healthcare, and a buffer should be automatically covered by passive income in a non-variable way. For this reason, situations that lend themselves to Lean FIRE have more “structure.”

For example, a Lean FIRE follower that owns a cabin in the woods of Washington with an “old reliable truck” and loves nature eliminates rent, surrounds themselves with value, and has fewer variable expenses.

Much the same, a homesteader who owns their home in New Mexico and produces their own food eliminates the financial burden for essentials – though they arguably pay in sweat equity.

Another realistic example is a person who owns a home in a walkable neighborhood, with community and green spaces, and with the added leverage of low property taxes, no HOA fees, and solar panels, ensures that even if housing costs, energy costs, or general neighborhood costs spike, theirs don’t.

Though these situations don’t leave much room for financial “oops,” they are structured to ensure the essentials are covered and are likely not variable. Beyond this “foundation,” it is essential you either build slack into the plan or you build flexibility into your life (location flexibility, income flexibility, spending flexibility).

2) You design a life that delivers the “free fundamentals” and the healthy essentials for free (community, purpose, nature, health).

This is the part people skip, and it’s why Lean FIRE fails when it becomes purely financial.

In the examples above, the person who lives in the cabin in the woods (assumed to be a solitary person) is immersed in what they love – nature. The person who owns the home in a walkable neighborhood, with community and the festivities that come with it, stays connected, active, and entertained without additional cost. And the homesteader, though life may not be easy, can find satisfaction in purpose. Each of these examples underpins a key aspect of Lean FIRE – the personality of the person choosing it must fit the “structure” of the lifestyle, and without the needs of that personality, the life they design must still be fulfilling within the financial and structural constraints of a Lean FIRE life.

If your “lean” plan removes the things that make life feel worth living, such as community, purpose, healthy diversion, nature, and movement, you don’t get a peaceful minimalist life. You get a weird psychological pressure cooker that eventually explodes into spending.

This is why I keep coming back to the same idea: Lean FIRE is a lifestyle architecture project.

Money is the constraint, but it’s not the point.

The tradeoffs are real, and you don’t need to pretend otherwise:

- You’ll likely compromise on housing size, location, and convenience.

- You’ll probably trade paid entertainment for built-in enjoyment (parks, walking cities, friends, hobbies).

- You may choose DIY and repair over replacement.

- You’ll need a serious plan for healthcare and “unknown unknowns.”

Lean FIRE isn’t about living small. It’s about living intentionally—and refusing to let inflated defaults dictate how many decades you have to sell.

Additionally, living the Lean FIRE life successfully requires acknowledging the compromises upfront.

The Realities and Sacrifices of Lean FIRE

With small budgets come the compromises, some of which are listed above, and include location, house size, and “extra activities.” While you may be able to live in the city or afford having 3 kids, you may not be able to do both on a Lean FIRE budget. That fact isn’t inherently bad; it is actually a valuable tool to help you screen whether the Lean FIRE life is, in fact, perfect for you and your direction, or if another approach to FIRE** would be better.

The major compromises to know about in Lean FIRE, and that overlap poorly, are:

- Difficult to have kids

- Difficult to live in a major city

- Many people who Lean FIRE actually Barista FIRE supplementing their income

- Difficult to have a big house in a conventional life

- May require shared living or alt living (van life, RV life, shared living, or a cabin in the woods)

- Likely requires settling for low-cost cities (e.g., Tulsa, Gulfport, Mobile)

- Big “one-time events” commonly forgone, like annual vacation

Why FIRE Lean?

Lean FIRE appeals to people who want the core promise of FIRE, time and autonomy, without signing up for the modern version of “success” that requires endless earning, endless upgrading, and endless background stress.

The benefits are straightforward:

- You can reach FI with a smaller portfolio.

- You can reduce the years you’re forced to play defense at work.

- You create more control earlier, not later.

- You escape the treadmill where every raise becomes a new obligation.

But Lean FIRE only makes sense if you’re honest about why it feels “hard” now.

The real lever: Lifestyle inflation and why Lean FIRE feels “hard” now

Lean FIRE isn’t new. What’s new is what people think is “normal.”

A few generations ago, a lower-consumption lifestyle wasn’t a radical identity. It was just… life.

Inflation-adjusted, what the average person in the 1970s consumed was $29,200 each year – adjusted for today’s dollars. This means that the average person’s life during the 1970’s, with no extra force or intention, was a Lean FIRE lifestyle.

By comparison, today, the average person consumed $60,413 per person per year (≈ $5,034/month) in 2025.

(Note: Calculations based on public data from the Bureau of Economic Analysis Personal Consumption Expenditures (PCE) per capita and CPI data – see footnotes for details)

1970 to 1979 Consumption Per Person, Adjusted for Inflation to 2025

|

Year |

PCE per capita (nominal $) |

In “today’s” $ (≈ Dec 2025) |

|---|---|---|

|

1970 |

$3,153 |

≈ $26,300 |

|

1975 |

$4,771 |

≈ $28,700 |

|

1979 |

$7,043 |

≈ $31,400 |

- This table depicts inflation-adjusted per-person consumption translated to “today” dollars ≈ Dec 2025 dollars

- 1970s average (1970–1979): ≈ $29,200 per person per year, or ~$2,440/month.

The problem, as to why for most the idea of a “Lean FIRE life” feels austere, is clear – our baseline expectations have moved.

The 1970’s were a time that predated Starbucks, annual iPhone and laptop upgrades, fast fashion, and endless subscriptions – at the same time (due to the lack of portability with phones), filled with more nature, built more around activity, community, nature, and the outdoors.

Today, we carry more subscriptions, more devices, more services, bigger housing expectations, bigger car expectations, with more “convenience spending” and unnecessary upgrades than most people realize—until they try to remove it. From 1970 to 2021, the size of the average American home ballooned from 1500 square feet to 2500 square feet according to the American Enterprise Institute while the birthrate (number of people living under a single roof) has dropped by 30% in the same period.

This is why Lean FIRE can feel extreme: not because the human needs changed, but because the default lifestyle has.

This isn’t ‘the cost to survive.’ It’s a proxy for “what we FIRE feels harder now.”

So, the story isn’t “people are dumb and buy lattes and avocado toast.”

The story is: modern life quietly sells you a package, then tells you that package is the minimum viable existence. Lean FIRE is built on becoming aware of that, openly acknowledging it, and then making the decision to opt out.

The deeper point: Lean FIRE succeeds when you stop trying to “discipline” yourself into a smaller life and instead build a life where “smaller” feels not only normal, but better: simpler days, fewer payments, fewer obligations, more time, more walking, more friends, more real food, more sunlight. That’s not a downgrade. That’s a different definition of wealthy.

Where Lean FIRE works best

The goal of financial independence on a lean budget can be achieved if you make your lifestyle (and overall costs) fit the numbers. As costs for the same elements of living vary by city, state, and country, there is an opportunity to make a Lean FIRE life possible, specifically by moving to a location where the costs of living naturally fit the Lean FIRE constraints.

With this tool in mind, the lever of optimizing location works to drastically reduce expenses because it directly influences three big costs: housing, transportation, and healthcare. These three elements, and their average costs, are structurally higher or lower based on the location chosen.

For instance, housing is naturally higher cost than the US average in New York City and inherently lower cost in Beloxi, Mississippi.

Transportation costs are naturally cheaper in walkable cities with robust public transportation, like Tulsa, Oklahoma, and Portland, Oregon, and more expensive in car culture states with high gas prices, such as California, Hawaii, and New York.

Healthcare costs are inherently more expensive in states that legislate accordingly such as Vermont, South Dakota, Tennessee, and Texas, while being vastly cheaper in state that legislate for accessible healthcare, such as Oregon, Pennsylvania, and Washington D.C. according to the Journal of Consumer Affairs, and additionally being “accessibly cheap” in California, Arizona, and New Mexico as border states to Mexico making affordable medical tourism accessible in Mexico.

The insight from this is understanding that changing your location makes these essential expenses easier to control and structurally lower in cost.

With the possibility of mobility as a cost-reducing tool, the new question is, where can one go to lower their costs of living in the U.S.?

In the U.S., Lean FIRE tends to work best in:

- Regions with lower housing pressure (smaller cities, certain rural areas, places with less “status pricing”)

- Setups that reduce car dependence (walkable pockets, bike-friendly areas, smaller footprints)

- Communities where you can build “free fundamentals” without paying for them (parks, trails, libraries, community spaces)

Anyone pursuing Lean FIRE has the opportunity of priceless location independence, if they can make the math work. If you are trying to make the Lean FIRE math work, consider trading in high-cost regions, like the western and eastern coastal regions of the United States, for the Midwest, the heartland, and the southern United States for an immediate drop in costs.

Then, from the popular urban centers that generally attract large companies that pay high salaries and drive up the cost of living, consider either trading down for suburban and rural life in a less competitive area or trading up for a specific neighborhood that is walkable and self-contained, and by nature reduces your cost of living by delivering more living without additional cost.

If you have an opportunity to trade in your current location for a cheaper one, start by searching for low-cost, high-quality-of-life city replacements in Tennessee, Oklahoma, New Mexico, Texas, Mississippi, Alabama, Arkansas, and Florida. No matter what you want in life – mountains, beaches, bohemian university towns, or simply livable middle America, these states all have an option at a fraction of the cost of the rest of the country.

And then there’s the leverage many people ignore: Moving abroad to exchange for a lower-cost country.

Lean FIRE becomes dramatically more viable with location strategy – and often, moving domestically doesn’t deliver nearly as much leverage as moving abroad. While Tulsa, Oklahoma, has half the cost of living of New York City, and is more livable than most expect, Bangkok is still 25% cheaper than Tulsa. If you are already arranging the logistics for a move to empower your FIRE strategy, research the Expat FIRE approach to make your Lean FIRE ambitions even more possible.

Thanks to the role that geography and geoarbitrage play in how successful your setup is within a Lean FIRE life, a life abroad presents some unique opportunities to live a Lean FIRE life more comfortably.

- If you want “Lean FIRE but livable,” Expat FIRE is a path to unlocking countless livable locations for cheaper than even “cheap life” in North America.

- If you want flexibility and seasonal cost control, Nomad FIRE can be an option, allowing the pressure release valve of mobility.

Lean FIRE isn’t only about spending less. It’s about placing yourself in a context where spending less is easy.

Risks, downsides, and essential mitigations in Lean FIRE

Lean FIRE has real upside, but it also has less margin for error. That’s the trade. If you want the freedom, you have to respect the fragility.

The big risks with the lean approach:

- Healthcare: The hinge. If your healthcare plan is vague, your Lean FIRE plan is vague.

- Inflation: Especially for non-negotiables like housing and medical costs.

- Sequence-of-returns risk: Bad early market years can stress a lean portfolio.

- Lifestyle drift: Boredom, loneliness, or “I deserve it” spending that slowly breaks the budget.

- Underestimated expenses: The classic Lean FIRE failure mode is a fantasy spreadsheet.

- Burnout risk + identity risk: Burning out on frugality with no easy way “back in” to change it is a very real possibility as you grow and your desires and needs change, while already in a “Lean FI” life.

Essential Mitigations

Lean FIRE doesn’t need to be reckless. You can compensate for budget by putting in the energy to mitigate possible risks and build guardrails into your Lean FIRE approach:

- Test it: Try the lifestyle before you buy and commit, allowing a change of course before you’re “too far from shore.”

- Healthcare first, not last. Get clear on coverage, worst-case costs, and what your plan is if you move. Be honest and recognize that if health and health coverage are the factors that break when stress testing your Lean FIRE plan, you can’t FIRE lean. Simple as that.

- Run conservative assumptions. 3.5% or 3% may be more appropriate for long timelines if you plan to be retired longer than 30 years or you are planning to build multi-generational wealth by leaving an inheritance. Use the calculator to test multiple scenarios and compare.

- Carry an appropriate buffer. A cash reserve isn’t “inefficient” when it prevents forced selling in bad markets.

- Keep an “income option” alive. Even a small, flexible income can turn Lean FIRE from fragile to calm. This is where Barista FIRE can bolt on in a smart, fulfilling way. Maintaining a side hustle is an excellent financial pressure release and a great way to maintain marketable skills.

- Design the environment. If your plan relies on constant willpower, redesign the plan.

- Escape hatches: Barista FIRE, seasonal work, and options for transitioning out of Lean FIRE, either to a different form of FIRE or by returning to normal life “easily” are invaluable options as we grow and change. If Lean FIRE lasts for just a season, a good Lean FIRE plan allows for a smooth transition back out.

- Annual review: During the accumulation phase and in FIRE, assessing assets, investment performance, withdrawal rate suitability, satisfaction in life, and changing life needs are prudent for timely “tune-ups” to the living guide that is a good Lean FIRE plan. The economy, your assumptions, your current investment performance, withdrawal rates, inflation, whether or not you’re burnt out on the frugal lifestyle, and healthcare needs are all excellent points to review and assess annually.

Lean FIRE isn’t about proving toughness. No one’s frugality willpower is tough enough to withstand every possibility life can throw at it. Lean FIRE is about building a system that survives real life.

Healthcare: The elephant in the room and the linchpin in plans

Of the “hiccups” reported by those who had difficulty executing Lean FIRE, or any FIRE, unplanned expenses while aging are the most common and detrimental issues.

To avoid the sabotaging effects that ignoring health needs and their costs can have, be honest about your healthcare needs now. If your health needs make lean FIRE prohibitive, be honest and don’t put your health at risk.

Additionally, just like the foundations of Lean FIRE require the essentials to be covered and as many of the fundamentals to be low-cost as possible, leverage the value of prevention by investing in your health early. An ounce of prevention is worth a pound of cure, and healthy, active lifestyles are naturally lower cost. Getting the appropriate check-ups, taking ownership of your nutrition, proactive self-care, and leveraging the science-proven benefits are investments in your health that will pay dividends later.

As a tertiary option, consider medical tourism to keep health care quality high and costs low, while also considering Barista FIRE as a path to continuously maintained healthcare, even if financial hiccups arise.

The hard reality is – Lean FIRE can work, but only for the right person. I know this from experience.

In exploring ideas across the internet on Lean FIRE, who it works for, who it hasn’t, and the practical insights that can be gleaned from each anecdote and experience, I stumbled upon the Financial Samurai blog (written by Sam) very opinionated on Lean FIRE and why he believes Lean FIRE can’t work.

I loved reading the Financial Samurai’s write-up, as it was informative, from someone with a very informed perspective on all things personal finance and FIRE-related. At the same time, it’s important to note that his perspective is one from someone who Fat FIRE’d in one of the most expensive cities in the US (I believe San Francisco). His annual passive income was last reported as $310,000, which translates to an estimated net worth of $7.75 million based on commonly accepted FIRE principles. More importantly, Sam FIRE’d from a high-expense lifestyle. To someone like Sam, assessing the possibility of living on a $25,000 “Lean FIRE income” would understandably feel like poverty or austerity. But the key point to highlight is, this is likely very accurate – for him.

For Sam of the Financial Samurai to acknowledge this is insightful, aware, and exudes the kind of non-romantic assessment that every potential FIRE follower needs to apply to their prospective plan. Even if it means that their plan isn’t feasible, with the current life structure, and the demands and unacknowledged expectations that might come with it.

In the Financial Samurai’s Lean FIRE post, I could sense the bias in his opinion. A very valid perspective that people should be listened to, for the kind of insight that can come from listening to any anecdote. But I offer a contrasting perspective from someone who did taste the high-earning white-collar life – and found more happiness in rustic simplicity.

Currently, I am writing from a café in Buenos Aires, where I’ve lived for the last 6 months. In those 6 months, the expenses for my partner and me have totaled less than $2,000 each month – roughly $24,000 a year, and well within the Lean FIRE thresholds. living in one of the most expensive neighborhoods in the country, eating out daily, live music often, gym memberships, and sparing no expense. A Lean FIRE lifestyle, facilitated by the levers of geoarbitrage and the bolt-on option of Expat FIRE.

In the months prior to moving to Buenos Aires, we lived in Thailand for roughly $1800 per month (~$22k per year).

Then, before leaving the US, living in Dallas, my life was filled with an apartment in a walkable, hipster neighborhood, vacations camping in National Parks, and a social life that revolved around Italian-style dinner party hosting at home. The cost of this life, underpinned by minimalism, an aversion to debt and new cars, and a “buy it for life” approach to everything, added up to between $2500 and $3000 per month before my travels. While Lean FIRE is understandably not feasible for a married former finance professional with two children living in San Francisco, I am proof that, as a single, adventurous person who prioritizes health & fitness, the outdoors and nature, and experiences, Lean FIRE can work, if you, your preferences, and your life are structured for it.

At the moment, I wander the world and can change my location to fit the budget that I want. But, if location independence isn’t in the cards for you yet, what are the best ways to make Lean FIRE work for you?

Here is how Lean FIRE could work

- Homesteading

- Cabin in the woods approach: Rustic simplicity, taking pleasure in nature

- Lean FIRE underpinned by a paid-off home

- Expat FIRE alternated with, or in conjunction with, Lean FIRE

- Barista FIRE

- RV life – thinking outside the box (US summers, Baja Mexico, and Central America winters)

Mind you, none of these are conventional paths suitable for the average person. The middle point between the Financial Samurai’s opinion and the reality of my situation is that Lean FIRE is a conscious mindset tool and approach for the right person.

Who Lean FIRE is best for (and who it isn’t)

Lean FIRE can be a powerful tool and is great for a specific kind of person, but it won’t work for everyone.

Lean FIRE tends to fit best for people who are:

- Minimalists and essentials-first types: You genuinely prefer simple days to expensive days

- DIYers, creative problem solvers, and self-sufficient types: you’ll fix, cook, walk, and learn instead of buying convenience

- Not status-motivated: You don’t need to perform to the societal standard of success to feel successful

- Adventurous & open-minded: You can redesign your norms without panicking

- Light on fixed obligations: Fewer dependents, fewer rigid payments, fewer immovable anchors

- Healthy enough for a loose plan: Not “perfect health,” but realistic about medical costs and needs

- Alt living movement enthusiasts: Those open to tiny house, van life, homestead living

- The flexible and adaptive by nature

- Nature and community lovers over consumers

Lean FIRE tends not fit people who:

- Have high fixed housing costs they refuse to change

- Have significant ongoing medical needs without a rock-solid healthcare plan

- Want a high-discretionary lifestyle but assume they can go “lean” at will

- Rely on comfort spending to regulate stress – because Lean FIRE removes that outlet

The reality is Lean FIRE might work, but only for the right person.

Not because they’re special, but because their preferences and life structure naturally fit the constraints inherent to the Lean FIRE strategy.

How to Lean FIRE: The 6-step roadmap

Lean FIRE is a numbers game and a lifestyle game. This roadmap has to cover both.

The Lean FIRE Roadmap

- Define your Lean lifestyle, and be honest about your non-negotiables. What stays? What goes? What do you refuse to sacrifice (health, relationships, nature, movement)?

- Build your essentials budget, honestly. Housing, food, transport, healthcare, taxes, and a buffer for “real life.” If you’re guessing, you’re not planning.

- Choose your assumptions and run the Lean FIRE calculator. Pick a withdrawal-rate range (4% / 3.5% / 3%). Stress-test. Don’t worship one output.

- Engineer the expenses, not just the mindset. Lean FIRE becomes easy when housing and transportation stop being silent killers. Change the structure.

- Invest simply and consistently. The default FIRE engine is diversified, low-fee index exposure aligned with your risk tolerance. If you’re doing something more complex, do it with eyes open (and ideally with professional guidance).

- Test-drive the lifestyle (30–90 days), then iterate. The dry run is where you find the hidden costs, the psychological friction, and the points of failure—before you bet years on the plan.

- (Essential Bonus) After achieving Lean FIRE: Annual check-ins. Not because you’re obsessive, but because Lean FIRE is a system with variables: inflation, markets, health, and life changes.

An Encouraging Truth: If the plan feels too tight, you don’t have to abandon FIRE. You can blend.

Lean FIRE can bolt into Barista FIRE, Expat FIRE, or Coast FIRE, depending on what lever you want to pull next.

The Lean FIRE Investment Approach

When your plan is built on a smaller number—and a smaller margin for error—your portfolio doesn’t need to be clever. It needs to be durable. It needs to survive boredom, bad headlines, inflation, a medical surprise, and a couple of ugly market years without forcing you into panic decisions that break the plan.

So, the Lean FIRE investment approach is “boring on purpose” for the same reason commercial airplanes are boring on purpose: the goal isn’t to impress anyone. The goal is to arrive.

A Lean FIRE portfolio has one core job: capture market-like returns over time with as little leakage and self-sabotage as possible.

That means it must:

- Stay diversified (so one sector, one company, or one theme can’t ruin your decade)

- Stay low-fee (because fees compound against you the same way returns compound for you)

- Stay simple enough that you can hold it through drawdowns without constantly second-guessing yourself

And it must not:

- Depend on market timing, stock picking, or “one weird trick.”

- Depend on you being “disciplined” every day for the next 20–40 years

- Depend on perfect conditions (steady inflation, smooth markets, stable health costs)

Lean FIRE works when the lifestyle is intentionally designed—so the portfolio can quietly do its job in the background.

The default Lean FIRE engine: diversified, low-fee index investing

For most Lean FIRE plans, the cleanest approach is the classic FIRE approach:

A diversified portfolio using broad market index funds / ETFs with low expense ratios, held for the long term, aligned with your risk tolerance and your ability to stay invested when markets get ugly.

In plain English:

- Broad market exposure (not a basket of “favorite” stocks)

- Diversification across sectors – and often across geographies if it fits your plan

- Low fees so compounding doesn’t leak out through expense ratios and unnecessary trading

- Automated saving, because Lean FIRE breaks when the plan relies on motivation

If you want the simple rule: the common FIRE math assumes you’ll earn market-like returns over time. To achieve this, you must build a portfolio designed to pursue that—without adding fragility.

Lean FIRE investing isn’t about maximizing returns.

It’s about building a portfolio you can hold, through real markets, while living a life you actually like—one where your essentials are covered, your fundamentals are rich, and your plan doesn’t collapse the first time the world gets messy.

The Difference Between Lean FIRE and Other Types of FIRE

Lean FIRE is not “better” than other FIRE types. It’s simply the most essentials-first version of the strategy. The differences are mostly about margin, flexibility, and what you’re optimizing for.

Traditional FIRE is “portfolio covers the lifestyle.” It’s bigger numbers, more margin, more optionality.

Lean FIRE is “portfolio covers essentials.” It means FI is achieved earlier, but the budget and living expenses are tighter.

Coast FIRE is about timing. In Coast FIRE, you save hard early so compounding can do the rest while you keep working and FI later with a larger pot of assets than in Lean FIRE.

Lean FIRE is a baseline design. You make life cheaper, so the portfolio target is lower and achieved earlier.

Barista FIRE is a balance between active income and passive income. Barista FIRE combines partial portfolio sourced passive income and part-time employment income to achieve an optimized life balance and partial financial independence, often with the bonus of benefits and a safety net for sanity.

Lean FIRE can be pure “no work required,” but many people de-risk it by keeping a small income option, making it functionally Barista Lean FIRE in practice.

Expat FIRE is location leverage: reduce costs (sometimes dramatically) by building life in a country with a better cost-to-quality ratio.

Lean FIRE often becomes more livable—and less psychologically tight—when you add a location strategy.

If you want one sentence: Lean FIRE is the “smallest engine that still runs.” The other FIRE types are different ways to either build a bigger engine or reduce how hard the engine has to work.

Lean FIRE FAQ

- What is Lean FIRE?

Lean FIRE is a version of the FIRE approach that aims for financial independence on a deliberately “lean” annual spending level—usually by building a life where the basics are covered and the “good life” comes from what I call the free fundamentals (community, purpose, nature, movement), not constant paid consumption.

Mechanically, it’s still the same FIRE math: you’re saving and investing until your portfolio can cover your annual expenses using a safe withdrawal rate. The difference is the target lifestyle: Lean FIRE designs the expenses down, so the FI number becomes more achievable.

- What is Lean FIRE vs. Fat FIRE?

Lean FIRE and Fat FIRE are the same FI strategy with different FI goals and approaches to compromise in achieving them.

Lean FIRE is “essentials-first”: lower fixed costs with the compromises of fewer paid conveniences, less discretionary spending, tighter margin.

Fat FIRE is “high-discretionary” spending, allowing for more expensive housing options, more travel and convenience, more outsourcing, more buffer, with the compromise of more savings required to achieve the goal, along with more complexity (taxes, planning, and lifestyle expectations).

In other words, Lean FIRE buys time and simplicity. Fat FIRE buys comfort, flexibility, and margin. Neither is morally better. They just optimize for different lives.

- Is $2 million enough to retire at 40?

It can be, but it depends on your annual spending, your withdrawal rate, and your healthcare plan.

Here’s the clean translation:

At a 4% withdrawal rate:

$2,000,000 × 0.04 = $80,000/year

At 3.5%:

$2,000,000 × 0.035 = $70,000/year

At 3%:

$2,000,000 × 0.03 = $60,000/year

But retiring at 40 is a long runway, because with an average lifespan of 78.5 years in the US, the nest egg needs to last 38.5 years when the underpinning research of the Trinity Study tested for 30 years. That’s why many people choose to be more conservative (3–3.5%), or they keep a “pressure release valve” like Barista FIRE income for a few years – especially to deal with healthcare, market downturns, and the fact that real life is not a spreadsheet.

So: yes, $2M can be enough, under the right assumptions and withdrawal rate. The real question is: is your life a $60k/year life, an $80k/year life, or a $120k/year life? The number only makes sense in context.

- What are the rules of Lean FIRE?

Lean FIRE doesn’t have formal “rules,” but it has a handful of non-negotiables if you want the plan to be stable:

– Know your real annual spending (and don’t use a fantasy number).

– Build a lifestyle that’s livable on that spending (Lean FIRE fails when it becomes constant deprivation).

– Use a realistic withdrawal rate (4% is the classic shorthand; many Lean FIRE plans benefit from 3–3.5%).

– Treat healthcare as the hinge, not a footnote.

– Plan for bad years (sequence-of-returns risk + inflation + life surprises).

– Run annual check-ins so the plan evolves as your life evolves.

– Protect the free fundamentals so your life doesn’t become a low-cost pressure cooker.

The core “rule” is simple: Lean FIRE is a life design project aimed at creating a minimalist “structure” as a base, and maximizing personal fulfilment without additional cost. If life isn’t sustainable, the math doesn’t matter.

- How long will $500,000 last using the 4% rule?

Under the 4% rule, $500,000 supports about:

$20,000 per year ($500,000 × 0.04)

But the 4% rule is not a guarantee, and it’s not a countdown timer. It’s a rule-of-thumb based on historical market data for a roughly 30-year retirement based on the Trinity Study, assuming you stay invested and adjust withdrawals with inflation.

So the real answer is:

If your spending is ~$20k/year, $500k is in the Lean FIRE range and could last a long time if markets cooperate and you’ve planned for healthcare.

If your spending is higher than $20k/year, you’re either supplementing with income (Barista-style), lowering expenses, or using a more aggressive withdrawal plan (which increases risk).

A more conservative lens (especially for early retirement) is:

3.5% = $17,500/year

3% = $15,000/year

That’s the real “gut check” for Lean FIRE: can you live well at that spending level, with healthcare handled, and still sleep at night?

Sources

- Average annual consumer spending per person (U.S. BEA “Personal consumption expenditures per capita”), converted into today’s dollars using the CPI-U. (Source: https://fred.stlouisfed.org/data/A794RC0A052NBEA)

- Source: https://www.bls.gov/cpi/tables/historical-cpi-u-201710.pdf

- CPI-U annual averages for the 1970s come from BLS historical CPI tables. (Source: https://www.bls.gov/news.release/pdf/cpi.pdf)

Guides to Achieving Financial Independence

- How to achieve Financial Independence & Retire Early

- Barista FIRE Guide: Semi-Financial Independence

- Expat FIRE Guide: Living abroad with geoarbitrage to retire early

- Nomad FIRE Guide: Achieving financial independence by traveling around the world

- Coast FIRE

FIRE Calculators

- FIRE Calculator | How much do you need to retire early?

- Expat FIRE Calculator

- Nomad FIRE Calculator

- Lean FIRE Calculator

- Coast FIRE Calculator

- Barista FIRE Calculator

.

.

ABOUT THE AUTHOR

Carlos Grider launched A Brother Abroad in 2017 after a “one-year abroad” experiment turned into a long-term life strategy. After 65+ countries and a decade abroad, he now writes about FIRE, personal finance, geo-arbitrage, and the real-world logistics of living abroad—visas, costs, and tradeoffs—so readers can make smarter global moves with fewer surprises. Carlos is a former Big 4 management consultant and DoD cultural advisor with an MBA (UT Austin) and Boston University’s Certificate in Financial Planning. He’s the author of Digital Nomad Nation: Rise of the Borderless Generation and is currently writing The Sovereign Expat.