Most people love the idea of financial independence and retiring early, but these possibilities can seem remote on the standard path of saving and investing 10% of one’s paycheck. At the same time, though the FIRE movement offers proven approaches for early financial independence, it often comes with hefty sacrifice, and few people want to spend their entire, already uncomfortable working career, in increased frugality and austerity. Luckily, there is a middle ground approach that makes retiring early possible, while still living a normal, comfortable life – Coast FIRE.

The “Coast FIRE” approach to financial independence uses an intentional one-time burst sacrifice of savings to make a single lump sum investment early in life to achieve a later target FIRE number via compound returns. By investing early, significantly, and properly, then letting time and “compounding growth” do the rest, Coast FIRE followers can live and work in a normal life, while simply “coasting” to their planned early retirement date, without the stress or worrying about saving for longer.

In this complete guide to Coast FIRE, we’ll explain how this flexible approach to FI combines the prudence of traditional retirement planning and the smart financial moves of the FIRE movement to give you the early financial independence you want, when you want it, how you want it.

Read on for a complete guide to Coast FIRE.

Disclaimer: This content is for educational and informational purposes only and is not individualized financial, tax, or legal advice. I don’t know your personal situation, and reading this does not create an advisor-client relationship. Consider consulting a qualified professional before making financial decisions, and invest based on your goals, time horizon, and risk tolerance.

Assumptions Notice: Examples and calculator outputs are hypothetical, based on user inputs and assumptions (e.g., returns, inflation), and actual results will vary.

Stop guessing. Stress test your plan for 50 years.

Build your FIRE number, then pressure test withdrawals across inflation and ugly sequences.

- PASS/FAIL + ruin year

- Inflation plus real return sequences

- One-time expense shocks

Includes the FIRE Number Builder, 50-year Stress Test, and the IPS rulebook.

COAST FIRE AT A GLANCE

Coast FIRE, in one sentence:

Coast FIRE is the point where you’ve invested enough that you can stop saving aggressively, because your portfolio can grow into your full FIRE number by your target retirement age.

One equation:

Coast FIRE Number = (Annual retirement expenses × 25) ÷ (1 + r) ^ years until retirement

(You can swap 25 for 29–33 if you want a more conservative withdrawal rate.)

One example:

If you want $60,000/year in retirement, your future FIRE number is about $1.5M (60k × 25).

If retirement is 25 years away and you assume 7% growth, your Coast number is about $276k today (1.5M ÷ 1.07^25).

Use the calculator:

Our Coast FIRE Calculator lets you quickly explore your Coast FIRE options

A simple Coast FIRE roadmap:

- Pick your target retirement age (how many “coasting” years you have).

- Estimate retirement expenses (and don’t ignore inflation).

- Convert that into a future FIRE number (25x, or more conservative).

- Discount it back to today to get your Coast FIRE number.

- Build a “burst savings” plan to hit that number early (career + expense setup).

- Invest, then run a yearly check-in (returns, inflation, life changes, plan-B levers like Barista/Expat).

Table of Contents

What is Coast FIRE

Coast FIRE is the financial independence approach achieved by saving and investing a large sum of money early in life, and allowing compound returns to grow that sum to a target future FIRE number at a specific date in the future while allowing the investor to “coast” along the way without additional savings or investment.

This approach allows people who prefer it to concentrate their hard work, sacrifice, and savings required to achieve financial independence into a shorter period of time. In doing this, they better leverage the power of compounding returns and time than the average FIRE follower or saver for retirement, who generally spreads their savings and investing equally over their entire “accumulation phase,” right up to retirement. Additionally, Coast FIRE allows a person, during their working years, to live a more normal life with a lighter financial load and without the burden of continued saving or the stress of worrying about retirement.

While other FIRE avenues emphasize continuous, slow-burning approaches to saving, investing, and long-term frugality, Coast FIRE types take a proactive, early completion approach, through burst sacrifice and savings efforts, underpinned by good math and aided by time.

Who is Coast FIRE best for

Given Coast FIRE is more effective the earlier it is started, and when that initial savings and investment is larger, Coast FIRE is best suited for the following people and personality types.

- The young (18 to 30) are taking advantage of unusually high-paying jobs or a time of few financial responsibilities.

- Those who appreciate the value of delayed gratification

- University students taking a work gap year and open to leveraging the flexibility inherent to youth to be more frugal and save more

- Situations with reasonably high pay with expenses covered, or in low-cost-of-living areas, wherein an unusually large amount can be saved

- Those who don’t necessarily want to retire early, and find reasonable satisfaction in their careers today, but want to achieve FI in a reasonable time, for the optionality

Setting the Stage: An early start, lump sum effort, and time are the keys to Coast FIRE

We’ve already reviewed that Coast FIRE leverages the power of hard work early (savings), simple yet smart investing, and time to make future millionaires, while living a normal life. Now, let’s review some numbers on the potential gains in Coast FIRE that support this.

Examples of Coast FIRE and the power of starting early:

Assuming an aggressive portfolio, roughly matching the stock market, and achieving the same historical stock market returns of 10%…

- $15,000 invested at 18 years old will become $1,000,000 at 62. This means one summer of hard work, hustling, and saving before university can make a millionaire with no additional savings.

- $20,000 invested at 21 years old will become $1,000,000 at 62. So, two to three summers of internship savings could be all it takes to make a million dollars.

- $48,000 invested by 30 years old will become $1,000,000 by 62. Strategic, conscious savings of $16k per year from age 27 to 29 could be all it takes to make a millionaire.

The examples above prove the power of time & compounding interest underpin the Coast FIRE approach.

Massive, strategic savings and investment action early are what make these principles real in your FI plan and make the seemingly impossible (financial independence or early retirement) very possible.

Warren Buffett bought his first stock at 11 years old. By 21, he had saved $21,000. That practice of saving and investing early grew the habits, and arguably the acumen, early that drove him to billionaire status today. Additionally, Warren Buffett’s own approach of “value investing” mirrors Coast FIRE’s approach of buying common sense, smart investments, then holding them with no unnecessary trading, letting time and the markets do the rest on the way to wealth.

Starting early is the single biggest principle you could learn from Buffett’s success, and that is exactly what underpins Coast FIRE.

How Coast FIRE Works

Step 1: Before your “Coast FIRE date”: The Build & Accumulation Phase

First, you make sure you actually understand the basics of FIRE, the personal finance principles behind it, and what Coast FIRE requires in terms of commitments and sacrifice so you can confirm whether Coast FIRE (or another type of FIRE**) is the right path for you.

Then you pick your timeline, number of years of “Coasting,” and full FIRE date. Coast FIRE starts with a date because your timeline determines how much compounding runway you have. Decide when you’d like to retire (how many years from now), and estimate what your annual expenses will be in retirement. Remember to account for not just your current annual expenses, but the lifestyle you’ll likely be living then, your health and relationship requirements, with inflation and reality accounted for.

From there, calculate your future FIRE number. Ensure to think about inflation and buying power. Then you do the key Coast FIRE move: you take that future FIRE number and discount it back to today using your expected rate of return on your portfolio, which gives you your Coast FIRE number, your target.

Once you have your Coast FIRE number target, the strategy moves to the savings execution phase. You must craft the most favorable earning and expenses situation you can to hit your Coast FIRE number as fast as possible, optimizing job, expenses, spouse/dependents reality, location, and anything that meaningfully increases savings without breaking your life. At this time, you earn and save aggressively until you hit that Coast number. As you save, you also invest smartly – diversified, low-fee, and aligned with your risk tolerance and risk capacity, so your plan isn’t fragile.

Step 2: After you hit your Coast FIRE number, the Coast Phase

This is where Coast FIRE becomes what people actually want it to be: breathing room.

You continue working and earning, but now, just to cover your current expenses, not to save. You no longer have to save aggressively to keep your retirement plan alive. That is what will change the entire feel of your working life. You can start making decisions based on lifestyle, quality of life, and how you want your days to look, rather than optimizing everything around maximum earning and maximum savings.

For aggressive FIRE types, this is the moment where 50% to 75% of your check isn’t being saved anymore. Keep in mind, the useful perspectives of the FIRE mindset don’t treat this new “financial breathing room” as “more to spend.” It treats it as a new financial space to optimize your life, with more flexibility, more sanity, more margin, or a better quality of work.

But “coast” doesn’t mean “never think about it again.” Coast FIRE only works if you check to ensure the train is still on the rails and adjust for any surprises. This means you need to check in yearly on your returns and your anticipated future FIRE number, whether your assets are growing roughly in line with the plan, inflation, your current lifestyle, and your planned (and likely) expenses in retirement. Regularly, you need to ensure the portfolio is still appropriate, and you adjust the course as necessary.

Step 3: After your full FI “FIRE date” (the choose-your-own-ending phase)

When you reach your full FI date, Coast FIRE turns into options – of financial independence or early retirement.

This is when you execute the real retirement planning to fully “FIRE”, and you decide whether traditional full retirement is even what you want. Barista FIRE, Expat FIRE, and other alternatives could be smarter, healthier, or simply more enjoyable versions of “work optional” suited to your personality and needs. Also, you and your life have likely changed in the decade(s) since your FIRE date, and it’s alright, and smart, to update your approach to life in FI accordingly.

Then, if you want the cleanest version of the story, you fully FIRE and celebrate: change your life, quit your job, and pursue what fulfills you. The point isn’t that you must stop working; it’s that at FI, you finally get to choose.

Compounding growth (on smart investments): The Key to Coast FIRE’s ease, potency, and success.

As compounding growth in your investments is a major engine in the Coast FIRE plan, let’s do a deeper dive into what it is, how it works, and why you should make it work for you as early as possible.

Lesson 1: Compounding growth of investments and starting early are powerful tools

Compounding growth is the miracle engine that can turn that 18-year-old’s $15,000 investment into a $1,000,000 net worth at 62, with time and no additional work. Compounding growth is the silent, invisible exponential growth that happens when the gains (in interest, dividends, or appreciation) from a previous year grow over the principal amount invested.

Simply put, as time goes on, not only does your money initially invested work for you, but the additionally earned money works for you as well, creating a compounding effect. So, while you could just invest $100 in 10 years (to work for you as an investment), if you invest $50 today, that $50 will create the $50 to work for you later.

In compounding, the money that is working for you is creating more money that will work for you, which will also create more money that will work for you…and the process continues endlessly, as long as you give it enough time.

The following chart depicts the growth of a single $10,000 investment experiencing compound growth over 20 years, with no additional investment

|

Year |

10% |

|

0 |

$ 10,000 |

|

1 |

$ 11,000 |

|

2 |

$ 12,100 |

|

3 |

$ 13,310 |

|

4 |

$ 14,641 |

|

5 |

$ 16,105 |

|

6 |

$ 17,716 |

|

7 |

$ 19,487 |

|

8 |

$ 21,436 |

|

9 |

$ 23,579 |

|

10 |

$ 25,937 |

|

15 |

$ 41,772 |

|

20 |

$ 67,275 |

Lesson 2: Choosing the right investments early is essential to maximizing compound growth

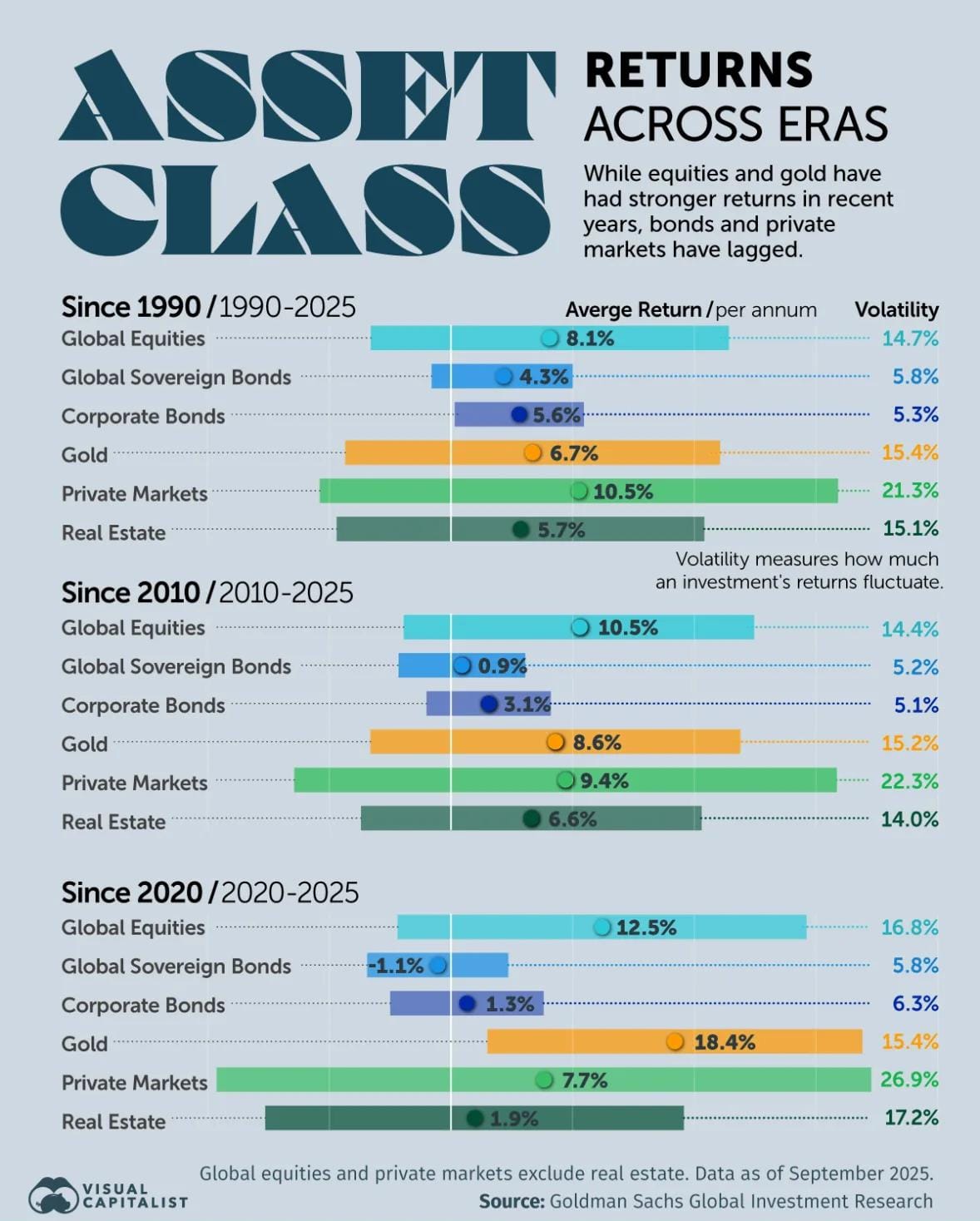

In addition to understanding and leveraging time and compound growth, understanding that smart investments that generate high yet reliable returns are essential to understanding this “time plus patience” formula.

In the example above, the required return for its success was10%, which is what the stock market has performed at for the last 15+ years.

Returns by Asset Class since 1990 | Infographic Source: Visual Capitalist; Data Source: Goldman Sachs Investment Research

In contrast, at current, the average return on a savings account is remarkably low at ~.6% (which we’ll round up to 1%), and even high-yield savings accounts only return 3.5% to 4% annually as of this year.

In the example below, we compare that same $10,000 invested over time at 10% (roughly stock market returns), 4% (high yield savings account returns), and .6% (average savings account returns).

|

Year |

10% (Market) |

4% (HYSA) |

0.6% (Savings) |

|

0 |

$ 10,000 |

$ 10,000 |

$ 10,000 |

|

1 |

$ 11,000 |

$ 10,400 |

$ 10,060 |

|

5 |

$ 16,105 |

$ 12,167 |

$ 10,304 |

|

10 |

$ 25,937 |

$ 14,802 |

$ 10,616 |

|

15 |

$ 41,772 |

$ 18,009 |

$ 10,939 |

|

20 |

$ 67,275 |

$ 21,911 |

$ 11,271 |

Later, we will discuss common Coast FIRE investment approaches to try and get as close to the market returns as possible, but internalize the two essential lessons that follow.

The Takeaways:

- Compounding growth is extremely powerful in building wealth

- Choosing the right investments and making your money work for you is just as powerful

The “72 Rule of thumb”: Market portfolios generally double every ~7.2 years

A commonly accepted finance rule of thumb is the rule of 72. While we go into the rule of 72 in another article**, accept this takeaway and rule of thumb for your rough planning.

A portfolio that maintains a return of 10% will double every ~7.2 years.

10% is the commonly accepted historical return of the US stock market, and the commonly accepted Coast FIRE investment approach aims match this in the accumulation phase.

So, what does this mean for you?

If your assets are smartly invested to match the market return of 10%, you can plan on your assets doubling every ~7.2 years during your “coasting” phase.

Try the calculator at 7% and 9% too; Coast FIRE is sensitive to assumptions.

How Coast FIRE differs from Traditional FIRE: Delayed gratification, lifestyle balance, and polarized experiences

Traditional FIRE is an approach to FI wherein the period of saving (accumulation) extends from now all the way until FIRE. At the FIRE date, the person then has all of the targeted asset amount and is fully capable of financial independence and retiring early at that time.

Traditional FIRE is different from Coast FIRE in that this period of saving, accumulation, sacrifice, and frugality is extended over a longer period of time. The benefit of this traditional FIRE approach is that the sacrifice (expense reduction and savings) is stretched over a longer period of time and thus less intense. The downside of the traditional approach is that the portion of saving and investment that happens later (than would happen in Coast FIRE) does not get as much time to benefit from the power of compounding growth that happens to investments made earlier.

In contrast, Coast FIRE leans toward saving very aggressively up front to maximize the leverage of time and compounding.

Coast FIRE trades “burst sacrifice” and receives a “normal lifestyle” in return over the rest of the career – traditional FIRE requires slow burn discipline, and frugal living through one’s entire career.

Coast FIRE is about stopping contributions once you’ve invested enough; Traditional FIRE is about stopping work once the portfolio can fund everything.

|

Approach |

What you stop |

What you keep |

Best for |

Main risk |

|---|---|---|---|---|

|

Traditional FIRE |

Full-time work (eventually) |

Full retirement funded by portfolio withdrawals |

People who want to make work optional ASAP and can sustain a high savings rate |

Sequence-of-returns risk early in retirement; underestimating expenses/healthcare. |

|

Coast FIRE |

Contributions (after you “hit the Coast number”) |

Working for current expenses; invested portfolio compounding |

People who can front-load savings early want a more normal life now, and don’t mind working |

Assumption risk (returns/inflation); the plan breaks if you stop too early or expenses rise |

|

Barista FIRE |

Full-time work (or high-stress work) |

Part-time income + partial portfolio withdrawals |

People who want time back sooner and can maintain a flexible income |

Income stability + benefits risk (healthcare); lifestyle creep during “semi-FI” |

|

Lean FIRE |

Most discretionary spending / high-consumption lifestyle |

Extreme simplicity + low annual spending + portfolio withdrawals |

People who value freedom over comfort upgrades and can keep expenses low long-term |

Low margin for error (health, housing, inflation shocks); burnout |

|

Chubby FIRE |

“Always more” spending pressure / constant upgrading |

Comfortable spending + margin + portfolio withdrawals |

People who want early retirement without deprivation, but not Fat FIRE |

Bigger target means longer runway; lifestyle creep if spending isn’t intentional |

|

Fat FIRE |

Most financial constraints on lifestyle |

High discretionary spending + margin + often more complex assets |

High earners/owners who want maximum optionality and comfort |

Complexity + creep (tax/estate/asset management); bigger sequence risk exposure due to higher withdrawals |

|

Expat FIRE |

Living in your home country, and paying high Cost of Living |

Your quality of life, and more of your money |

Those that are “international curious” |

Currency risk, culture shock, and isolation if there are no active attempts to integrate |

Which approach is better? That depends on the person.

The differences in sacrifice, timing, and outcome, and how worthwhile or not they are depend on your individual preferences, and your preference towards polarized experiences (pure relaxation, burst hard work) or moderation (balanced saving and frugal living at once) as both can achieve the same financial independence, at the same time – simply with different paths to get there.

Why choose Coast FIRE (quick explanation)

So now that you know that Coast FIRE and Traditional FIRE are equal in outcome (they both lead to financial independence) and actually cost the same amount in dollars (when adjusted for time and compounding growth), why would you choose Coast FIRE?

- To set yourself up for a robust investment portfolio later, eliminating the effects of some unpredictability (of employment, life, and the ability to save) along the way

- To intentionally commit to a period of sacrifice and savings when you are mentally and logistically prepared for it, and during times of more flexibility (single, no kids, more career mobility, and during the resilience of youth)

- To give yourself breathing room to enjoy life sooner (after a strategic, expected compromise) instead of a lifetime of saving

- To achieve the early peace of mind / lowers stress that comes from getting the “retirement work” done early in life.

- To allow for more work-life balance after hitting your Coast FIRE number, as less money is required (with no need to save), allows for lower hours or lower pay along the way, and the opportunity to live more in the place of work is no longer required.

- Allows the flexibility to add more later – if you anticipate lifestyle creep, or want a more luxurious FI period, having no current savings requirement means you can “top off” your Coast FIRE number at will.

Coast FIRE in one equation

Your Coast FIRE Number = Your Future FIRE Number / ((1 + expected returns) ^ years of coasting))

Or, the same equation stated a different way…

The Lump Sum Amount You Need to Save = Your Future FIRE Number / ((1 + expected returns) ^ years of coasting))

This single equation takes the amount that you will need for financial independence in the future (Your Future Fire Number), then “discounts the number” (using your expected returns) by calculating how much money invested today, at that expected rate, would grow into your FIRE number.

We will get into the details of the math later, but your future FIRE Number can be calculated as “25 x your future annual expenses,” assuming a 4% withdrawal rate in retirement.

Use our Coast FIRE Calculator to quickly find your numbers

While it is great to understand the financial math, using our calculator allows you to quickly test assumptions, rates of return for varying portfolio aggressiveness, and timelines to FIRE.

Quick Coast FIRE Calculator

Estimate the portfolio you’d need today so that, with no further contributions, it grows into your full FIRE number by the time you retire.

If you invest $516,838 today and let it grow at 7.0% annually, in 20 years you’ll have enough to support $80,000 per year in retirement using a 4.0% withdrawal rate.

| Portfolio needed at retirement | $2,000,000 |

|---|---|

| Years of growth | 20 years |

| Expected annual return | 7.0% |

| Amount needed today (Coast FIRE) | $516,838 |

How to use our full Coast FIRE calculator

- Enter Expected annual expenses in retirement

- Enter your Annual withdrawal rate (%)

- Enter your Expected annual investment return (%)

- Enter Years until retirement

This is the quick calculator to help you internalize the possibilities while reading this article. Visit here for our full Coast FIRE calculator with charts, reports, and button to share your projections.

The Math behind Coast FIRE

Coast FIRE has two numbers (and one job).

The two “numbers” that power Coast FIRE are:

- Your Future FIRE number (later): the portfolio size you want at retirement age, the amount that can generate enough income to cover your annual expenses.

- Your Coast FIRE number (now): the amount you need invested today for it to grow into your FIRE number by a specific date, even if you stop contributing.

The math is just one idea: take a future goal and discount it back to today.

Step 1: Find your future FIRE number

First, decide your target retirement age, because that tells you how many years your money has to “coast.”

Next, estimate your annual expenses in retirement.

One reality check: because of inflation, lifestyle creep, and the boring-but-real costs of aging (especially healthcare), your retirement expenses will usually be higher than today unless you intentionally design them not to be.

Then calculate your FIRE number using the classic rule of thumb:

FIRE Number (future) = 25 × annual expenses in retirement

That “25×” is just the 4% rule in disguise (1 ÷ 0.04 = 25). If you want a more conservative plan, long retirements, more margin, or leaving money behind, you can stress-test 29× (3.5%) or 33× (3%) instead.

For a deeper review on choosing withdrawal rates (4%, 3.5%, 3%, etc.), the 4% rule, and FIRE numbers, read this section on the Simple Math of FIRE.

Step 2: Discount it back to today (your Coast number)

Now take your future FIRE number and discount it back to a number you can aim for today using this equation:

Your Future FIRE Number ÷ ( (1 + expected return) ^ years of coasting ) = Your Coast FIRE Number

That’s it.

It’s the same logic as asking: “How much do I need to invest right now so that, with time and compounding, it becomes my target later?”

Important: don’t use a single assumed return like it’s a promise. Test your potential plan multiple times using a range of returns (7%, 8%, 9%…) and build a plan that survives the less flattering versions.

A simple example

Let’s say you want $1,000,000 at retirement in 20 years and you assume 10% annual returns.

$1,000,000 ÷ (1.10 ^ 20) = $148,643

So if you invested about $148,643 today, and you truly earned 10% for 20 years, you’d land at ~$1,000,000.

This is a simplified model – inflation and return variability are exactly why Coast FIRE requires stress-testing and annual check-ins. (More on that below.)

Example Math (20-year snapshot)

|

What you’re solving for |

Years |

Expected return |

Input |

Output (rounded) |

|---|---|---|---|---|

|

If you invest $200,000 today, what does it become? |

20 |

7% |

$200,000 today |

~$774,000 in 20 years |

|

20 |

8% |

$200,000 today |

~$932,000 in 20 years | |

|

20 |

9% |

$200,000 today |

~$1,121,000 in 20 years | |

|

20 |

10% |

$200,000 today |

~$1,346,000 in 20 years | |

|

If you want $1,000,000 in 20 years, what do you need today? |

20 |

7% |

$1,000,000 target |

~$258,000 today |

|

20 |

8% |

$1,000,000 target |

~$215,000 today | |

|

20 |

9% |

$1,000,000 target |

~$178,000 today | |

|

20 |

10% |

$1,000,000 target |

~$149,000 today |

This is simplified compounding math. Real life includes inflation, taxes, and markets that don’t move in a straight line, so the point is to stress-test assumptions, not worship one number.

How to calculate your Coast FIRE number (fast and correctly)

- Choose your target retirement age

- Estimate retirement spending (in the lifestyle you actually want)

- Compute your FIRE number: expenses × 25 (or × 29 / × 33 for more margin)

- Choose an expected return range (I’d start with 7%–9% for planning; run 10% as a “best case,” not your only case)

- Count your years of coasting (today → retirement age)

- Discount back to today: FIRE number ÷ (1 + return) ^ years

Then compare the result to what you have invested.

The assumptions that drive the math (and where you start)

Coast FIRE isn’t hard because the formula is complicated. It’s hard because three assumptions quietly run the show:

- Inflation (your future expenses are not today’s expenses)

- Your expected return (and the fact that it won’t be smooth)

- Your spending (because life changes, family, health, location, priorities)

The way you stay sane is simple:

- Run multiple return assumptions (7%, 8%, 9%, 10%, etc.)

- Build a margin buffer.

- Commit to a yearly check-in to adjust course.

Coast FIRE works best when it’s treated like a true, adaptive plan, and not a one-time calculation you do once at 25 and never revisit.

The risks and “good to knows” before starting Coast FIRE + how to mitigate

Coast FIRE is simple on paper: one lump sum (or a front-loaded saving phase) + time + compounding. But the plan can still break in real life if you inflexibly treat the math like a guarantee written in stone instead of a model you can, and should, adapt.

Here are the big risks and the “good to knows” worth internalizing before you commit to the approach.

Major sacrifice initially: The upfront cost is real

To make Coast FIRE a significant and worthwhile approach, you usually need a meaningful cash outlay early.

For example, to target a $1,000,000 portfolio in 20 years, a cash outlay now of ~$150,000 would be required (at ~10% assumed returns). While the outlay is minuscule compared to the gain, that could be a mountain of cash for the average 20-year-old.

That’s the trade: Coast FIRE asks you to do the hard part early, when you have the most compounding runway, and then “coast” without the same savings pressure later.

Keep in mind that you don’t have to do it as one dramatic lump sum. You simply have to achieve your savings target (Coast FIRE number) by your “Coast date.”

A realistic version looks like this:

A 20-year-old tradesman who saves $1,300 per month for 10 years (from age 20 to 30), then stops saving and investing at 30, would have a $1,888,355 portfolio at 50.

That 20-year-old sacrifices for a decade. However, he lives age 30 to 50 more comfortably than the average person (and with hard-earned but intuitive financial discipline), and lives even more comfortably at 50, a millionaire, financially independent with the option to retire early.

The point: Coast FIRE is “easy” later because it’s harder earlier, and the size of that early push depends on your timeline, your return assumptions, and how much margin you want.

Ensure to stress test assumptions (7%/9%/10% returns) with realistic plan Bs for all scenarios.

These calculations are sensitive to the assumptions, especially expected returns.

Don’t plan Coast FIRE with one number that looks perfect. Recalculate your plan and the math behind it at 7%, 9%, and 10% (or whatever range fits your portfolio and risk tolerance) and ask:

- What if I get the “good” outcome?

- What if I get the “mediocre” outcome?

- What if I get the “bad” outcome, and I still want my life to work?

A real Coast FIRE plan includes plan Bs that you can execute without panic: contribute again for a year and downshift later, move the target date, or use an “escape hatch” strategy.

Good math is required up front (financial advisor consultation recommended)

The Coast FIRE approach rewards good planning and punishes sloppy planning.

You’re essentially saying: “I will stop contributing intentionally and trust the financial engine I’ve built.”

That’s a different level of commitment than “I’ll just keep saving and see what happens.”

So, yes, this is one of those cases where a financial advisor consultation recommended is not a throwaway line, especially if you’re basing your timeline on tight assumptions. A good fee-only financial advisor will be competent in calculating the math, reviewing the assumptions, and addressing issues that a novice FIRE planner may overlook.

Coast FIRE plans may require “adjustments” later and are not “set-it-and-forget-it.”

Even if you nail the math today, you still need a system for updates later.

Tax laws may change, you may change countries, change marital status, or even add children/dependents to the equation. This is all ok, you just need to remember to check and update the plan.

Your plan needs to be able to absorb that without collapsing.

Market performance is a wild card.

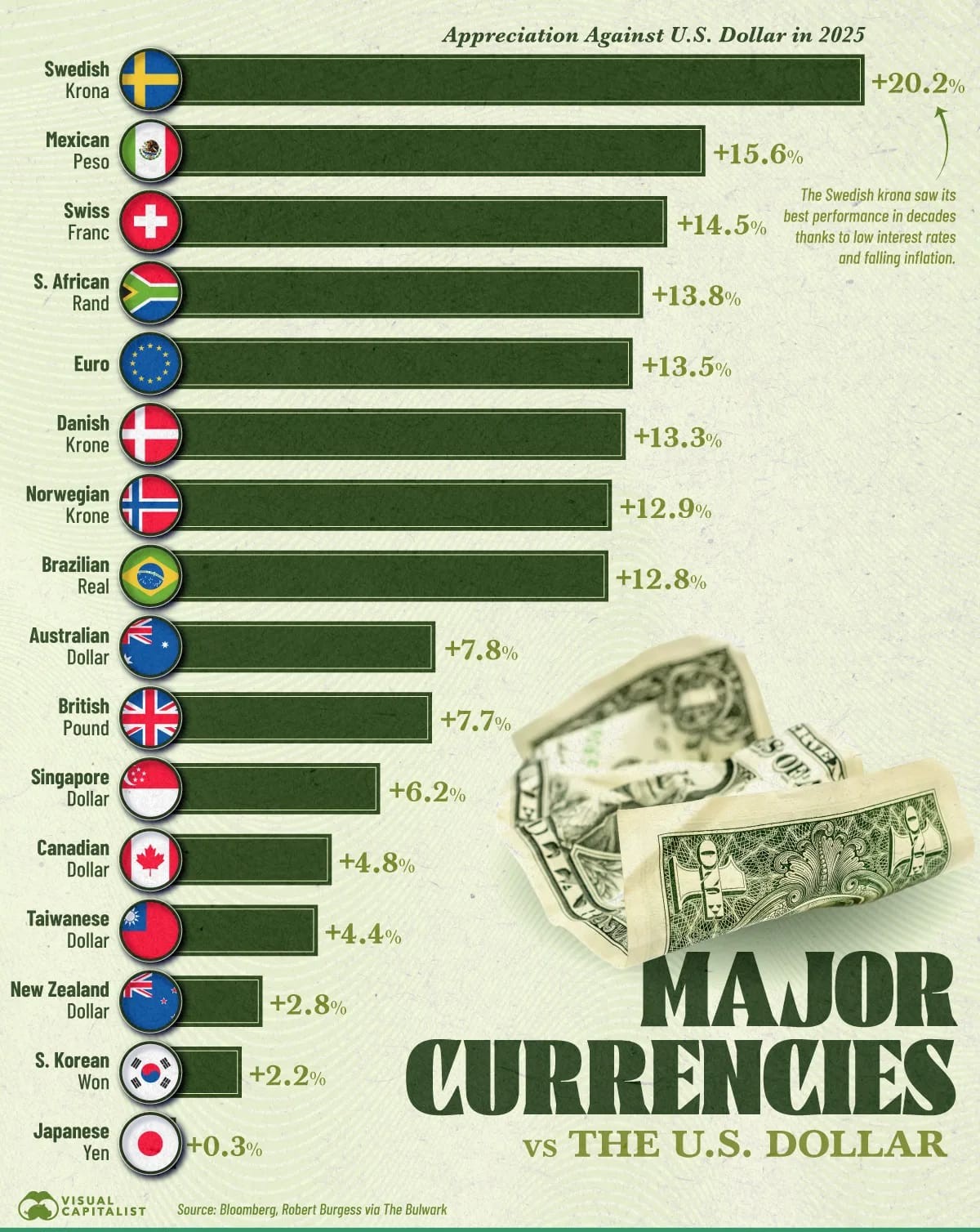

These calculations are usually based on historical returns of the US stock market, but the world is rapidly changing.

Additionally, a notorious statement in finance is, “Past performance is not a guarantee of future performance.”

If you invest in global markets or if you plan to spend in a different currency in retirement (perhaps as ExpatFIRE), different variables present themselves.

Infographic of US Dollar power reduction against major currencies | Source: Infographic produced by Visual Capitalist; Data Sourced from Bloomberg

The point is not “don’t do it.” The point is, continue educating yourself and involve a savvy financial professional in the planning until you feel confident in your personal financial planning skills, and check in on your portfolio, market performance, and your plans in retirement (expenses, destination, lifestyle) once a year to adjust course as necessary.

Sequence of returns risk

Sequence of returns risk is usually discussed for retirement withdrawals, but it matters here too, because your outcome depends heavily on what markets do during the years you’re relying on compounding.

And there’s a related risk people don’t think about:

- Losing out on significant bull markets by being too conservative too early, or by parking money in low-return “safe” places that don’t compound the way your model assumes.

If your plan requires equity-like returns, your portfolio has to be built (inherently aggressively) to pursue them, within your risk tolerance and time horizon.

Essential Mitigations in Coast FIRE:

If you want Coast FIRE to feel calm (instead of fragile), build these guardrails in from day one:

- Assumption stress tests (7/9/10% returns)

- Inflation adjustment

- Annual check-ins

- Sequence of returns risk awareness

- “Escape hatches” and plan B options (Barista/Expat/keep contributing in bad years)

Inflation and Spending Variability: Two important factors in Coast FIRE planning

If Coast FIRE is the “time and compounding” plan, then inflation and spending variability are the two forces that quietly try to ruin it.

Inflation: your future expenses are not today’s expenses

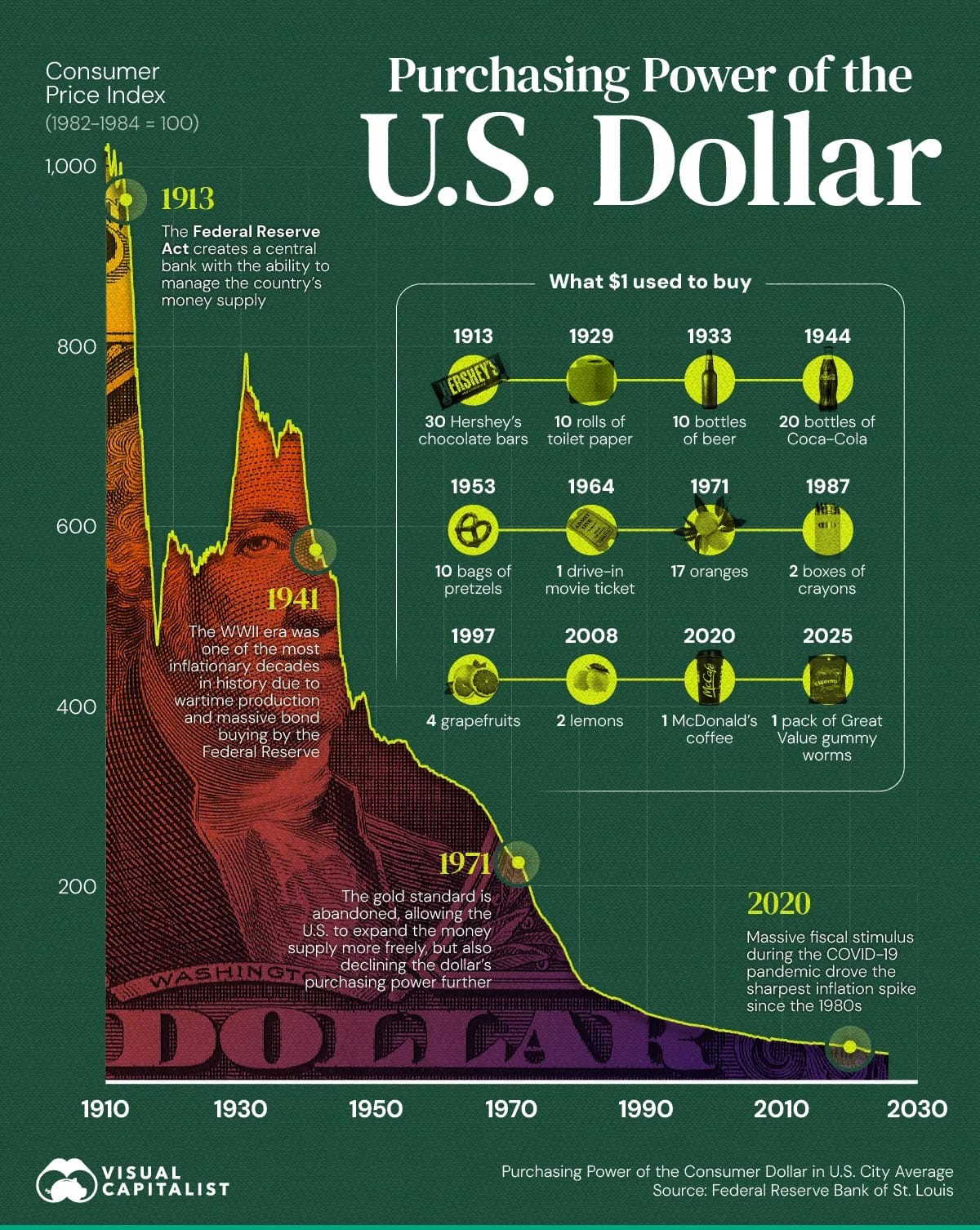

The math breaks when you calculate a FIRE number using today’s spending, then pretend the future has the same buying power.

Infographic depicting loss in buying power of the US dollar and inflation in prices since 1910 | Infographic Source: Visual Capitalist; Data Source: Federal Reserve Bank of St. Louis

Even mild inflation (such as 1% to 3%) compounds over long periods. Coast FIRE planning lives in long periods. That means inflation shouldn’t just be a footnote; it’s core math.

There are two clean ways to handle inflation:

Option A (simple):

Keep your retirement expenses in today’s dollars, and use a “real return” assumption (expected return minus inflation).

Option B (also valid):

Inflate your future expenses forward, calculate the future FIRE number in future dollars, then discount back using nominal returns.

You don’t need perfection here; you need consistency. If you mix nominal and real numbers, you’ll confuse yourself and overestimate safety.

For more information, read our inflation explainer to understand nominal vs real returns **

Spending variability: the “future you” problem

Coast FIRE is planned far out. That’s the feature and the risk.

A plan built at 25 assumes you know what 45 or 55 looks like. But life changes:

- lifestyle creep

- family commitments

- healthcare

- the economy

- where you live (and what that costs)

This is why annual check-ins matter. Not because you’re doing it wrong, but because you’re doing a long-range plan in the real world, and discovering who future is, and their unique needs different from your needs now, along the way.

The simplest safeguard is a yearly “reality audit”:

- Did my spending assumptions change?

- Did my retirement lifestyle change?

- Did inflation shift the goalposts?

- Is my portfolio still aligned with the returns I’m assuming?

- Do I need to top off, delay, or pivot?

Some forms of FIRE are reasonably simple to DIY because the strategy is “keep saving, keep investing, adjust slowly.”

Coast FIRE is different. You’re making an intentional decision to stop contributing (or dramatically reduce contributions) and rely on compounding to do the heavy lifting.

That can be a brilliant move, but it’s also a plan that deserves either:

- a one-time review from a fee-only financial planner, or

- disciplined personal monitoring (annual check-ins, updated assumptions, and a clear Plan B).

The goal isn’t perfection. The goal is not to be surprised ten years later by something you could have stress-tested on day one.

And to be clear: “help” doesn’t mean being sold products. It means confirming your assumptions, your risk, your inflation handling, and whether your plan has enough margin to survive real life.

What does it realistically take to reach Financial Freedom via Coast FIRE?

Here’s the honest answer: Coast FIRE is not “easy.” It’s just simple. The lever is time. The price you pay is that the plan asks for meaningful action early, then rewards you later with breathing room.

Everything below is simplified compounding math (no taxes, no inflation adjustments, no messy markets). It’s meant to give you intuition and guardrails, not a false sense of certainty.

Coast FIRE Realities by Age

18 to 25: the perfect time to start

Reality: This is the window where small dollars now can do massive amounts of work later, because they have decades to compound.

- $50,000 saved today is roughly $1.4M to $2.7M by age 60

- $1,000,000 at 60 requires $36k today.

At this age range, the “price” of $1,000,000 at 60 is still shockingly low: roughly $18k–$36k invested once (again: simplified, assuming ~10% returns). - $1,000 invested at 20 is the same as:

- $2,594 at 30

- $6,727 at 40

- $17,449 at 50

Same destination. Very different price tag.

Tips:

- Consider a pre-university high-paying work stint to stash away well-invested assets.

- $15,000 invested at 18 years old will become ~$1,000,000 at 62. One aggressive summer of work and savings before university, invested, and no further savings, can make a millionaire at 62.

- $20,000 invested at 21 years old will become ~$1,000,000 at 62. Two to three summers of serious internship savings can be all it takes.

(Again: simplified math. Real life requires inflation adjustment and annual check-ins, covered elsewhere in this guide.)

25 to 30: the most potent opportunity period for investing

Reality: This is still the “cheap” decade in a “high value” period. You’re old enough to earn real money, young enough that time and flexibility are still on your side.

- The same $1,000,000-at-60 target now costs you roughly $36k at 25 or $57k at 30 (invested once, assuming ~10%).

- That’s the Coast FIRE trade: every 5 years you wait, the upfront requirement jumps significantly.

Tips:

- If you’re going to do a “burst sacrifice” period, this is prime territory: fewer obligations than your late 30s, more income than your early 20s, and still a long runway.

30 to 35: savings need to be higher (and it’s less effective than your 20s)

Reality: Coast FIRE still works here, but the “price” is rising fast.

- You’re now in the phase where savings need to be higher because you have fewer compounding years left.

- For many people, this is the last period to invest heavily before life responsibilities kick in.

Tips:

- Treat this phase like a short campaign: tighten fixed costs, concentrate savings, and avoid the “I’ll do it later” drift that quietly kills Coast FIRE plans.

35 to 40: The struggle becomes balancing savings with responsibilities

Reality: At this point, the math is still doable, but the lifestyle friction is higher.

- The struggle is balancing large savings with responsibilities: mortgage, family expenses, and less flexibility.

Tips:

- Whether or not you decide to Coast FIRE, set a priority that all one-time windfalls (bonus, tax returns, inheritance) go directly to savings.

- Also consider: Expat FIRE and Barista FIRE if the “save more” lever is maxed out, but you can still change your cost structure or income model.

40 to 50: You can still apply the Coast FIRE approach, but you need significant alternative leverage. Realisticly other options are possibly better

Reality: Coast FIRE in 40s and 50s isn’t “too late,” but it’s much harder to brute-force with compounding alone. You’ll usually need some combination of:

- Higher contributions,

- A later target date,

- A strategy shift.

Tips:

At this point, consider Expat FIRE and Barista FIRE instead. These alternatives can function as “escape hatches” when you want to keep the goal but reduce the pressure.

Realistic Saving and Investing Timelines

These are “back-of-napkin” numbers for intuition, assuming a rate of return of ~10% and no inflation/tax adjustments. The goal of this is not precision; it’s awareness and helping you understand how the lever works.

Be sure to run the Coast FIRE calculator at 7–9% too.

What does a $1,000,000 target cost at different starting ages (by age 60)

|

If you’re… |

Years to age 60 |

$1,000,000 at 60 requires …(invested today) |

|---|---|---|

|

20 |

40 |

$22,000 |

|

25 |

35 |

$36,000 |

|

30 |

30 |

$57,000 |

|

35 |

25 |

$92,000 |

|

40 |

20 |

$149,000 |

This is the “Coast FIRE tax” of waiting: time is either your engine or your enemy.

$1,000,000 / $2,000,000 / $3,000,000 targets by timeframe (invested today)

Assuming ~10% annual returns:

|

Target |

In 10 years |

In 20 years |

In 30 years |

|---|---|---|---|

|

$1,000,000 |

$386,000 |

$149,000 |

$57,000 |

|

$2,000,000 |

$771,000 |

$297,000 |

$115,000 |

|

$3,000,000 |

$1,157,000 |

$446,000 |

$172,000 |

If those numbers feel impossible, that’s not a personal failure; it’s the math telling you which lever you need: more time, more contributions, a later target date, or a different strategy (Barista / Expat / keep contributing longer).

Practical Strategies for Coast FIRE

The Coast FIRE approach: Build the engine early, invest it intelligently, then stop needing to save aggressively while the portfolio compounds in the background.

The practical strategies come down to two questions:

- How do you invest in a way that actually captures compounding?

- How do you create the kind of early “burst” savings that make the whole plan work?

Most Coast FIRE plans don’t fail because compounding “doesn’t work.” They fail because people never create the conditions to invest enough early for compounding to matter.

Common FIRE investment approaches: Diversified, low-fee ETFs

The classic Coast FIRE investment approach is boring on purpose: broad market, diversified investing with low fees, built around your investment risk tolerance (and your ability to stay invested when markets get ugly).

In practice, that usually means:

- Broad market index exposure, not stock picking, not timing, not “one weird trick.”

- Diversification across sectors and, ideally, geographies, such as a mix of U.S. and international exposure, if that fits your plan

- Low fees so compounding doesn’t leak out through expense ratios and unnecessary trading

- Consistent and automated, because Coast FIRE breaks when the plan relies on motivation

The job of this portfolio isn’t to be clever. It’s to be durable and reliable, something you can hold for decades without constantly second-guessing yourself.

The cleanest rule here is your Coast FIRE math assumes you’ll earn market-like returns over time. Your portfolio needs to be built to pursue that, within your risk tolerance and risk capacity.

And if you’re doing anything more complex than broad diversification and low-cost funds, it’s worth doing the grown-up thing: educate yourself and talk to a fee-only advisor to make sure the numbers work and you’re not accidentally building a fragile plan.

Alternative options of investment: Real Estate, Lifestyle businesses

Coast FIRE can be powered by investments other than index-style investing, but you want to be honest about what you’re signing up for.

The headline difference is simple:

- Index investing is mostly passive (once it’s set up).

- Real estate and lifestyle businesses can be excellent, but they’re rarely passive in the way people advertise, and returns depend on the efficiency that comes from active involvement.

Real estate can work when the numbers genuinely work (and the risks are understood): rental property cash flow, house hacking, value-add renovations, or even REITs if you want real estate exposure with less operational complexity. The tradeoffs: concentration risk, illiquidity, tenant/maintenance stress, and local-market dependence.

While there are a multitude of factors that determine whether real estate investment is a viable Coast FIRE path for you, it depends on your experience, your location, and the context created by your life, as displayed in the opportunity of “rentvesting”.

In the beginning, staying within your area of competence and maintaining simplicity while also maintaining returns that support your FIRE plan isn’t a bad bet.

Lifestyle businesses can also power Coast FIRE, especially if you build something that throws off steady profit and doesn’t require your soul as ongoing collateral. But again: it’s not “set it and forget it.” It’s a different kind of work, and often a different risk profile.

The Coast FIRE filter is this: does the approach reliably convert early effort into long-term compounding without requiring constant heroics? If yes, it can belong in the plan. If not, it might still be a good idea, just not a Coast FIRE engine.

For an introduction to lifestyle business opportunities as investments, I highly recommend the book Main Street Millionaire by Cody Sanchez.

Engineering a Coast FIRE “windfall” season

When people hear “windfall,” they picture luck – perhaps an inheritance, or a good weekend in Vegas. In Coast FIRE, “windfalls” are usually engineered by creating a situation that will deliver the earnings and savings your Coast FIRE plan needs.

The pattern you’re looking for is high savings potential for a short season, especially setups where major expenses are covered (housing, food, transport), or where overtime/per-diem makes the income unusually dense.

1) The criteria: what you’re actually hunting for

To outperform the generic advice, keep it simple. You’re looking for:

- High income density: high pay per month, not just “good salary.”

- Low expenses: ideally, expenses paid, or spending outlets naturally constrained

- Finite duration: a defined season, so it feels like a campaign, not a permanent struggle.

- Tolerable stress: hard, but survivable; you can do it without breaking your life.

A job is Coast-FIRE-friendly if it checks 3 of 5:

- Housing provided or cheap

- Meals/per diem provided

- Lots of overtime / long rotations

- Defined season (6–24 months)

- Limited spending outlets (you can’t lifestyle-creep easily)

2) Coast FIRE “Windfall Job” archetypes: Repeatable setups that tend to work

These aren’t necessarily the “best” jobs for filling your Coast FIRE fund. They are conditions that repeatedly create burst savings and are meant to spur ideas for how you can create burst savings.

My previous experience working on high-paying overseas defense and security contracts, and my later “stint” in management consulting, were the two periods that most empowered my FIRE journey. From personal experience, I highly recommend exploring similar “windfall jobs” to catapult your FIRE journey forward as well.

Archetype A: FIFO / rotational / camp-based work creates high pay with forced simplicity

The purest Coast FIRE setup is earnings density + constrained spending. If housing and meals are covered (or heavily subsidized) and you’re working long rotations, you can create a burst sacrifice phase without needing superhuman willpower. It’s not glamorous. It’s strategic.

Archetype B: Travel-paid work: Stipends, per diem, and expenses covered create ample financial margin

Travel work applies essentially the same logic. The work moves, but your fixed costs don’t explode. The savings rate stays high because the structure is doing the discipline for you.

Archetype C: Overseas contracting and “project” work: A defined horizon with minimal spending traps

Often, higher pay, fewer lifestyle spending outlets, and a defined time horizon. This can be a Coast FIRE “campaign” if you treat it like one.

Archetype D: Seasonal immersive work: Creates a live where you work scenario

Seasonal work becomes Coast FIRE-friendly when it’s immersive, and your day-to-day life is built around the job, expenses are efficiently covered, and spending opportunities are naturally limited. The result is maximum time worked (and maximum compensation) and minimal time to spend those earnings.

Archetype E: Commission sprints offer high upside, but sales are always personality-dependent

True windfall potential in a short time, if you can sell and keep spending in check. The risk is volatility and burnout, so treat it like a sprint, not a permanent lifestyle.

Archetype F: “Remove housing” roles may offer moderate pay, but compensate with extreme savings rates.

Windfall job salaries don’t always need to be high. Because housing is the biggest expense for most people, removing the housing expense can change everything.

Archetype G: “Overtime season” in your current job

This is the most overlooked. One year of aggressive overtime combined with a lifestyle freeze can be a windfall in disguise without switching careers.

Archetype H: Temporary geographic arbitrage, including taking on the Expat/nomad life for a season

Work stays the same; cost structure changes. If you can work remotely, a 6–18 month lower-cost base can create a savings surge without changing your job.

3) Examples of jobs to get your research started

Below are specific examples of jobs and job fields that generally don’t require a new university degree to get started. Some need short certifications, a clean background check, and a willingness to grind for a season. All present a burst earnings opportunity, and the opportunity to hit your Coast FIRE number goals.

FIFO / remote-site / rotational work with expenses covered

- Oil & gas/energy field ops: Entry tracks like roustabout/leasehand/floorhand/pipeline support

- Mining site roles: Site labor, haul truck driver, plant/operator assistant

- Wind/solar field construction travel crews

- Remote camp services: Lower pay, but near-zero expenses

Travel-paid / stipend-heavy work

- Travel nursing: The cleanest version of this model, because the contracts and housing structure are built-in

- Other contract travel roles, including per diem and the opportunity for overtime pay

Overseas contract or project-based work

- Overseas contracting work: Often higher pay with a defined time horizon

- Milestone/bonus-based project roles paid in lumps rather than slow monthly drips

Immersive seasonal, “live where you work” employment

- Resort seasonal work with housing, such as in ski towns and national parks

- Cruise ship work or maritime-adjacent hospitality roles

- Remote tourism operations and expedition-style roles

Trades/shutdown/turnaround opportunities with high overtime and per diem

- Industrial shutdown/turnaround crews

- Scaffold builder/rigger / firewatch / flagger

- Union construction paths, which often have paid training/apprenticeship in many places

Why these careers and situations fit Coast FIRE

Because they solve the hardest part of Coast FIRE: generating the lump sum invested needed to get to the Coast FIRE number.

These situations do three useful things at once:

- They make saving large amounts possible – sometimes for the first time.

- They make saving large amounts automatic – because expenses are constrained.

- They turn Coast FIRE into a campaign instead of a lifelong austerity identity.

And that’s the point of Coast FIRE: do the hard part early, intentionally, and for a defined period, so you can live a more normal life while the engine runs.

For more ideas, read our Windfall Job Brainstorm List

How to Coast FIRE (A Roadmap)

The goal of this roadmap is to guide you in turning your potent idea of achieving Coast FIRE into a plan you can execute, without getting lost in spreadsheets or false precision.

- Pick your target retirement age, and what “retired” actually means for you.

Coast FIRE starts with a date. Your timeline determines how much compounding runway you have and the numbers required from there. - Define your “future lifestyle” expenses (not your current expenses).

This is where people accidentally sabotage themselves within Coast FIRE. Inflation, lifestyle creep, healthcare, and family commitments all matter. Your retirement spending will almost certainly be higher than now unless you intentionally design it not to be. For now, plan for it to be reasonably higher, and add a margin for error. - Calculate your future FIRE number.

Use the simple rule of thumb:

Your FIRE Number = 25 × your annual expenses

(Or, consider running a conservative version – 29× or 33× – if you want a long retirement and more margin.) - Discount that future FIRE number back to today, using your expected rate of return, to find your Coast FIRE number.

This is the heart of the method:

Coast FIRE Number = Your FIRE Number ÷ ((1 + expected returns) ^ years of coasting)

You’re taking the future finish line and calculating what amount invested today would grow into that number. - Stress-test assumptions before you commit to the plan.

Don’t run Coast FIRE with one optimistic return assumption and vibes. Run returns of 7%, 9%, 10% and decide what you’ll do in the “less flattering” scenarios. This is where Coast FIRE becomes resilient instead of fragile. Use the Coast FIRE Calculator to help you quickly explore options in this step. - Create your “burst sacrifice” plan to hit the Coast number.

Coast FIRE is about bulk sacrifice early and up front + time + the power of compounding.

Whether you hit the number with a lump sum, a 2–3 year sprint, or a 5–10 year campaign, the goal is the same. Just aim to get enough invested to coast, ASAP. - Invest simply, consistently, and in a way you can hold.

Coast FIRE doesn’t require exotic strategies. It requires that you avoid self-sabotage in your investing approaches: high fees, unnecessary trading, and portfolios you can’t stick with when markets get ugly. Keep your investing simple. - Once you hit your Coast number, choose your coast mode, and set your check-in system.

After your “Coast FIRE date,” you make decisions for your career based on lifestyle, quality of life, and current earnings, instead of obsessing over maximum savings.

But you still check in once a year to ensure:- Your Coast funds are on track

- Your portfolio is still appropriate

- Your expenses and retirement plan still match reality

Then you adjust the course as necessary.

Coast FIRE is “pay now, retire later,” followed by “live normally, but without the stress of aggressive saving.” That’s the whole point.

Alternative Strategies: FIRE’ing on time, but Expat FIRE temporarily to allow continued “half rate” growth

There’s a strategy that doesn’t get talked about enough because it doesn’t fit neatly into one label:

You can Coast FIRE and use Expat FIRE temporarily as a lever for more asset growth, so you still FIRE on time, but with less pressure.

Coast FIRE is often built around the assumption that once you hit the Coast number, you stop contributing and let compounding do the rest.

But if life gets more expensive, markets underperform, or you want more financial margin… You have options that don’t require “going back to the grind.”

One of the cleanest options is to change your cost structure for a season.

If you temporarily move abroad (Expat FIRE), you can lower your cost of living without lowering your quality of life, and then use that extra breathing (savings) room to:

- Keep investing at a “half rate” (not a full FIRE savings rate, just enough to stay on track)

- Reduce withdrawals or reduce pressure on the plan

- Buy time so compounding can keep doing what it does best

It’s the same Coast FIRE logic of time + compounding, but you’re giving the engine a smoother road, or time to catch up if plans go awry.

A practical version of this looks like:

- You hit your Coast number (or get close).

- You realize your assumptions need more margin for error to compensate for hiccups (inflation, spending increases, low market returns).

- Instead of trying to force huge savings in a high-cost life, you do a temporary Expat FIRE phase: 12–36 months in a lower-cost, high-quality location, allowing you to save more income.

- You keep working, but your expenses drop enough that you can invest meaningfully, even if it’s only “half rate.”

- Then, when you’ve completed the “top up” to your assets, you return to your base life with a stronger portfolio, a stronger plan, and less stress.

This is especially powerful if your plan includes any of these realities:

- You’re in the 35–45 window, where responsibilities make aggressive saving hard

- Your retirement lifestyle is likely to be international anyway

- You want an “escape hatch” that’s not just “work more.”

Two important “good to knows” if you use this approach:

- Currency, taxes, and residency matter.

If you plan to spend in a different currency in retirement, or invest globally, variables change. This is not a reason not to do it; it’s a reason to plan properly and check in yearly. - Expat FIRE is not a vacation strategy. It’s a planning and financial lever.

The point isn’t “move abroad because it’s cheap.” The point is: use location intentionally to keep your Coast FIRE plan resilient, especially when inflation or life changes start moving the goalposts.

If you want to go deeper on how to do that responsibly (visas, taxes, healthcare, currency risk, lifestyle design), see the Expat FIRE guide here: The Complete Guide to Expat FIRE.

The differences between FIRE types: Coast FIRE vs. Barista FIRE vs. Traditional FIRE vs. Expat FIRE…

Coast FIRE differs from the other types of FIRE in the timing of savings, prioritizing lifestyle in the “mid years”, comfort with your current work status, and the willingness to “lump” strategic actions into specific periods (investing, saving, enjoying).

If you like your work but hate the pressure to save forever, Coast FIRE fits. If you want time back now, Barista FIRE fits. If you want a smaller number through location, Expat FIRE fits. And if you want ‘never think about money again,’ you’re drifting into Chubby/Fat territory, whether you label it or not.

A helpful way to think about it: every FIRE subtype is trying to solve the same problem, how to make work optional, but they use different levers.

- Traditional FIRE pulls the savings-rate lever for a long time.

- Coast FIRE pulls it hard early, then lets time do the rest.

- Barista FIRE uses part-time income to shrink what the portfolio must cover.

- Expat FIRE changes the cost structure (and sometimes taxes) by changing location.

- Lean / Chubby / Fat mostly change the lifestyle target and therefore the size of the number.

Below is the cleanest way to distinguish the different approaches to FIRE:

Traditional FIRE

Traditional FIRE is the classic “save and invest aggressively until the portfolio can fund 100% of your life.” You work now, you accumulate continuously, and at the FIRE date, you stop needing earned income.

How it differs from Coast FIRE:

Traditional FIRE extends the period of saving (accumulation) from now all the way until FIRE. That’s the slow-burn approach: ongoing discipline, ongoing savings, and usually ongoing frugality.

Coast FIRE flips that timeline. It concentrates the hard work, sacrifice, and saving into a shorter period earlier, because dollars invested earlier get more years of compounding growth. Coast FIRE is about stopping contributions once you’ve invested enough; Traditional FIRE is about stopping work once the portfolio can fund everything.

Traditional FIRE is Ideal for:

- People who want to work part-time ASAP and can sustain a high savings rate

- People who want a cleaner “finish line” psychologically (full FI, not partial)

- People who don’t mind the slow burn as long as the path is straightforward

Learn more in the Complete Guide to Financial Independence and Retiring Early

Barista FIRE

Barista FIRE is the “dial” version of FIRE. Instead of waiting until the portfolio covers 100% of your life, you aim for partial FI and keep a part-time income stream to cover the rest (often with an eye toward benefits like healthcare).

How it differs from Coast FIRE:

Coast FIRE is primarily a timing strategy – save early, invest, let compounding work, keep working for current expenses while the portfolio grows in the background. Barista FIRE is primarily an income structure strategy – keep part-time earnings so the portfolio has less to do.

In other words:

- Coast FIRE reduces pressure by stopping aggressive saving after a front-loaded phase.

- Barista FIRE reduces pressure by keeping some earned income, so you don’t need a full portfolio yet.

The two can also stack well: someone can hit a Coast number, then later choose Barista FIRE as an “escape hatch” if markets underperform or if the plan needs more margin.

Learn more in the Complete Guide to Barista FIRE

Traditional Retirement

Traditional retirement is the default cultural script: work most of your adult life, save steadily (often 10–15%), and retire later, typically around conventional retirement age, using a mix of portfolio withdrawals, pensions (if you have them), and government benefits.

How it differs from Coast FIRE:

Traditional retirement spreads the effort out. Coast FIRE concentrates it. Coast FIRE is basically saying: “I’d rather do the retirement work earlier, when remaining time is the biggest asset, and buy freedom in the mid years.”

Traditional retirement tends to optimize for stability and conventional milestones. Coast FIRE optimizes for optionality, more flexibility in your 30s, 40s, and 50s, because the retirement engine is already running.

Expat FIRE

Expat FIRE uses global living and geoarbitrage to lower the “FI number” required by lowering the cost of living (while maintaining, or upgrading, quality of life). Sometimes taxes and currency factors matter too, but the core lever is cost structure.

How it differs from Coast FIRE:

Coast FIRE is a compounding-driven plan: time + investing does the heavy lifting. Expat FIRE is a lifestyle-and-location plan: expenses are the lever.

This is why Expat FIRE can “bolt on” to Coast FIRE so well. If your Coast plan starts to feel tight because of inflation, lifestyle creep, or a change in circumstances, reducing expenses through location can keep the timeline intact without forcing you back into a punishing savings rate.

It’s also where the real-world variables show up: visas, residency, taxes, healthcare, and currency. Those aren’t reasons to avoid it; they’re reasons to plan it like an adult.

Learn more by reading The Complete Guide to Expat FIRE

Fat FIRE & Chubby FIRE

Chubby FIRE and Fat FIRE aren’t different math; they’re different lifestyles.

- Chubby FIRE usually means comfort plus margin.

- Fat FIRE means high discretionary spending plus more complexity.

How Fat FIRE and Chubby FIRE differ from Coast FIRE:

Coast FIRE can absolutely lead to Chubby or Fat outcomes, but your Coast number has to be bigger, and your plan needs more margin because higher spending is less forgiving. Bigger lifestyle targets also tend to create more complexity: taxes, insurance, asset allocation, and the psychological trap of “always more.”

Coast FIRE is most elegant when the target lifestyle is clear and stable. The more discretionary you want, the more you want guardrails and periodic recalibration.

Learn more in the Complete Guide to Chubby FIRE and the Complete Guide to FIRE

Lean FIRE

Lean FIRE is the essentials-first version of FIRE: minimize expenses, keep the lifestyle simple, and reach financial independence with a smaller number.

How it differs from Coast FIRE:

Lean FIRE shrinks the number by shrinking spending. Coast FIRE shrinks the effort later by front-loading savings and letting compounding carry the plan. You can do Coast FIRE toward a Lean endpoint (and many people do), but the main tradeoff is margin: the leaner the lifestyle, the less room you have for inflation, healthcare surprises, or life-changing shape.

Lean FIRE is powerful when you genuinely like a simple life. It’s fragile when it’s built on “I’ll tolerate this forever” rather than “this actually fits me.”

Learn more in The Complete Guide to Lean FIRE

Coast FIRE Myths, Corrected

Coast FIRE is simple enough that it attracts two kinds of misunderstanding: people who oversell it as a magic trick, and people who dismiss it because they think it’s just “retirement with a new name.”

Neither is right.

Here are the big myths, corrected.

|

Myth |

Reality |

|---|---|

|

Coast FIRE means you stop working. |

FALSE – Coast FIRE isn’t “stop working”, it’s “stop needing to save aggressively”, but you still work to cover current expenses while the portfolio compounds toward your future FIRE number. |

|

Coast FIRE is just doing nothing and hoping markets save you. |

FALSE – Coast FIRE is front-loaded with work: you do the hard work early (saving + investing), but you still maintain the plan with stress tests and annual check-ins. |

|

Coast FIRE is only for high earners. |

FALSE – High income helps, but Coast FIRE is really about starting early and building the “coast engine” with a lump sum invested properly. |

|

Once you hit your Coast number, you’re done. |

FALSE – Coast FIRE is not set-and-forget. Inflation, life changes, and market variability mean you need annual check-ins and occasional course corrections during both the coast and FIRE phases. |

|

Coast FIRE is always the smartest FIRE path. |

FALSE – It’s a lever, not a religion. Sometimes, continuing to invest aggressively buys more margin. Coast FIRE is best when it improves your life now without making the plan fragile. |

Myth #1: Coast FIRE means you stop working

Coast FIRE isn’t “stop working”, it’s “stop needing to save aggressively.”

That’s the distinction that matters.

In traditional FIRE, the finish line is when your portfolio can cover everything, and earned income becomes optional. Coast FIRE is earlier in the timeline: you’ve invested enough that, with time and compounding, it’s expected to become your full FIRE number, so you can stop forcing a high savings rate.

You still work. You just don’t have to run your life on hard mode to make the math work.

Myth #2: Coast FIRE is just “doing nothing” and hoping markets save you

Coast FIRE isn’t passive. It’s front-loaded.

The whole plan depends on doing the hard part early: saving, investing, and building the engine while you still have the most compounding runway. After that, “coasting” doesn’t mean ignoring reality; it means changing what you optimize for.

A real Coast FIRE plan includes:

- A stress test of multiple return assumptions, not a single number

- Inflation handling (nominal vs real)

- Annual check-ins to adjust course

If you’re not willing to revisit assumptions once a year, you’re not doing Coast FIRE, you’re just drifting.

Myth #3: Coast FIRE is only for high earners

High income helps. It’s not required.

Coast FIRE is really about two things:

- Getting a meaningful amount invested early (whether through a lump sum or a “burst sacrifice” period)

- Keeping your fixed costs from exploding later

AS in our example earlier, a 20-year-old tradesman saving consistently for 10 years can build a Coast FIRE engine just as effectively as a tech worker saving aggressively for 3. The timeline changes. The math still works.

What do you do when you’ve achieved your Coast FIRE number?

Hitting your Coast FIRE number is a weird milestone, because it doesn’t come with the obvious fireworks of traditional FIRE.

You haven’t “retired.” You haven’t crossed the finish line. You’ve just done something quietly powerful:

You’ve built an engine that should get you to your full FIRE number on schedule, without you having to keep pushing the savings boulder uphill every month.

So what do you do now?

You shift from accumulation mode to execution and maintenance mode.

That means two things at the same time:

- You start making career and lifestyle decisions with more freedom.

- You keep the plan honest with simple guardrails, so the engine doesn’t drift off course.

Financial Independence doesn’t mean you have to retire.

This is the part most people miss when they first encounter FIRE.

Financial Independence isn’t “never do anything productive again.”

It’s leverage.

It’s the ability to choose work for reasons other than fear:

- Because it’s meaningful

- Because it’s flexible

- Because it keeps skills sharp

- Because it connects you to people

- Because you like the rhythm

- Because you want the benefits

- Because you enjoy building something

Coast FIRE is basically a permission slip to stop treating your job as the center of the universe.

And once you hit your Coast number, the question becomes less “How fast can I escape?” and more:

What do I want my life to look like while the money compounds in the background?

Here are the most practical options.

1) Keep working, but stop optimizing for maximum income

A lot of people use Coast FIRE to make work more livable:

- Fewer hours

- Fewer meetings

- Less commuting

- Lower stress

- More control over where you live

- Better alignment with your actual values

You don’t need a dramatic resignation letter. You just need to stop building your entire life around earning one more dollar or slaving away for one more promotion, if where you’re at now is sufficient.

2) “Upgrade” your job quality, not your job title

Coast FIRE is the moment where it makes sense to optimize for:

- A better manager

- A healthier culture

- Flexibility

- Remote work

- A schedule you can live with

- Work that doesn’t drain your nervous system

This is also where people switch from “career ladder” thinking to “life design” thinking.

Not because you’ve given up. Because you’ve stopped pretending that a bigger title is automatically a better life.

3) Use Coast FIRE to invest in yourself (skills, health, optionality)

Coast FIRE creates time and margin. And that time can be converted into future leverage.

Common “smart uses” of this phase:

- Learning a high-value skill that improves earnings without increasing misery

- Building a side business slowly, without desperate timelines

- Improving health and sustainability so the plan doesn’t get derailed by burnout

- Taking a geographic reset to move closer to family, move to a lower cost city, or test living abroad

Coast FIRE doesn’t have to be the “coast forever” plan. It can be a bridge into something better.

4) Keep contributing to add margin and reduce fragility

This is the quiet power move.

Once you’ve hit your Coast number, you can stop contributions. But continuing to invest even a little:

- Increases your margin of safety in your investments and withdrawals later

- Lowers your reliance on perfect market returns

- Gives you options if inflation runs hot or life gets expensive

Think of it as buying safety. Coast FIRE works best when it’s calm, not tight.

5) Run a yearly check-in, so the plan stays real

This is the non-negotiable if you want Coast FIRE to be resilient.

Once a year, check:

- Are my expense assumptions still realistic?

- Did my (planned) retirement lifestyle change?

- Did inflation move the goalposts?

- Is my portfolio still aligned with the returns I’m assuming?

- Do I need to top off, delay, or pivot?

The people who get burned by Coast FIRE are usually the ones who calculate once and then never look again.

The people who win treat it like an operating plan.

Hitting your Coast number doesn’t mean you’re done. It means you’ve earned the right to stop living like every month is a race.

You can keep working. You can shift how you work. You can change where you live. You can keep investing. You can build something new.

Coast FIRE isn’t “retire early.” It’s “build leverage early”, then use it to design the middle of your life as it matters.

FAQ

What does it mean to “Coast FIRE”?

To “Coast FIRE” means you’ve invested enough that your current portfolio, left alone to compound, should grow into your full asset number required for financial independence by your target retirement age, even if you stop contributing.

The key idea in Coast FIRE is not “stop working,” it’s stop needing to save aggressively. You can keep working to cover your current expenses while your investments quietly do the long-range work in the background.

What is the difference between FIRE and Coast FIRE?

Traditional FIRE is about reaching the point where your portfolio can cover 100% of your expenses, and earned income becomes optional.

Coast FIRE is earlier in the timeline at the point where you can stop saving because your portfolio is expected to grow into your future FIRE number with time.

In short:

Traditional FIRE: stop working (eventually)

Coast FIRE: stop needing to save aggressively (now)

When do I know I can “Coast FIRE” and how do I know I’ve reached my Coast FIRE number?

You “know” you can Coast FIRE when your current invested assets meet (or exceed) your Coast FIRE number, which is the amount required today to grow into your target FIRE number by your target date.

That’s a calculation with assumptions. The way to calculate your Coast FIRE number is:

1. Pick a target retirement age

2. Estimate retirement expenses (in the lifestyle you actually want)

3. Compute your future FIRE number (25× expenses, or more conservative if you want a margin)

4. Discount that future FIRE number back to today using an assumed return rate and your years of coasting

5. Stress-test the assumptions (7% / 9% / 10%)

6. Build guardrails (annual check-in + “escape hatch” plan)

If your plan only works at your most optimistic return assumption (e.g., 10% returns) and no other assumptions (e.g., high inflation, 7% expected returns), you haven’t “reached Coast FIRE.” You’ve reached “Coast FIRE if everything goes perfectly.”

How much do you need to Coast FIRE?

How much you need for Coast FIRE depends on three things:

Your future spending (your retirement lifestyle)

Your timeline (how many years until retirement)

Your return assumptions (and how conservative you want to be)

That’s why “How much do you need?” doesn’t have one universal number. The same $1,000,000 future goal can require $20k–$400k today, depending on age and assumptions.

If you want the simplest rule: the earlier you invest, the less you need. Time is either your engine or your enemy.

Use our Coast FIRE Calculator to find your number

What investment rate of return should I use?

Don’t pick one number and build your life around it.

A clean approach is to use a range and stress-test:

1. Start with 7% / 9% / 10% for a diversified, equity-heavy portfolio

2. Run the calculator at all three

3. Build a plan that survives the less flattering scenarios

Also, remember: the market doesn’t deliver returns in a smooth line. The long-term average is not the same thing as what you experience year-to-year.

If you’re going to be conservative, be conservative on purpose, and know what tradeoff you’re making (higher Coast number, longer timeline, or more contributions).

What is inflation, and how does it affect Coast FIRE planning?

Inflation is the slow force that changes how much money buys throughout time. A dollar now buys more than a dollar in the future, and a dollar in the future buys less than a dollar now – that is inflation in action. Coast FIRE plans break when people calculate a FIRE number using today’s spending and assume future dollars have the same purchasing power.