A guide to every variation of FIRE, how taking it abroad enhances the plan, and how to use each in sequence to achieve financial independence faster.

Disclaimer: This content is for educational and informational purposes only and is not individualized financial, tax, or legal advice. Examples and calculator outputs are hypothetical. Consider consulting a qualified professional before making financial decisions.

When most people discover the Financial Independence and Retire Early movement (FIRE) and its many approaches – Barista FIRE, Coast FIRE, Fat FIRE, Lean FIRE, Nomad Fire, and Expat FIRE – they treat it like a crowded menu at a great restaurant, assuming any dish (or approach) will satisfy. They pick one, aim for it, then put their head down, work, save, and hope to retire. At least this is how they visualize the journey to financial independence happening.

The people who actually achieve financial independence treat these variations of FIRE like gears in an engine. They select and shift between options to efficiently get through various stages of life: earning, wealth accumulation, and distribution. Financial independence is the destination for all of them.

I used four of these types of FIRE on my own journey to a financially independent life — Barista, Coast, Lean, then ExpatFIRE. But these weren’t four different paths. They were four stages within the same journey.

Most people reading this are somewhere on that same sequence right now. They just don’t realize it. And they don’t consciously know which stage they’re in, or what comes next. Understanding which FIRE approach you’re using now, and the best approach to apply next will empower you with FI sooner.

In this guide, I will help you understand each FIRE approach available, identify the best variation of FIRE for your point on your FIRE path, and get to financial independence faster. As a kicker, we will explain how to use geography as most powerful lever for achieving financial independence earlier.

Table of Contents

- The Types of FIRE and Why They Work Better Abroad

- Lean FIRE Abroad

- Coast FIRE Abroad

- Barista FIRE Abroad

- Nomad FIRE

- ExpatFIRE

- Chubby FIRE and Fat FIRE Abroad

The (Wrong) Question Most People Start With

Most people interested in retiring early starting by asking, “what is my FIRE number?”

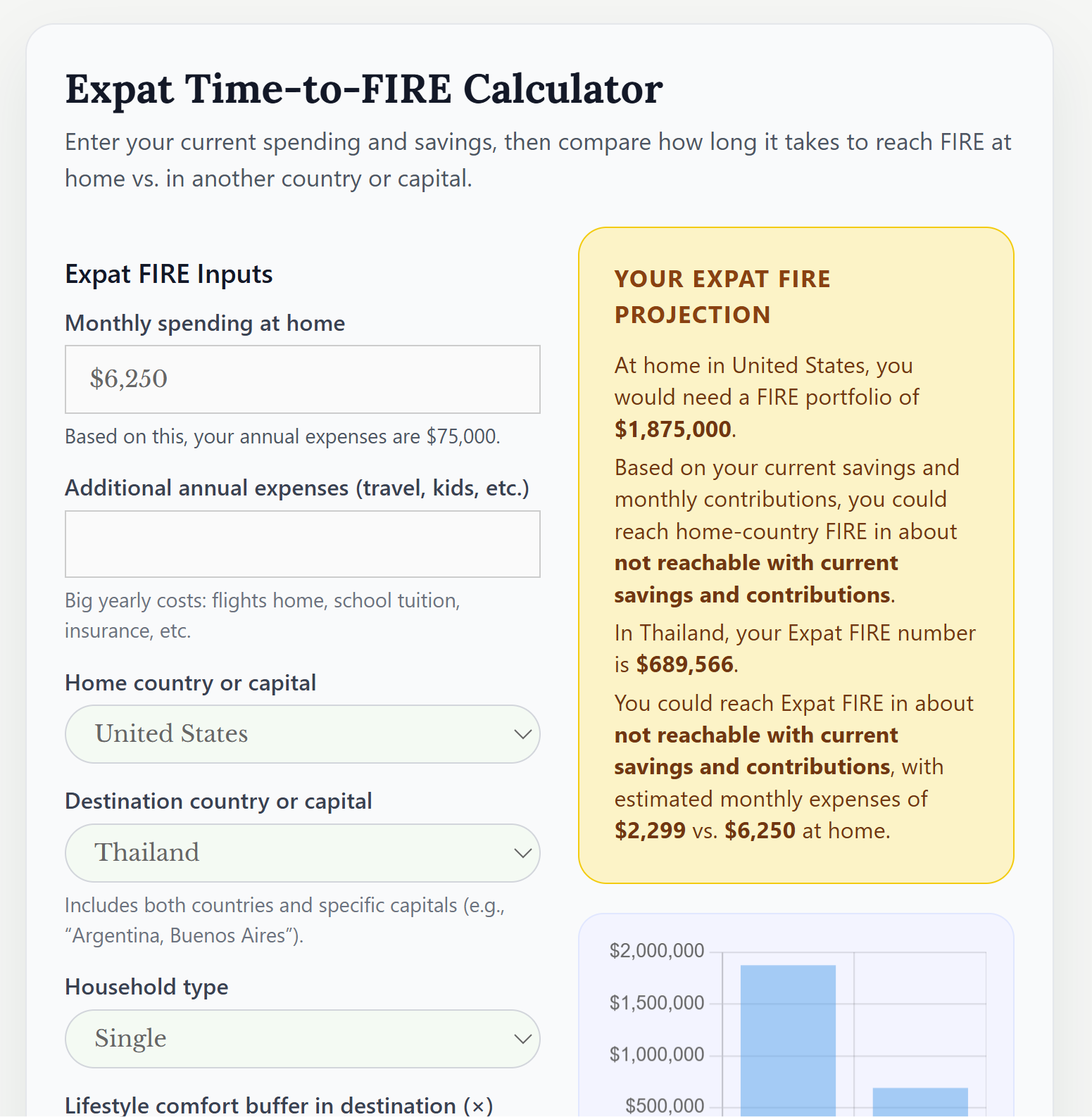

How much does the aspiring early retiree need in their portfolio to pay for their expenses indefinitely and potentially never work again? To calculate this price tag for financial freedom, take your annual expenses and multiply them by 25 to find your “FI number”. This is the amount of funds they need in a balanced portfolio to pay for recurring living expenses indefinitely at a 4% withdrawal rate. Then, they usually look at the gap between what they’ve saved and what you need, and feel either encouraged or crushed depending on how far along you are.

That FIRE number is real and useful. But most people make one mistake when they calculate it: they calculate it against a US cost of living they have no obligation to keep.

The median American spends roughly $78,500 per year on living expenses, according to the Bureau of Labor Statistics. That puts the standard FI number at about $1.96 million. For a household saving 15–20% of a median income, that’s a 30-to-40-year savings project. No wonder FIRE feels theoretical for most people.

Move abroad, and you restructure the math. A genuinely comfortable life in Chiang Mai, Medellín, or the quiet interior of Portugal costs $20,000–$35,000 per year. The FI number on that life is $500,000–$875,000 — a target that’s reachable in 10 to 15 years for many earners, and in many might have already crossed that financial independence finish line without realizing it, if they are willing to take on the adventure of moving abroad.

The question isn’t just which type of FIRE — it’s which type of FIRE, run against which cost of living, at which stage of your savings journey, and where in the world you seek financial independence.

How to Find the Right FIRE Approach for You: Find Yourself First

Before walking through the individual approaches to FIRE, find clear answers to two questions:

1. How much do you need per year to live the life you want, at home and abroad? What are your actual expenses, in your home country? Have you run that number against the cost of living abroad in a geoarbitrage friendly country?

2. How close is your current portfolio to covering both numbers – your home country number and your cost of living in another country – indefinitely at a 4% withdrawal rate?

Those two answers are the first direction markers that point to which FIRE approach is best for you right now, and which one you’re building toward.

Portfolio not yet at FI number | Portfolio at or near FI number | |

|---|---|---|

$20K–$30K/yr spend | Lean FIRE (building) | Lean FIRE (achieved), Expat FIRE (achieved) |

$30K–$50K/yr spend | Coast → Barista FIRE abroad, building | Nomad FIRE / ExpatFIRE |

$50K–$80K/yr spend | Barista FIRE abroad + Coast FIRE | ExpatFIRE / Chubby FIRE abroad |

$80K+/yr spend | Coast FIRE + high-density income phase | Chubby FIRE / Fat FIRE abroad |

One note on reading this table: these spending levels applied abroad (in the Expat FIRE and Nomad FIRE cases) are not for a stripped-down existence. This spending covers a quality apartment, good food, leisure travel, and a functioning daily life in dozens of cities that most Americans would consider exceptional. Taking an achieved FIRE portfolio abroad to the right country generally doubles to triples the buying power and luxuriousness of your early retirement, relative to life in the US, Canada, and norther Europe.

We will cover each approach to FIRE to find the best approach to you, but the subtle nudge to encourage you to consider a (financially independent) life abroad is specifically for the underappreciated timeline acceleration and increased comfort on the same portfolio.

For now, find your row, make note, and read the section that matches where you are right now, and the one that matches where you’re going.

The Types of FIRE

Lean FIRE Abroad

What it is

Lean FIRE is financial independence on a deliberately minimal annual spend. Developing the discipline to live on a small budget, and low annual expenses, translates to a much smaller portfolio and total assets needed to be financially independent. The portfolio is just large enough to sustain that spend indefinitely. No extras, no buffer for lifestyle upgrades — the budget is lean by design, not by accident.

In the US, living lean means roughly $25,000–$40,000/year ($2,000 to $3,500 per month) — a lifestyle that requires serious intention and geographic flexibility to make comfortable, generally eliminating the Pacific Coast and large desirable cities. While Lean FIRE theoretically sounds like a great tradeoff, frugality in exchange for financial freedom, most American cities make Lean FIRE feel like deprivation.

However, Abroad, the same annual “lean” spend buys something different entirely. Anyone considering targeting Lean FIRE should also consider Expat FIRE, as the ultimate payoff will be much higher in comfort, quality of life, and sustainability.

What Lean FIRE looks like abroad

$1,500–$2,000 per month in Chiang Mai, Da Nang, Medellín, or the interior of Portugal isn’t austerity. The average income in €1,741 ($1,985) per month. The average nomad’s cost of living in Chiang Mai is $1200. The average monthly rent for a serviced apartment walking distance from Da Nang’s beaches is $650.

Lean FIRE taken abroad translates to luxurious. It’s a furnished apartment in a walkable neighborhood, meals out most nights, a gym or yoga studio, day trips on weekends, and reliable fast internet. These possibilities are the baseline of a good daily life, not the ceiling.

The numbers:

- Typical Lean FIRE monthly budget abroad: $1,500–$2,000 (after transitioning and settling)

- Annual spend: $18,000–$24,000 (in Southeast Asia, selectively in South America, and rural southern Europe)

- FI number at 4% withdrawal: $450,000–$600,000 assets needed

- US comparison: $600,000 in the US funds roughly $24,000/year — genuinely tight, genuinely stressful, virtually impossible

A kicker: For FIRE types withdrawing stocks to pay for life, you may be able to take your withdrawals tax free due to 0% long term capital gains taxes.

The key point: the Lean FIRE number is achievable on a timeline that feels real, and taken abroad it creates a living situation that is realistic. A 30-year-old earning a median US salary and saving aggressively can hit $500,000 by their late 30s or early 40s, and transition into a fantasy life in Central America, on the South America Pacific, or on overlooked islands in the Indian Ocean.

Who it’s for

Lean FIRE abroad is right for readers who value simplicity and mobility over comfort upgrades, who are willing to make the move, and who are already near a modest FI number ($350,000 to $600,000). It’s also the right entry point for people who want to start the life now and let the portfolio grow from there, taking a partial Coast FIRE approach within their Lean FIRE escape.

However, the life abroad portion is not right for anyone who needs community roots they can’t rebuild, close proximity to aging family they’re not willing to be far from, or anyone uncomfortable with the lean life leading up to lean FIRE or a lifestyle that doesn’t fit inside a $2,500/month ceiling anywhere in the world.

The honest test for Lean FIRE Abroad: spend 30–90 days actually living on a Lean FIRE budget in your target city before you commit the portfolio to it. It works for some people and not others, and the answer is personal.

Where it leads

Lean FIRE abroad isn’t always permanent. Many people use it as a launch pad — starting with a Lean FIRE budget abroad to simply live a period without working, in sabbatical and travel mode. As they settle into life and crave a return to purpose (or a cash increase) more than a recharge, they may take a remote job or build a remote business for temporary cash flow (Barista FIRE), and meanwhile withdraw less and let the portfolio compound at low withdrawal rates (Coast FIRE), and gradually let the numbers in their portfolio grow so that their lifestyle can expand with it later.

Others fully comfortable with the life may stay lean by choice and find the simplicity exactly what they wanted. Both are valid. The difference is whether lean is a constraint or a preference.

Lean FIRE Resources to Start with:

→ Lean FIRE Guide | Lean FIRE Calculator | Cheapest Cities in the World

Coast FIRE Abroad: Taking the foot off the gas and letting your assets work, and grow, for you

The insight most people miss: Left alone to compound, the right sum of money can grow into the perfect sum of money, no further effort required.

Coast FIRE is an approach to save enough that if you stop contributing today your portfolio will compound passively to your full FI number by a target retirement age without another dollar added. You save enough early and the accumulation phase is done. You just need to cover living expenses until the portfolio catches up.

The implication that most Coast FIRE readers never run: if your Coast FIRE number is already hit in the US, your full FIRE number may already be hit abroad.

The math, worked through

Say you need $75,000 per year to retire comfortably in the US. Your FI number is $1,875,000. You’ve saved $750,000. In the US, you’re not there — you still have a $1,125,000 gap.

Now run the abroad version.

In Thailand, the cost of living, on average, is only 37% of the cost of living in the US.

If you move to Thailand, your equivalent lifestyle costs $27,750 per year, your FI number becomes $693,750. You’ve already crossed it.

This isn’t creative accounting. It’s the same math, run against an honest cost of living, in allocation with better economics.

How does this “life abroad” math relate to a Coast FIRE strategy?

While you could Coast FIRE in the US by continuing to work while no longer saving, and letting that $750,000 double every years due to compound interest (achieving $1.5 million in 7 years and ~$3 million in 14 years), all while enjoying spending your entire paycheck each week…you could just leave now!

Taking Coast FIRE abroad, allocating a portion of your portfolio to take withdrawals from ($600k for $2000 a month, in Bangkok, Japan, Malaysia, or El Salvador), and allowing the rest ($150k) to double on its own every seven years, you can “coast” your way into a better retirement, all while not working at all. After 15 years in retirement, that $750k would become $1,350,000, opening up new options as you age.

Coast FIRE abroad isn’t just “coast a little longer while living cheaper.” For a meaningful slice of readers who have been saving seriously for 5–15 years, it’s the realization that the gap they thought they had doesn’t exist anymore — once they remove the geography assumption baked into the original calculation.

The numbers:

- Typical Coast FIRE monthly budget abroad: $2,000–$4,000 (mid-range, quality lifestyle)

- Annual spend: $24,000–$48,000

- FI number range: $600,000–$1,200,000

- US equivalent lifestyle: $4,000–$8,000/month, FI number $1,200,000–$2,400,000

Who it’s for

Coast FIRE abroad is right for readers who have been saving for years and suspect they may be closer to financial independence than their US-denominated FI number suggests. Run the numbers before you assume. The Coast FIRE Calculator will show you your Coast FIRE number; the ExpatFIRE Calculator will show you what that number means abroad.

The key action

Run your FI number twice: once against your current US cost of living, once against a realistic abroad budget. The gap between those two outputs is the financial value of moving. Do this before deciding you need more time.

Where it leads

Coast FIRE abroad typically converts to ExpatFIRE faster than expected – likely immediately. A low withdrawal rate combined with any part-time or passive income can close the remaining gap between your portfolio now and your FIRE number within a few years. The portfolio does the heavy lifting; the geography keeps the withdrawal rate low enough to let it.

→ Coast FIRE Guide | Coast FIRE Calculator | ExpatFIRE Calculator

Barista FIRE Abroad

FIRE Abroad subsidized by a digital nomad life

Barista FIRE is semi-retirement: the portfolio covers most expenses, and part-time or freelance income covers the rest. The original concept was simple — leave a high-stress career, take a low-stress job for the benefits and the income gap, and let the portfolio compound. Abroad, the concept upgrades significantly.

The “barista job” becomes a few hours of remote consulting, a small online business, freelance writing or design, online tutoring, or any income source that travels well. Essentially, part time retirement, part time digital nomad, full time existing anywhere you please. The income requirement is modest. The lifestyle is full.

This list of the most popular jobs among successful digital nomads and remote workers abroad is a great place to ideate options. Over 400 digital nomads shared how they earn money remotely in our Global Digital Nomad Study, and the insights they shared might pave the way to your Barista FIRE life abroad. My book, Digital Nomad Nation painted very clearly that a new trail is being blazed here that makes FIRE abroad even more flexible.

The visa alignment no other FIRE type has

This is where Barista FIRE abroad becomes uniquely powerful: the income structure, proof of earned income that is location independent, maps directly onto the digital nomad visa ecosystem, and makes a life abroad more sustainable and more possible comfortably.

Dozens of countries now issue DNVs or equivalent long-stay permits built for exactly this profile — remote income earners who want to live legally in a country for 6–24+ months. The income thresholds for most of these visas sit precisely in the range that Barista FIRE generates:

- Costa Rica Digital Nomad Visa: ~$2,500/month income

- Portugal Digital Nomad Visa: ~$3,480/month

- Thailand Long-Term Resident Visa (remote worker): ~$2,666/month

- Colombia Digital Nomad Visa: ~$800/month

This approach, with a digital nomad visa, is the easiest way to get around the normal 90 days out 180 day stay limitation in Europe’s Schengen zone and many other countries. Italy’s Digital Nomad Visa, Portugal’s D8 Visa, and Spain’s Teleworker visa are the backdoor options for any nationality to stay in Europe indefinitely. The same exists in the top destinations in Asia and Latin America for those who can prove remote income.

You’re not working full-time. You’re generating enough part-time income to qualify for a legal long-stay visa in a country where your portfolio goes untouched and your cost of living is a fraction of home. You’re selectively choosing work that improves the quality of your life and that you find engaging. The visa and the FIRE strategy not only solve but enhance each other.

The numbers:

- Typical Barista FIRE monthly budget abroad: $2,000–$3,500 (total)

- Part-time income needed: $1,000–$2,500/month (covering the gap above portfolio withdrawal and qualifying for digital nomad visas and residencies)

- Portfolio needed: $300,000–$800,000 depending on the income-to-expenses gap and target countries

- US comparison: same semi-retirement in the US typically requires $1M+ portfolio to generate comfort with part-time income covering healthcare

Who it’s for

Barista FIRE abroad is the sweet spot for readers who have a partial portfolio — not quite at full FI, but close — and a remote-compatible skill. The ideal profile: someone who enjoys some work on their own terms (creative, consulting, writing, design, teaching, coaching), has a portfolio in the $400,000–$800,000 range, and is willing to move.

This is also the most forgiving entry point into FIRE abroad. You don’t need to have the full number. You need enough portfolio to take the pressure off, and enough income to keep the math comfortable while the portfolio grows.

Where it leads

Barista FIRE is the most common bridge to ExpatFIRE. In my ~10 years abroad, I’ve met many friends that started living abroad as a digital nomad, lived in a low cost country and saved, and now lived fluidly around the world as financially independent expats that work remotely for purpose. In Barista FIRE abroad, income keeps flowing, portfolio keeps growing, expenses stay low, and the full FI number gets closer every year. Most people who have achieved ExpatFIRE passed through this Barista FIRE phase, whether they called it that or not.

Best Resources on Barista FIRE Abroad:

Barista FIRE Guide | Barista FIRE Calculator | 53 Best Digital Nomad Visas | Where can I live on $3,000/month?

Nomad FIRE

The distinction that matters

Nomad FIRE is not a different financial structure than ExpatFIRE or Lean FIRE. It’s a different lifestyle choice layered on top of one of those structures. You’re financially independent — or close enough — but you choose to keep moving rather than settling a base.

Perhaps you’ve always wanted to travel the world, and your round the world backpacking trip just so happens to be financially independent.

Perhaps you want to Expat FIRE but you’ve spent so little time abroad its too soon to settle – and 2 months on each continent is the perfect solution?

The distinction: Nomad FIRE is about mobility as a priority, not a budget strategy. You could afford to settle. You choose not to.

This framing matters because most descriptions of Nomad FIRE treat constant movement as a financial necessity — as if you’re moving from city to city to hunt cheap rent. That’s not Nomad FIRE. That’s budget travel. Additionally travel and constant movement will always be more expensive than settling in one spot, making Expat FIRE the cheaper choice and Nomad FIRE the more adventurous choice. Nomad FIRE is the deliberate choice to design a life around mobility and travel once the financial foundation is already in place, and the logistical differences matter more than the financial logisitics.

What Nomad FIRE actually requires

Sustained mobility is more expensive than most people plan for. Moving constantly adds a “mobility premium” — flights between bases, higher short-term rents, the cost of not having the negotiating power a long-term lease gives you, and the logistics overhead of managing a life without a permanent address.

The numbers:

- Typical Nomad FIRE monthly budget: $2,500–$4,000 (varies significantly by region — Southeast Asia is cheaper, Europe and Japan are not)

- Mobility premium vs. settled expat life: roughly 10–20% higher baseline cost at best, but can be 30% to 50% higher depending on spending and planning discipline

- FI number: $750,000–$1,200,000

- Visa structure required: rotating DNVs, tourist allowances, visa runs, or a stack of short-stay legal options across multiple countries

What the logistics actually look like:

- Remote banking that doesn’t flag foreign transactions or close accounts for inactivity

- Travel health insurance that covers multiple countries year-round

- Mail, domicile, and US tax residency sorted — these bite people who don’t sort them before they leave

- A rolling calendar of visa expirations and entry requirements, and maintaining the documentation and residency awareness to apply for them.

Where it leads

Most Nomad FIRE followers eventually settle — into ExpatFIRE or Chubby FIRE abroad — as the appeal of constant movement softens. My research found that most nomads settle into a single place or base after two years of travel. That’s not failure; it’s the natural evolution. Nomad FIRE is often the best phase between “I’ve hit my number” and “I’ve found my place.” Use it to find that place.

The honest caveat: Nomad FIRE works well until visa stacking becomes legally complicated or healthcare needs become serious. Have a residency option in your back pocket before you need one.

→ Nomad FIRE Guide | Nomad FIRE Calculator | Best Cities for Digital Nomads | Digital Nomad Visas

If you find the prospect of the modern nomad lifestyle interesting, be sure to read my book Digital Nomad Nation.

ExpatFIRE

The destination most wanderlusting FIRE followers are building toward

ExpatFIRE is full financial independence with a permanent or semi-permanent base abroad. This is the club I joined recently, love, and recommend to anyone who thinks “I could live here” every time they travel to a quite European countryside village, a tropical island, or a buzzing Latin American center. Not constantly moving. Not scraping by on Lean FIRE minimums. Not working part-time to cover gaps. The portfolio covers the expenses. The base is chosen for quality of life, not just cost reduction. The lifestyle is designed intentionally, not defaulted into.

The numbers:

- Typical ExpatFIRE monthly budget: $2,500–$5,000 (a designed life with room for travel, food, and quality)

- Annual spend: $30,000–$60,000

- FI number: $750,000–$1,500,000

- US equivalent lifestyle: $60,000–$120,000/year, FI number $1,500,000–$3,000,000

That gap — between a $750,000 ExpatFIRE number and a $3,000,000 Fat FIRE number in the US for a comparable lifestyle — is the value of the decision in one line.

What the structural requirements look like

- Long-term visa or permanent residency (retirement/pensioner visas, rentista or rentier programs, or residency by investment)

- International health insurance that isn’t dependent on your passport country

- Banking and tax structure understood and managed — especially for US citizens, whose worldwide income tax obligations don’t disappear at the border

- At least one base selected for a multi-year minimum, not just current affordability

Who it’s for

ExpatFIRE is for those who want a settled life — community, rhythm, roots — but abroad, in other climates and cultures surrounded by other languages and cuisines, within a continuing experience that they can grow into. Not the perpetual mover. Not the minimalist. The person who wants a full life, deliberately designed, outside the US cost structure and culture.

→ ExpatFIRE Guide | ExpatFIRE Calculator | From $8,000 to ExpatFIRE | Moving to Country Guides

Chubby FIRE and Fat FIRE Abroad

Fat FIRE is full financial independence with no lifestyle compromise — $80,000–$150,000+ per year in withdrawals, funded by a portfolio typically over $2,000,000. Chubby FIRE is the comfortable middle ground: financially independent with an above-average lifestyle, roughly $60,000–$100,000 per year, a $1,500,000–$2,500,000 portfolio.

In the US, achieving Fat FIRE is a $3,000,000–$5,000,000 project. Most people treat that number as the ceiling and either grind toward it for decades or quietly give up on the idea.

Chubby FIRE and Fat FIRE are unique, within the context that they create abroad, because the potential of a retirement with this ample a portfolio is commonly overlooked for Americans – which is a travesty. $80,000 to $150,000 could buy a comfortable retirement in the US, so most people that achieve it don’t consider the need to go abroad – that’s supposedly for the expats like me trying to stretch their money further, right? Wrong.

Chubby FIRE and Fat FIRE abroad still buy an inordinate increase in quality of life.

For example, Switzerland is on average 30% more expensive than the average cost of living in the US. However, Switzerland could barely be compared to the average US city. The closest comparable would be taking a clean version of San Francisco and New York combined, and dropping it into Colorado somewhere near the ski slopes and scattering a defining café culture (that birthed Starbucks) in between. Virtually any location you choose will be safe with a high quality of life and easily accessible nature and enjoy public transportation that is extremely difficult to find in the US these days.

In other words, Chubby FIRE and Fat FIRE level independence taken abroad unlock the keys to day to day living and backdrop combinations that are virtually non existent in the US, and allows you to curate a an unreal lifestyle.

Singapore. Switzerland. Tokyo. Milan. Berlin. Northern summers in Sweden and winter summers in Melbourne and Sydney. Springs in New Zealand and on the Cherry Blossom Trail during Golden Week.

Singapore is one of the safest city states in the world, and it is easily accessible from nearly anywhere in the world. Switzerland offers one of the highest qualities of life with peace and nature at your doorstep in a way that is impossible to find in the US. Nordic summers are amazing, and everything between Melbourne and Sydney has a vibrance of western culture against eastern backdrops with 1970s US era freedom and flow that you won’t find many places . And this level of affluence, independent of location opens up countless other livable locations and experiences – from New Zealand to Monaco, from chasing F1 events to following your favorite artists around the world.

Not just to jet set, but to live in if you choose to.

While aiming for Chubby FIRE or Fat FIRE in the US is a goal worth achieving, it is a more powerful goal abroad. While the other approaches to FIRE give a more for less in terms of luxury and comfort, but essentially different levels of the same, Chubby FIRE abroad opens new doors.

Chubby FIRE and Fat FIRE viewed through a global lens unlock a lifestyle that most dismiss as only possible for jet setting billionaires. But, it is possible, very possible, on the portfolio that the average upper middle class American will retire with…if they are willing to change their country code.

The numbers:

- Chubby FIRE abroad: $4,000–$7,000/month, FI number $1,200,000–$2,100,000

- Fat FIRE abroad: $7,000–$12,000/month, FI number $2,100,000–$3,600,000

- US equivalent Chubby FIRE: $8,000–$15,000/month, FI number $2,400,000–$4,500,000

- US equivalent Fat FIRE: $15,000–$25,000+/month, FI number $4,500,000–$7,500,000+

Who it’s for

Higher earners who aren’t willing to compromise on lifestyle but are willing to relocate to get better value. Senior professionals, successful business owners, anyone who has looked at their Fat FIRE number in the US and wondered if there’s a more efficient path.

There is.

For Chubby and Fat FIRE readers who want to go further than cost reduction — into tax efficiency, long-term residency planning, and structuring a sovereign financial life — that’s a deeper conversation than this article covers. It’s the Sovereign Expat framework, and it warrants its own guide.

→ Chubby FIRE Guide | Fat FIRE Guide | ExpatFIRE Calculator

The FIRE Sequence: How These Types Work Together

Nobody stays in one gear forever. The people who reach ExpatFIRE fastest don’t arrive there in a single move — they shift through several types as the portfolio grows, life circumstances evolve, and geography changes. The phase you’re in right now isn’t your permanent address. It’s your current position on the journey.

Here are four realistic paths. Find the one that most closely matches where you’re starting from.

Path 1: The Coast-to-Expat Track

For the early-career saver with a marketable remote skill

Aggressive saving in the US for five to eight years hits the Coast FIRE number. Rather than grinding toward the full FI number from a US cost base, make the move abroad on a Digital Nomad Visa to your country of choice – I highly recommend considering El Salvador, Portugal, Spain, Italy, Croatia, Brazil, Japan, Indonesia (outside of Bali), Malaysia, and Thailand.

Barista FIRE in a low cost historical town center, a bohemian beach village, or cottage in a mountain village — part-time remote income covers expenses, portfolio compounds untouched for two to four years. The full ExpatFIRE threshold arrives faster than it would have in the US, where every additional year of saving is fighting against a high-cost baseline that’s constantly increasing.

This is the fast track for people in their late 20s to mid-30s who have a remote-compatible income and are willing to make the move before conventional wisdom says they’re “ready.”

Path 2: The Lean Launch

For those close to a modest number and ready to move now

If your current portfolio sits at $500,000–$650,000 in the US, that is not enough. Abroad, that is Lean FIRE already funded. Start by moving to a quality low-cost base — Chiang Mai, Da Nang, Medellín, the Alentejo in Portugal. Live lean, keep withdrawals low, and leave enough breathing room in your withdrawals to let the portfolio grow with minimal draws. Along the way, master the art of integrating into your country, as learning the language, culture, your neighborhood, and the nuances of life will continue to bring costs down throughout your first two years in your new home.

Ideally, maintain an optional income stream if it fits (a few consulting hours a month, some freelance work) to keep your withdrawal rate even lower. As quality of life and lifestyle preferences settle, the life evolves naturally from Lean FIRE toward ExpatFIRE and the portfolio grows past the number.

This is the path if you are done waiting and willing to start living the life in a leaner, more flexible fashion, while the numbers close the remaining gap passively.

Path 3: The Barista Bridge – FIRE Abroad combined with Digital Nomadism

For the reader with a portable income stream and a partial portfolio

Portfolio is at $400,000–$750,000. Not at the FI number, but close enough that a modest remote income covers the gap. Move abroad on a DNV. Low expenses mean the portfolio goes untouched — or close to it — for two to four years, keeping in mind that a well diversified portfolio will double in seven years if left untouched. The income gradually scales down as the portfolio scales up. ExpatFIRE is achieved without a hard stop — the transition is gradual, the finish line moves closer every year, and the life abroad is already the life you wanted, and it is steadily improving as your nest egg grows.

This is the path I took. Barista FIRE, then Coast, then Lean, then ExpatFIRE — not as separate goals, but as the same engine in different gears. Most of the readers who eventually reach ExpatFIRE do something close to this, whether they name it that way or not.

Path 4: The Chubby Direct Approach

For the higher earner who’s closer to their number than they think

High-income professional with $2,000,000 to $3,000,000 saved. In the US, you are not yet at Fat FIRE. Abroad, are already at Chubby FIRE — comfortably, with full quality of life intact. Move directly to a premium expat base and enjoy full financial independence from day one, at a lifestyle that would cost $4,000,000+ to replicate domestically. No Lean phase, no Barista phase, no waiting.

This is the path for readers who don’t need to optimize for speed — they need to realize they’re already there, once they update the geography assumption in the calculation.

The point these four paths share

Different starting points, different gear shifts, same destination. The readers who get there fastest are not the ones who found the perfect FIRE type before moving. They’re the ones who identified their current position, moved on a type that fit it, and adjusted as the journey developed. FIRE abroad is not a plan you execute. It’s a path you navigate.

Which Type Is Right for You: The Decision Framework

Two questions. Answer them in order.

Question 1: What is your real annual spend abroad?

Not your US spend. Not a rough estimate. The actual number for the life you want to live, in a real destination you’re genuinely considering.

If you haven’t run this number yet, do it before reading further. Use the ExpatFIRE Calculator and the FIRE Calculator side by side — one for your current US baseline, one for your target abroad scenario. The gap between the two outputs is the value of the decision you’re evaluating.

Question 2: Where is your current portfolio relative to your abroad FI number?

Three positions:

(A) Less than 60% of the way to your abroad FI number (B) 60–90% of the way there (C) At or past your abroad FI number

Now match your position to your type:

Under 60% + spend of $1,500–$2,500/month abroad: → Lean FIRE abroad now. You’re closer than you think. The portfolio grows faster at a low withdrawal rate than it does sitting in a US savings account while you grind toward a US FI number. Move, lean out, let the math work.

Under 60% + spend of $2,500–$4,000/month + remote income: → Barista FIRE abroad on a DNV. Income covers expenses, portfolio grows untouched. This is the Barista Bridge. Two to four years of this and the full FI number is typically in reach.

60–90% of the way there + any spend level: → Run the Coast FIRE calculation against your abroad number before you do anything else. You may have already crossed your full FI threshold once the geography assumption changes. The Coast FIRE Calculator will tell you in five minutes whether you still have a gap or whether the gap is already closed.

At or past your FI number + spend of $2,500–$5,000/month: → ExpatFIRE. This is not a future goal. Pick a base, research the residency path, and start planning the move. The life is already funded.

At or past your FI number + spend of $5,000+/month: → Chubby or Fat FIRE abroad. Run the abroad version of your Fat FIRE number. It is almost certainly lower than the US number you’ve been targeting — meaningfully lower. Do the math before spending another year optimizing toward the wrong number.

Any of the above + preference for mobility over roots: → Nomad FIRE, built on whichever financial structure applies above. Keep the visa strategy in mind from the start, and have a residency fallback lined up before you need it.

These categories are not rigid, and the life is not a spreadsheet. The readers who reach financial independence fastest are not the ones who picked the perfect type and executed it without deviation. They’re the ones who started — picked the closest type for where they were, moved on it, and adjusted as the numbers and the life evolved.

Geography is a lever. Pull it as soon as the math makes sense for your position. Don’t wait for certainty. Certainty is what you build by living the thing, not by planning it from a desk in a city that’s making the numbers harder.

Start Here

- → Calculate your ExpatFIRE number

- → Calculate your Coast FIRE number

- → FIRE Abroad: How Moving Overseas Can Cut Your FIRE Number in Half

- → Where can you live on your current budget?

- → The FIRE Starter Kit: Build your number, then stress-test it for 50 years

- → 53 Best Digital Nomad Visas

- → From $8,000 to ExpatFIRE: How I achieved financial independence through a life abroad

.

.

ABOUT THE AUTHOR

Carlos Grider launched A Brother Abroad in 2017 after a “one-year abroad” experiment turned into a long-term life strategy. After 65+ countries and a decade abroad, he now writes about FIRE, personal finance, geo-arbitrage, and the real-world logistics of living abroad—visas, costs, and tradeoffs—so readers can make smarter global moves with fewer surprises. Carlos is a former Big 4 management consultant and DoD cultural advisor with an MBA (UT Austin) and Boston University’s Certificate in Financial Planning. He’s the author of Digital Nomad Nation: Rise of the Borderless Generation and is currently writing The Sovereign Expat.